-

-

Quick Contact

Get A free

Consultation Now!

Tag Archives: equifax

8 Ways to protect yourself from ID theft and financial hacks

We’ve all been carefully watching the news as details of the Experian credit hack unfold, but one thing is for sure: no one is safe from the threat of identity theft.

We’ve all been carefully watching the news as details of the Experian credit hack unfold, but one thing is for sure: no one is safe from the threat of identity theft.

In fact, according to data by the National Crime Victimization Survey/U.S. Bureau of Justice Statistics, 7% of U.S. adults 16 or older have been victims of identity theft.

Shockingly, across the world last year alone, 4.2 billion personal records were stolen by hackers and data thieves!

So there’s a strong chance that you may have your data compromised at some time in your life, and 86% of identity theft victims suffer the fraudulent use of one of their current financial accounts like a credit card or bank account.

Surveys show that 85% of Americans have already taken steps to prevent identity theft, such as shredding financial documents or changing passwords. But now more than ever, it’s critical that you take you fortify yourself against identity thieves.

Is a credit freeze the answer?

Many media outlets and credit “experts” have been advising people to place a freeze on their credit report.

Credit freezes do offer some protection since lenders won’t be able to pull your credit report and new accounts can’t be opened in your name.

To request a freeze, you have to contact each of the credit bureaus, Equifax, Experian, and TransUnion, separately, and each one will have details, terms, and restrictions on their website.

While freezes will protect against new accounts being opened in your name, they don’t even prevent the most common type of identity theft these days: misuse of existing accounts. In fact, only 4% of identity theft victims have new accounts opened in their names according to Bureau of Justice Statistics data

So what other options do you have to keep your identity safe?

Get a copy of your credit reports

It’s important to start by carefully reviewing all three of your credit reports for errant accounts or suspicious activity. You can request a free copy of your credit reports from TransUnion, Equifax and Experian or contact MyNationwideCredit.com for a free report and consultation.

Check your financial accounts

You should also monitor each of your financial accounts, including all credit card and bank statements. Even tax refunds have been a growing target of fraudsters, so IRS records also need to be reviewed.

Set strong passwords

The first line of defense against internet fraud and identity theft is setting strong passwords. The average person now has dozens of passwords that they enter online, many of them for sites and accounts that hold sensitive financial information.

When setting passwords, avoid personal information like birthdates, addresses, and family names. Use nonsensical combinations of letters and include numbers and !*#. You should also avoid using the same password for every account, and be careful about user names and what other information you store in internet accounts.

Enroll in a credit monitoring service

To ramp up your protection against identity thieves, consider enrolling with a reputable credit monitoring service. A good service will track all activity on your credit report every day, notifying you if there are any changes, such as a hard inquiry used to open new accounts or erratic charges.

Alert the authorities immediately

If you see suspicious activity or that you’ve been the victim of identity theft or fraud, contact the authorities immediately. You can file an identity theft report with the Federal Trade Commission (FTC) at identitytheft.gov.

The FTC also recommends that you file a report with your local police department if you’ve been the victim of identity theft.

Place a fraud alert on your credit reports

A fraud alert on your credit reports will raise the level of scrutiny and caution on your accounts if you suspect that you’ve been the victim of identity theft or even just a data hack. Creditors will need to contact you before opening any new credit lines or accounts. You only need to file a fraud alert with one of the credit bureaus since they are required to instruct the other two bureaus to do the same.

There are two kinds of fraud alerts. An initial fraud alert requires that a lender call you or make “reasonable steps” to contact you and confirm the new activity is valid and will last 90 days.

Extended fraud alerts are available if you’ve been the victim of ID theft and have a police report to prove it. You can only file an extended fraud alert one time but it lasts for seven years, and it requires that a credit contact you to verify new activity.

Register a credit lock

On face value, credit locks and credit freezes offer similar benefits, including preventing someone else from opening a new account in your name. But there are also some huge advantages to credit locks that you should consider. (You can’t institute a credit freeze and a credit lock at the same time.) In fact, credit freezes offer additional levels of protection over freezes, and also cost less.

Unlike locks, credit freezes are guaranteed by state law, so you have a level of legal protection. And while freezes can take a little time and effort to activate and deactivate, locks are initiated using an app on your smartphone and can be produced or discontinued immediately.

(However, only TransUnion and Experian offer instant credit locks, with Experian’s TrustedID Premier lock system taking 24-48 hours to process).

Similarly, only two bureaus (this time, TransUnion and Equifax) offer free credit locks, so you’ll have to pay for Experian’s CreditWorks lock program. But it’s still probably worth it considering that Experian’s credit lock program also offers daily credit monitoring and alerts.

***

Do you have any questions about the Experian hack, how to monitor and safeguard your credit and protect from ID theft? Contact Nationwide Credit Clearing for a free credit report and consultation!

25 Facts about the Equifax hack – and what you can do to protect yourself

1. Equifax – which is one of the country’s big three credit bureaus (along with TransUnion and Experian) recently suffered a significant data breach.

1. Equifax – which is one of the country’s big three credit bureaus (along with TransUnion and Experian) recently suffered a significant data breach.

2. In fact, according to the company, the personal data and even some financial records for up to 143 million Americans has been compromised – which amounts to about half of the total U.S. adult population!

3. Equifax (EFX ) is a private company that’s traded on the New York Stock exchange with a mandate is to earn profits for its shareholders, which it did to the tune of over $3 billion in revenues in 2016.

4. Along with TransUnion and Experian, makes money by collecting your financial and demographic information, analyzing it in the form of a credit report, and then selling that data to lenders, banks, mortgage companies, auto dealers, credit card firms, and yes, even marketers.

5. However, although Equifax tracks the payment and credit statistics for nearly every American adult (a small number are what’s called “Credit Invisible”), they don’t seek our permission, nor is there a way to opt out or keep your data private.

6. Equifax’s negligent mishandling of the situation has been highly publicized. The timing, for one, is of grave concern. Reportedly, Equifax knew about the data breach as early as mid-May but didn’t announce the hack publically until July 29.

7. Industry reports point to the fact that the security breach in Equifax’s platform existed for nine years without being fixed, and hackers slowly siphoned off consumer information for months.

8. Signaling that some serious malfeasance took place, three high-level Equifax executives sold shares of their own holdings after the hack was discovered, but before it was made public.

9. These three inside-trading execs, including Equifax’s Chief Financial Officer John Gamble, made $1.8 million from the sales of Equifax stock – before stock prices fell upon news of the hack.

10. By cracking Equifax’s database, the cybercriminals were able to obtain consumer records including names, Social Security numbers, birthdates, addresses and driver’s license numbers – all of the information they need to open new accounts or commit identity fraud.

11. According to credit expert John Ulzheimer, those pieces of data are “the crown jewels of information for credit fraudsters.”

12. Since people’s names, social security numbers, birth dates, etc. never change, the information can be used to defraud and steal from consumers without a shelf life.

13. According to Equifax, the credit card numbers of at least 209,000 consumers were also lost in the hack.

14. Just as concerning, the compromised data may include user names, passwords, security questions and other login information for Internet websites and other financial accounts.

15. In the wake of the breach, two high-level Equifax employees stepped down this week, Chief Security Officer Susan Mauldin and Chief Information Officer, Dave Webb.

16. Shocked by the magnitude of the breach and the revelation that Equifax hid it from the American people, Equifax stock plummeted, falling from $142 per share to $92 as per the time of this writing.

17. Both the FBI and the Federal Trade Commission have initiated investigations into the hack, as well as possible Equifax impropriety. Additionally, the state attorney general of Massachusetts is suing the credit giant, and class action suits are also springing up by the day.

18. So what is Equifax doing to try and remedy the problem? The credit firm has set up a special website where consumers can log in and see if their data was included in the 143 million stolen by hackers.

19. However, you need to enter your last name and social security number to access their website – which is questionable considering the circumstances.

20. Equifax is also extending the offer of free credit monitoring service, called “TrustedID Premier,” for a year to those affected.

21. TrustedID Premier includes credit monitoring of Equifax, Experian and TransUnion credit reports, a credit freeze for Equifax accounts, identity theft insurance, and a monitor to see if someone is trying to sell your social security number on the internet.

22. This may sound sufficient, but critics argue that Equifax isn’t completely forthright about their help. For instance, once the year offer expires, the service is no longer free but costs $19.95 per month. (Consumers actually have to enter their credit card number just to enroll in Equifax’s “free” year-long monitoring service.)

23. It’s been slammed as a back-door way for Equifax to reduce their liability, too. Buried within the fine print when you sign up for TrustedID Premier was a release of liability, renouncing your rights to later sue Equifax or participate in any class action suit.

24. Lambasted in the media and pressured by consumer rights groups, Equifax quickly softened the language of this release to “the arbitration clause and class action waiver included in the Equifax and TrustedID Premier terms of use does not apply to this cyber-security incident,” as well as allowing consumers to opt-in.

25. So what should you do now?

Don’t wait until your financial accounts are hacked or your identity stolen until you act. In fact, we can almost ensure that there are more big data hacks coming, since 65% of Fortune 100 companies still use that same processing framework (called Apache Struts) that was so easily hacked at Equifax.

The best thing to do is to be proactive, starting with checking your credit reports in detail (not just score).

From there, we recommend utilizing these tools to protect your identity and finances:

Credit monitoring

Whether you take advantage of Equifax’s offer or use a trusted third-party service, credit monitoring will keep tabs on your credit report for signs of fraud or impropriety.

Fraud alert

Establish fraud alerts with each of the three major credit reporting agencies, Equifax, Experian and TransUnion, as well as alerts for each of your credit and debit cards.

Credit freeze

A credit freeze goes a step beyond fraud alerts in protecting you, which locks your credit files. No new accounts can be opened in your name without going through a security protocol, and only companies that you already commonly do business with will be able to make charges on your cards.

Change your passwords

It’s a good time to go through and change your passwords, for all Internet sites as well as banking, credit, and financial services. Make sure these are secure, not based on your address, birthday, name, or any personal information, and stored in a safe place.

***

In this extraordinary time of confusion and risk, we’re happy to provide you the information and tools you need to protect your credit – and your family’s financial future. Feel free to contact us anytime for a no-cost credit consultation.

What Is A Credit Report?

An extremely detailed report of a person’s credit history, that is prepared by a credit bureau, is what makes up a Credit Report. The report is typically used by a lender in determining a loan applicant’s creditworthiness, including the following:

- Summary of credit history

- Detailed account information

- Personal data

- Credit history

- Details of any accounts turned over to a credit agency

The information includes how often you make your payments are made on time, how much credit you have, how much credit you are using, and whether a debt or bill collector is collecting on money you owe. It can contain public records such as judgements, liens, collections & bankruptcies that provide insight into your financial status.

How Does A Lender Use A Credit Report?

Lenders will obtain your credit card when you are deciding if they want to loan you money. They will also use it to determine what interest rates they will give you and to determine whether you will be able to meet the terms of the account they are providing. Other kinds of companies such cable, insurance, utilities etc. will always run a check to make sure you will be able to meet the financial terms of the program/service you are requesting. Additionally, an individual or company that is renting you a residential property can check your credit report before renting to you.

Who Makes A Credit Report?

Credit reporting companies, known as credit bureaus or consumer reporting agencies, create credit reports. The major bureaus in the U.S are Experian, Equifax and Transunion. There are also specialty consumer reporting agencies that can report your history of paying bills for a product or service.

How Nationwide Credit Clearing Can Help You

At Nationwide Credit Clearing we professionally assess your individual credit situation by procuring information that allows us to obtain a copy of your credit report. Our staff of professionals will review the information and determine the best method of credit repair to use based on your specific situation. Our long standing reputation working with credit bureaus goes back as far as 1985. NCC works with all three major Credit Bureaus:

If you or someone you know has something on their credit report that continues to hold them back from living a financially full-filling life, it’s time to call the Credit repair experts at Nationwide Credit Clearing

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

Lower credit score?

How is it that you can actually get a lower credit score when you feel like your spending habits have gotten better? Learn why your credit scores might have dropped since you last checked them by using this informative infographic below:

In summary, here are 5 solid reasons your credit score may have recently dropped:

1. 30 plus days late on payments

2. Credit Card balances exceed 30% total

3. Closing an old account

4. Too many Credit Card Inquiries

5. Identity Theft may have racked up debt without you knowing.

If this seems overwhelming to you, it’s important to call a credit repair company such as Nationwide Credit Clearing

Our Family of Experts is Ready To Get You Back To Healthy Credit

LET US HELP YOU SOLVE YOUR CREDIT TROUBLE (773) 862-7700

Nationwide Credit Clearing, the home of the Free Credit report and Consultation.

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

CLICK BELOW FOR YOUR…

![]()

Why Is My Overall Credit Score Important?

What Is A Credit Score?

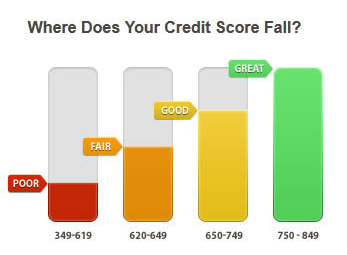

A credit score is a three-digit number, typically between 300 to 850, which credit bureaus calculate based on information in your credit report. It is a simple, numeric expression of your credit worthiness. Although the three credit reporting bureaus (Equifax, Experian, and Trans Union), use similar methods to determine a credit score, the formulas they use are not exactly the same and your credit score will vary from bureau to bureau.

How is My Overall Credit Score Calculated?

Your credit score is calculated based on a number of factors listed in your credit history that describe components of your financial life including the number and type of credit accounts you have, the amount of available credit, the length of your credit history and your payment history. Each of these factors is assigned a numerical value, and then weighted based on how prominently they affect your credit worthiness.

How Do My Actions Impact My Score?

The good news is that no matter where your credit score is today, there are a number of different steps you can take now that can change your credit history and help impact your credit score. You should take all the steps you can to help establish a good credit score.

Why Should I Check my Credit History and Overall Credit Score?

In today’s digital economy, your credit history and credit score are vital pieces of information that are key to helping you secure your financial life. Credit card companies, mortgage lenders, and insurance companies will pull copies of your credit report and score in order to decide whether to extend credit or how much to charge for your insurance premium.

Financial services companies tend to group borrowers into segments according to their credit score. These credit score ranges may determine how much you’ll be charged for your insurance coverage or the interest rate you pay on your mortgage, student or car loan or the type of credit card you’ll be offered.

If you haven’t checked your score lately, or have interest in improving your overall credit score, contact Nationwide Credit Clearing.

We offer Free (no credit card required) consultations after we pull your free credit report. Contact us Today!!

X-5 Credit Repair System

New X5 Credit Repair is the newest software that has been rolled out by Nationwide Credit Clearing. This software is the most cutting edge on the market today. once you become a client, you will be able to login to your account online to view the status as well as send email updates frequently regarding the status of your deleted items.

Along with that, everytime your file is updated, you will receive a text message regarding the changes.

On another note, if you just happen to be a mortgage broker and you refer a client to Nationwide Credit, you will automatically become an agent so you can check on the status of potential clients credit reports and deletions.

Remember, Nationwide Credit Clearing is the #1 Credit Repair company in the industry, providing you with the ultimate in credit repair technology… contact us today for your FREE credit report and consultation.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

![]()

Credit Repair Results – A Case Study

Nationwide Credit Clearing has been in the credit repair business for 28 years and we have helped thousands of people eliminate deragatory items from their credit report. We handle all of the work for the clients from start to finish. We give the client a free credit report consultation on day one. For us. however, It’s not just about signing up clients- we want to help them reach their goals. We Care! This is how much we care….

Here is an example of a client we have been working with more recently, and you can see by the data below… WE GET OUR CLIENTS RESULTS…

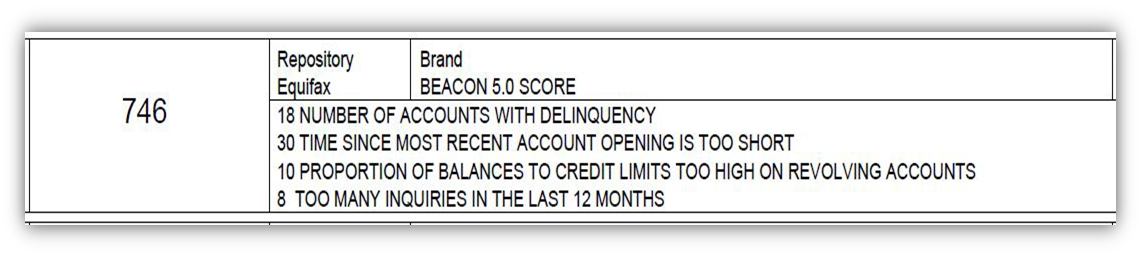

EQUIFAX: Score increase 26 Points from 720 to 746

Before:

After:

TRANSUNION: Score increase 42 Points from 685 to 727

Before:

After:

After:

EXPERIAN: Score increase 89 Points from 667 to 756

Before:

After:

As you can see, we take your credit matters personally, and if we don’t get you results, we are not satisfied. If your new years resolution involves managing your money or increasing your credit score so that you can ultimately live a more fullfilling life, then you came to the right place.

As you can see, we take your credit matters personally, and if we don’t get you results, we are not satisfied. If your new years resolution involves managing your money or increasing your credit score so that you can ultimately live a more fullfilling life, then you came to the right place.

What are you waiting for? Click HERE to get your FREE (no credit card required) Credit Report and Consultation…

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

How long does information stay on my Credit Report and how can Credit Repair help me?

This is a great topic because it is one of Most Frequently Asked Questions to credit repair companies by those who are trying to improve their overall credit score. The answer is probably not what you are looking for if you are someone who has had significant late payments, judgements, bankruptcy or other

This is a great topic because it is one of Most Frequently Asked Questions to credit repair companies by those who are trying to improve their overall credit score. The answer is probably not what you are looking for if you are someone who has had significant late payments, judgements, bankruptcy or other

Here’s the Breakdown:

and Although It depends on the type of negative information, here’s the average idea of how long different types of negative information will stay on your credit report:

- Late payments: 7 years

- Bankruptcies: 7 years for completed Chapter 13 bankruptcies and 10 years for Chapter 7 bankruptcies.

- Foreclosures: 7 years

- Collections: Generally, about 7 years, depending on the age of the debt being collected.

- Public Record: Generally 7 years, although unpaid tax liens can remain indefinitely.

Length of Time Matters:

For all of these negative items, the older they are the less impact they are going to have on your FICO® score. For example, a collection that is 4 years old will hurt much less than a collection that is 4 months old.

After that time it will be automatically removed from your report. But 7-10 years is a long time, and that negative information can be standing in the way of you buying a car, a house, or getting a good loan. Public records have a huge impact on your credit report and your credit score as well.

At Nationwide Credit Clearing, we help you get those items removed. There is no reason for those items to remain on your report for 7-10 years.

Positive Information:

All positive information on your credit report can stay there forever. The more positive information, the better your credit score will be

It’s time to start learning how to STOP LETTING BAD CREDIT AFFECT YOUR FINANCES. When you sign up with Nationwide Credit Clearing, we take the lead to work on your credit report and dispute unfavorable or inaccurate and outdated information. By doing this it will help save time, energy and frustration. More importantly we help to improve your credit score and ultimately fulfill your dreams… whatever they may be!

Nationwide Credit Clearing offers absolutely FREE – no credit card required – credit reports and consultations. To see your credit score, contact us now.

Comments