-

-

Quick Contact

Get A free

Consultation Now!

credit score

10 Things a good credit score can get you.

Your credit score is just a number, right? I mean, how important can it be to your finances?

Your credit score is just a number, right? I mean, how important can it be to your finances?

You know what else is just a number? Your bank balance, the amount you owe in debt, how much income you earn, and even at what age you’ll retire!

In fact, your credit score is more important than ever for nearly every aspect of your finances.

To prove it, we’ll cover ten things that you’ll get with a good credit score:

1. House

So, you finally want to achieve the American Dream by owning your own home? Well, if you’re like most people, you’ll need to obtain a mortgage to buy that home, and a good credit score will vastly help you qualify. In fact, the higher your score, the more loan options will be available to you and the lower your interest rate generally will be. The good news is that there are loans, like those guaranteed by the FHA, that can help lower-credit borrowers, but a high FICO will definitely come in handy.

2. Lower credit card interest rates

The average credit card interest rate in the U.S. is now around 14.99%, but that climbs to a lofty 24.9% when we look at credit card holders with lower credit scores. We’re also spending a LOT on our credit cards again, as the U.S. balance is now approaching $1 trillion! Increase your credit score and you’ll start saving significant money on your credit cards, almost immediately.

3. Business, personal, school.

Are you starting a business? Taking out a personal loan from the bank? Or even applying for student loans (which is now higher than both credit card and auto debt in the U.S.)? If so, a great credit score will be a huge help along the way.

4. Renting

Even if you can’t afford to buy your own home, you’ll have to live somewhere, and that means renting. As part of the initial application, you better believe that landlords check credit score these days for prospective tenants.

5. Lower insurance premiums

A lot of people don’t realize this, but insurance carriers actually cross reference credit scores of their policyholders (along with plenty of other factors) and assign higher premiums to those with low scores.

6. A better budget

If your credit score could magically go from 550 to 750 (and it CAN – it’s just not magic), you’d realize some incredible savings across most line items on your monthly budget. Add it all up and that savings could come to $100, $250, or even $500 a month!

7. Favorable utility and cell phones

Yes, even your utility providers check your credit score now, as they look to avert defaults. If you’ve walked into a cell phone store and asked to open an account then you know that the AT&T, Verizon, and others check credit, too.

8. More savings + less debt

With that new and improved budget, things are finally turning around for you financially. With extra disposable income every month, you can now afford to put some aside for savings every month and, most importantly, start paying down your debt. That’s when you REALLY start realizing more money in your pocket.

9. Dream job

Wait, a good credit score can get me a job? Well, not necessarily, but a bad credit score can certainly ruin your chance of landing your dream position! In fact, more than half of all employers do credit checks on their applicants these days and some, like in financial services, definitely will want a clean credit history and solid score before inking you to a new employment contract.

10. Financial security

Lower credit card rates, becoming a homeowner, paying off debt, saving for emergencies, and landing a new job all mean one thing: you’ve finally broken through the frustration, hard times, and penny-pinching that your low credit score brought. Studies show that consumers with good credit scores have a net worth that’s roughly 12-times that of low-scorers, and that’s no accident!

Are you ready to get these ten things a good credit score will bring you? We’re prepared to help with a free credit report and consultation, so contact us today!

50 Traits to help you achieve success, wealth, and financial independence. (Part 1)

What separates the most successful and wealthy people from the average person isn’t natural talent. They don’t have some secret the rest of us don’t have access to, nor are they luckier than we are. In fact, there are specific fundamental core concepts that just about every ultra-successful or wealthy person has in common. (Yes, maintaining an excellent credit score is definitely one of them!)

What separates the most successful and wealthy people from the average person isn’t natural talent. They don’t have some secret the rest of us don’t have access to, nor are they luckier than we are. In fact, there are specific fundamental core concepts that just about every ultra-successful or wealthy person has in common. (Yes, maintaining an excellent credit score is definitely one of them!)

It turns out, if you want to be well-off, it doesn’t matter where you came from, how much money your parents had, or what your present circumstances are. Maybe your credit score is 500 and you’re saddled with debt, but you set your mind to becoming debt free? Or, you’re a renter but want to buy a home because you’re tired of overpaying to make your landlord rich. It’s possible that your finances are well under control, but you’d like to build a better financial future for your family.

No matter what your version of “success” or “wealth” is, we all have to walk the same path to get there – which means incorporating these 50 habits to achieve success, wealth, and financial independence:

1. Pay off bad debt.

Successful people understand that paying interest is a great way to make someone else rich – and keep struggling, yourself. In fact, financially comfortable people always pay off credit cards, car loans, small installment loans as fast as they can, and don’t carry personal debt on a month-to-month basis. While they often pay off their mortgages as well, they distinguish between “good debt” and “bad debt.”

2. Plan for rainy days.

Financially aware people may take risks, but they definitely are pragmatic as well, planning and preparing for the unforeseen. They keep a good amount of savings, make sure they are well insured and protected, and generally minimize liability in every aspect of their lives.

3. Automate savings.

Whatever they earn, successful people break off a tiny piece and stash it, deducting it directly from each paycheck. This is what they mean by “pay yourself first,” as it gives them a solid foundation to invest and grow before they ever touch the rest of the funds for basics or play.

4. Invest young.

Even in their 20’s or sometimes their teens, these folks understand the compound principle of money. By putting money into 401k’s, Roth IRA’s and the like early, they benefit from returns and a windfall as they get closer to retirement.

5. Go the extra mile.

People who achieve big things in life invest extra effort, thought, and creativity into everything they do, no matter how big or small.

6. Sacrifice.

When you look at those who achieve excellence at anything from art to sports to neuroscience, the typical pattern is that that didn’t spend a ton of time partying or playing video games. Any classically trained musician will tell you that they didn’t attend a lot of social functions so that they could practice.

7. Log long hours.

Successful people got the hard work out of the way early, not looking for shortcuts or get-rich-quick schemes. By doing, they learned to refine their work, the way a swimmer refines their stroke to maximize the outcome and minimize the effort.

8. Problem-solving.

Instead of getting hung up on the minutiae of the process, they’re constantly focused on the target, asking questions like: how can I improve? What is lacking or holding me back? There is a built-in evaluation of every project they undertake.

9. Self-awareness.

People who accomplish great things in life are confident but not cocky, have a good sense of their own strengths and weaknesses, and have a high self-worth, while remaining humble.

10. Curiosity.

Some of the most unlikely experiences give rise to the best ideas. Great thinkers get outside their bubble and open themselves up with a relentless curiosity about the world.

11. Specialization.

They have specific training, knowledge, skills, and talents. Instead of just being generalists, high achievers invest in the education or training to become the best at one single thing, while adding on to their core skill. For example, professional athletes train constantly, but they also educate themselves on nutrition, concentration, and responsiveness.

12. Literacy.

There is no substitute for reading and ultra-achievers read non-stop. Studies show that 88% of wealthy read 30 minutes or more every day (for education or career reasons – not romance novels!). Reading is part of that core skill set, no matter the discipline.

13. Organization and goal setting.

81% of wealthy and successful people scratch things off a daily To Do list compared to only 19% of working class people. Just the act of writing down goals is very powerful, allowing the mind to prioritize and receive a jolt of satisfaction from completing even simple tasks.

14. Wise use of time.

Successful people use their downtime to inspire their projects and explore other ways of thinking. Since time is our greatest asset, successful people don’t spend theirs on empty entertainment. In fact, 67% of wealthy people watch one hour or less of TV every day, while 23% of poor people do, and only 6% of wealthy watch reality TV shows vs. 78% of poor.

15. Milestones.

Setting tangible goals with concrete timetables and planning the action steps to achieve them is crucial to success. Being able to break down big goals into small digestible steps is key, along with a consistent reevaluation of their plan based on changing circumstances. If we don’t, then we aren’t experiencing progress and our projects quickly lose momentum.

16. Risk and a relationship to failure.

Failure is not the enemy of successful people – it’s a necessary instrument of growth. In fact, if they don’t go through enough failure in their lives, they understand they’re not taking enough risks.

17. Optimism bias.

Successful people don’t wait around for luck to bless them –create their own opportunities with hard work, smart planning, and confidence in their efforts. In fact, 84% of wealthy believe good habits create opportunity instead of luck, while only 4% of poor believe the same. Furthermore, 76% of affluent people attribute negative outcomes to bad “luck” vs. only 9% of the poor.

18. Responsibility.

People who own their actions good and bad, and exhibit accountability for their actions tend to draw quality people around them. They never try to pass the buck or dodge blame – this goes back to that self-awareness piece.

19. Flexible thinking.

Agility takes practice, but it’s a necessary skill. Successful people have firm values but flexible thinking, adjusting their sails depending on how the wind blows.

20. Create vs. consume.

Instead of just amassing and worshipping material things, successful people are marked by their contributions, whether it’s a new business, building a house, or forming a non-profit. Creation is one of the processes held in highest esteem by high achievers.

21. Presence of mind.

The key to success (and happiness) is to always be fully present in the moment. That goes for work as well as play.

22. Motivation.

Mega high achievers dare to dream about the unattainable…then they attain it! In fact, 80% of wealthy and successful people are focused on a singular goal – and never take their eye off the ball.

23. Persistence.

“Fall seven times, get up eight,” as the old saying goes. You hear great minds talk about setbacks and disappointments, but they understand that their success is earned by bouncing back.

24. Dissatisfaction with the status quo’.

It’s really about developing a vision rather than accepting mediocrity. Achievement is about reaching higher.

25. Singular focus.

Multi-tasking is a myth that amounts to “do everything badly.” The human brain can only fully focus on one thing at a time. Successful people know this and don’t try to juggle – work in immersed short bursts of concerted effort.

***

Look for part two coming soon with 25 more traits of wealth and success!

As our society grows older, the financial burden looms.

What’s the fastest growing societal problem in the United States, as well as around the world?

What’s the fastest growing societal problem in the United States, as well as around the world?

While there are plenty to choose from, unfortunately, the impact of an aging population may be the most significant challenge we face. From healthcare to retirement, social services to housing, as the average life expectancy grows and the roles and needs of our seniors change, this massive demographic shift is already causing cracks in the faultline of our economy.

But it was only a decade or two ago that the thought of seniors needing to carefully manage their credit scores, credit card debt, and student loans was virtually unheard of.

In this ongoing series, Nationwide Credit Clearing will dissect some of the facts, stats, and financial trends among seniors in the U.S. Aside from offering this education, we really want to help, so any senior can contact us for a completely free consultation and credit report.

10 Facts, stats, and trends in senior finances:

1. Between 2007 and 2016, the percentage of senior households (with members 75 and over) grew from 31.2% all the way to 49.8% – or nearly half.

2. The amount of debt is also skyrocketing in the average older households, from $30,288 in 2010 to $36,757 in 2016. In fact, among older households with debt, the median total has risen more than 2.5 times since 2001!

3. Likewise, in 1992, only 41.5% of senior households had any debt, but that number has now risen to 60%.

4. More than 40% of single adults also count on their monthly social security check for 90% of their living expenses and income. The amount of that check? Only $1,404, on average.

5. Medical debt is one of the fastest growing financial burdens. Consider that 84% of people 65 years or older face at least one chronic condition. But insurance is covering less and less of the cost for their care, so in the five years leading up to their death, the average senior racks up $38,00 in medical (or medical-related) debt, and 1 in 4 approach bankruptcy.

6. Even credit card debt is on the rise among seniors. In 2001, just less than a quarter (24.2%) of seniors had any credit card debt at all. Now, more than 1 in 3 (34.2%) carry balances on their credit cards that aren’t paid off monthly. In fact, seniors hold 50% ore credit card debt than members of Gen Y!

7. You may be shocked to hear that the fastest form debt among seniors is student loan debt! It’s true, as these days, 2.2 million Americans 60 or older are responsible for student loans. However, it’s not that these industrious seniors are going back to school. Instead, they’re cosigning for their children or grandchildren at rates that have tripled since 2005. And with minimum student loan payments averaging $700 a month and the younger generation having a harder time making ends meet or defaulting more and more, these seniors are assuming the financial burden.

8. The financial picture for more and more seniors is bleak. In fact, one-third of all senior households either is going into debt every month to pay basic living expenses, or just breaking even.

9. Even more distressing, 25 million Americans ages 60 and up are considered economically insecure – which is living at or below 250% of the federal poverty level (that comes to about $29,425 for a single person.)

10. If we look at the data on credit scores, we see that seniors have the highest credit scores of any generation. In fact, the average FICO for all consumers 70 and over is 747, while 60-69 year-olds have an average FICO of 722 (and it goes down to about 640 for those 18-29.)

However, that doesn’t tell the whole story, as seniors are now defaulting on their financial obligations and debts at an unprecedented rate. Facing massive healthcare costs and medical bills, rising credit card and student loan debt obligations, and a shortfall from social security and retirement planning, seniors are now in need of some credit score help like the rest of us.

***

Look for part two in this series about the financial burden that comes with aging. And remember that we really do want to help, so any senior can contact us for a completely free consultation and credit report.

The homebuying and mortgage process starts with your credit score.

Homeownership rates are near modern-era lows, but it’s not because people don’t want to buy. But surveys reveal that coming up with a down payment, qualifying for the mortgage, too much debt, and even credit score are holding them back from homeownership.

Homeownership rates are near modern-era lows, but it’s not because people don’t want to buy. But surveys reveal that coming up with a down payment, qualifying for the mortgage, too much debt, and even credit score are holding them back from homeownership.

In fact, the majority of people who are planning to buy a house in the next 12 to 18 months are pretty confused about what credit score they need, and how to improve their score. However, this national survey found that only 45 percent of potential home buyers really understand what their credit score is measuring – their responsible management of debt and risk of defaulting on new loans.

Likewise, less than 50 percent of respondents could identify what their credit score affects in the mortgage process (such as interest rates, program guidelines, and the amount they qualify for.)

Their lack of clarity can actually hurt their score, further delaying or even canceling their plans to buy a home. For instance, 33 percent of consumers polled think that increasing income will help their credit score, and 28 percent believe that closing old accounts will do the same (not the case).

Even more concerning is that they’re unsure of where to even start with the knowledge, actions, and assistance to ready their credit for a home purchase. Only 22% of people polled thought that they should check their credit report in the three months leading up to their mortgage application!

Of course, when people start the process of buying a home, there are a lot of things to focus on: which neighborhood they want to live in, finding the perfect house, getting approved for a mortgage at a great interest rate, and then the all-consuming process of packing and moving. But before any of that happens, there is one more item that should lead off their checklist: taking care of their credit score.

So, keeping your credit score up to par has some very tangible benefits during the home buying process:

• Lower interest rates,

• A greater variety of loan programs available,

• Qualify for loans with less money down,

• Your offer on a house will be seen as more favorable if you have a high credit score, giving you more leverage. During multiple offer situations and bidding wars, the seller sometimes requests additional documentation like proof of the buyer’s credit score and funds.

• But, of course, saving money when you make your mortgage payment every month is the real benefit. Even a credit score increase of a few points may help you qualify for a lower interest rate, adding up to tens of thousands of dollars in savings over the life of your loan.

Consider these three scenarios, where three consumers who are buying a $400,000 home, with a $320,000 mortgage, qualify for interest rates of 4%, 4.5%, and 5%, respectively. Please note this is just an illustration for educational purposes.

Interest Rate: 4%

Monthly Payment: $1,527

Total of 360 Payments: $549,982.42

Total Interest Paid: $229,982.42

Interest Rate: 4.5%

Monthly Payment: $1,621

Total of 360 Payments: $583,701.48

Total Interest Paid: $263,701.48

Interest Rate: 5%

Monthly Payment: $1,717

Total of 360 Payments: $618,418.51

Total Interest Paid: $298,418.51

That means if your credit score was top notch and you qualified for a 4% interest rate (hypothetically), you’d save $190 a month compared to the 5%, and $94 compared to the 4.5% loan. That sounds nice, but doesn’t seem like big money, right?

But when you compare the long-term savings, the person with the 4% loan saves $68,418 in total payments over the life of the loan compared to the 5% loan, and $33,719 compared to the 4.5%

That’s some HUGE savings for just a very small interest rate difference. (For even more information how a good credit score will save you money, read this.

So, how do you make sure your credit score is ready for the home buying process? Here are some tips to make sure your credit score will be as high as possible when you’re ready to buy a home:

1. Always pay on time.

According to FICO, 96% of people with a FICO score of 785 or greater have no late payments on their credit reports, so be one of those people who have a spotless payment history if you want the perfect FICO. Since payment history is 35% of FICO’s scoring model, paying on time is crucial.

2. Check your credit report periodically.

It’s important to make sure that there are no errors on your credit file and everything is in order. These days, you also need to make sure that your identity hasn’t been stolen or compromised, which affects up to 1 in 8 Americans every year.

3. Spend less and pay down your balances.

FICO calculates a significant portion of your score by your credit utilization ratio – how much debt you keep to how much your total available balances are. A survey of those who had the top scores revealed their average credit card balances relative to their limits was just 7%.

FICO calculates 30% of their scoring model by the overall money you owe and how close you are to the limits on your credit cards and revolving debt, so low balances, and healthy ratios are the key to a top score.

4. Keep a good mix of credit.

Consumers with FICO scores above 760 have, on average, six accounts that are currently “paid as agreed” and an average of 3 accounts with a balance.

5. Keep well-seasoned accounts.

Most super scorers also have, on average, an account that’s 19 years old. The average age of their accounts is between 6 and 12 years old and they opened their most recent account 27 months ago or more. 15% of FICO’s scoring is calculated by the credit history.

6. Start early.

Don’t wait until you’re ready to start looking at houses or apply for a mortgage to start working on your credit. Get a copy of your credit report from Nationwide Credit Clearing six months before you’re ready to apply for a mortgage. That will give you plenty of time to pay down debt, close unwanted accounts, or dispute errors and inaccuracies in order to maximize your score – as well as working with Nationwide Credit Clearing to repair your score.

7. Do’s and Dont’s during the home buying process.

It’s important not to make big changes during the mortgage process, as it may trigger a red flag for lenders, who are trying to make decisions based on a static snapshot of your finances. Avoid big purchases on credit, moving large sums of money to and from bank accounts, and applying for any new credit or closing existing accounts.

8. Consider getting help.

Before you even sit down with a mortgage broker or take a ride around town with a Realtor, home buyers would be wise to contact Nationwide Credit Clearing. With a complimentary free credit report and consultation, we can analyze your situation and give you an accurate assessment if your credit is home-buying worthy or needs some work.

Contact us today to get started – and happy home hunting!

10 More ways to start saving money today! (Part 2)

Do you want to save money? Of course, you do! In part one of this series, we brought you ten ways you can start saving money immediately. Today, we’re back with ten more money-saving tips and hacks.

Do you want to save money? Of course, you do! In part one of this series, we brought you ten ways you can start saving money immediately. Today, we’re back with ten more money-saving tips and hacks.

You’re very welcome!

Make sure to follow Nationwide Credit Clearing for more great information on improving your credit score, saving money, and creating a brighter financial future.

Ten more money-saving tips and hacks:

1. Check for bank fees and credit card annual fees.

These days, banks make countless millions of dollars every year just on fees, charges, and other avoidable costs. But that doesn’t mean you need to stand for it – check to see what kind of fees your bank and credit card companies are charging you and don’t be afraid to take your business elsewhere. Just be reading the fine print and moving your money to a bank, credit card, or financial institution that charges less but still matches your needs, you can save a few hundred dollars every year.

2. Watch those ATM fees.

When you use a bank other than your own, the average financial institution hits you for $2.50 in ATM fees AND your own bank can charge you an average of $1.57. Ouch. Plan your trips to the ATM so you’ll always have enough cash on you, or use your debit card at places that don’t charge a service fee. Just by paying attention to when and where you use the ATM, you may be able to save $10-$25 every month per adult in your household.

Money-saving tip: most supermarkets don’t charge fees for cash back on purchases!

3. Find coupons, rebates, and discount codes.

It may be a little cliché to sit at your kitchen table pouring through the newspaper and cutting out coupons, but these days, just about everything you need is online to save some serious bucks. In fact, most retailers have specials, promotions, coupons, rebates, and offer discount codes for good customers – all accessible to you for free on the web.

But instead of spending a whole lot of time hunting for the money-saving offers you need, there are amazing websites available that search out, aggregate, and present all of those money-saving opportunities for you. You can even enter your favorite store or the products you normally buy, or specialty items you’re looking for and receive email alerts when great deals pop up.

4. Refinance your mortgage.

Call a mortgage broker or your current lender to see if you can take advantage of today’s super low rates. Even the difference of one percentage point in interest rate can save you tens of thousands of dollars over the life of the loan!

In fact, the best way to take advantage of a refinance with lower interest rates is by improving your credit score, which can save you tens of thousands of dollars – or more – over the term of the loan!

5. Review your cell phone plan.

Call up your carrier and ask to review your usage minutes and the plan you’re on. You might be overpaying for something you never use. Are there a few people in your household that use cell phones? Make sure to price out a family plan. In addition, if you have a home phone that you don’t really need, it’s a good time to cancel it.

6. Buy a good coffee maker.

If you’re like me, you’ll NEVER consider abandoning your much-needed caffeinated beverage, but making it at home will save you buckets of money. The average American spends $1,100 a year on coffee, though I would argue us working professionals drop even more at Starbucks. A good coffee maker will cut that cost by about 1/20 and you can make it how you like. Buy a thermos and bring extra to work for that afternoon caffeine injection.

7. Plan your meals out.

If you’re like me, you waste a lot of money on eating out. In fact, the average American spends more than $2,500 a year eating out! There’s nothing wrong with going to restaurants, but it adds up quickly so it should be a special, fun outing, not just an impulse based on convenience. Pre-scheduling your nights out to eat with the family and days out at work helps you cut costs. and you’ll actually enjoy the experience more. Try being frugal Monday, Tuesday, and Wednesday, and then start rewarding yourself toward the end of the week.

8. Lower your water heater’s thermostat.

Does anyone else see it as a ridiculous waste of energy that we turn on the scalding hot water and then have to cool it by turning the cold halfway up? Lowering your water heater to the 120-degree setting can save you up to $450 annually.

9. Regulate the heat and air.

About 32% of all energy waste comes from heating and air conditioning, which costs a pretty penny, especially in the cold winters or scorching summers. The biggest problem is that you’re heating or cooling your whole home equally, although you and your family are probably congregating in one or two rooms. So, turn down the thermostat but utilize portable heaters, fans, and even window AC units to save big money on your energy bills.

10. Improve your credit score with Nationwide Credit Clearing – and start saving money!

These days, your credit score is tied to just about every interest rate, loan, and financial account that you hold, which means that improving your credit score is the #1 most effective ways to keep your hard-earned dollars in your own pocket.

To find out just how much a great credit score can save you, contact us at MyNationwideCredit.com for a free report and consultation!

Is your bad credit score hurting your children?

Your credit score has little or nothing to do with your children, you may think. After all, young ones aren’t even aware of what a credit score is for the most part, nor do they concern themselves with the level of your credit card debt or other boring “adult stuff.”

Your credit score has little or nothing to do with your children, you may think. After all, young ones aren’t even aware of what a credit score is for the most part, nor do they concern themselves with the level of your credit card debt or other boring “adult stuff.”

So, even if you’re maxed out on your cards with a sub-par score, it won’t affect them, right?

Wrong. In fact, numerous new studies point to the fact that there’s a direct link between how parents manage their credit, debt, and other money matters, and how children will do the same in the future. Even more important, you could actually be hurting your child in myriad ways if you’re behind on bills and keep a bad score.

“Sadly, your credit doesn’t just affect you, it also affects your kids,” says Michael Banks, founder of Fortunate Investor.

From missing out on private schooling, participation in sports, field trips, getting tutoring, and having a new computer for homework. Braces, trips to the doctor, and other medical needs may go unmet if parents have too much medical debt, not enough funds set aside, or don’t qualify for A+ insurance programs due to their credit scores.

College choices, and especially their choice of universities and later vocation, will be negatively impacted, and these kids will be forced to take on student loans, won’t have co-signers to help them with their first credit card or car loan, and take lower paying jobs out of desperation and need.

“Your children will need you at some point for financial help,” says Justin Lavelle, Chief Communications Officer for BeenVerified.com. “Don’t waste away your financial future and your child’s hopes and dreams because you have sloppy money habits.”

These kids-now-adults will also lack the accurate and unemotional knowledge about debt, savings, and investing. So, point blank, the environment at home around credit and debt matters.

Research also shows that children do pay attention to their family’s finances, but not in ways you may think. Information filters in not in dollar figures and statistics, but in stress levels, perceived anxieties, topics that are taboo, and suggestions about their place in the world or society.

Furthermore, children whose parents have high levels of debt and low credit scores (which is different than just parents on the low end of the wage-earning scale), miss vital opportunities in life that may hinder their potential development as adults.

There even could be developmental or behavioral implications to your high debt/low score burden.

New studies even reveal that children whose parents have certain kinds of financial debt are more apt to have behavioral problems. In a study of 9,000 children ages 5 to 14 conducted by the University of Wisconsin-Madison, researchers found that children of parents with high unsecured debt, such as credit cards or medical bills, were more likely to experience anxiety, emotional stress, aggression, and even depression.

“Growing up in an environment of constant financial worry can cause your children to ‘inherit’ those same concerns and carry them into their adulthood,” says Marc Johnston-Roche, founder of Annuities HQ.

However, it’s worth noting that there wasn’t such a correlation found between secured debt levels and children’s wellbeing. That’s because secured debt tends to go towards more positive and utilitarian purposes, such as getting a mortgage to buy a house, some student loan debt to pursue a degree, or taking out a business loan so the family can improve their financial situation.

Those findings are confirmed by a first-of-its-kind study by Dartmouth College which discovered that how parents handle their credit has socioemotional implications. In their research, children of parents with higher levels of unsecured debt (credit cards, payday loans, and medical debt), were more likely to suffer from “poor socioemotional well-being.”

“High levels of unsecured debt may create stress or anxiety for parents, which may hinder their ability to exhibit good parenting behaviors, and subsequently affect the wellbeing of their child or children,” the study reported.

But there is potentially good news for children when parents do manage their credit – and communicate positively about it. A landmark study conducted by North Carolina State University and the University of Texas concluded that parents who were more likely to sit down and talk with their kids about credit, debt, saving, spending, and earning, even from a young age, give their children a head start for the future.

But, interestingly, the study also found that certain topics were often taboo or off-limits during family discussions about finances, like parental income, investments, and, yes, debt. They also found that parents were more likely to talk with their boys about investing and other matters than with their daughters – a concerning trend.

So, what’s the takeaway?

If you have a bad credit score, your children are statistically far more likely to have bad credit scores as they get older, too. And if you max out your credit cards and carry a lot of “bad” debt, you’ll likely pass that pattern on to your kids. No matter how well-intentioned you are, right now, you’re actually modeling what financial behavior should look like to your children – and they’re learning quickly.

You now have another compelling reason to clean up your credit and right your financial ship: keeping your children out of the same predicament.

Millions of Americans get a credit score boost because of new scoring rules. Will your score go up?

While millions of Americans just filed their taxes in hopes of a big refund, consumers may be getting some good financial news in another arena: their credit scores. That’s because the three major credit reporting bureaus – Experian, Equifax, and Transunion, just reported that they’ll start excluding tax liens from their credit scoring algorithms.

While millions of Americans just filed their taxes in hopes of a big refund, consumers may be getting some good financial news in another arena: their credit scores. That’s because the three major credit reporting bureaus – Experian, Equifax, and Transunion, just reported that they’ll start excluding tax liens from their credit scoring algorithms.

In a concerted effort to improve the accuracy and fairness of their scoring models in respect to public records, a significant number of Americans will see their credit scores jump, virtually overnight (the changes took place April 16.)

The push for reformatting the way judgments and tax liens are factored into credit scoring comes after a study from the Consumer Financial Protection Bureau revealed that incorrect, outdated, or otherwise erroneous information too-often showed up in credit files, sinking that person’s score. So, starting last July, the credit bureaus started their clean sweep of civil judgment data from credit reports, including some tax lien reporting. This April 16, they finished that job.

To be clear, the vast majority of Americans won’t see any difference if they check their credit score again. According to the IRS and other reports, between 93% and 94% of Americans do not have any sort of tax liens reporting on their credit. However, that still leaves about 12 to 14 million Americans that may have tax liens or other judgments affecting their credit score.

The number of people who see a credit score benefit could be even higher. Based on research by LexisNexis Risk Solutions, about 11% of our population will have a judgment or tax lien removed from their credit file.

No matter how you add it up, since the credit bureaus are reshuffling their credit scoring model and excluding tax liens from consideration, these “lucky” millions of consumers will enjoy that sizable score increase.

So, just how high might their scores increase with the new scoring changes?

The answer is “It depends,” of course, because credit scoring is based on a host of factors and individual circumstances (like payment history, status of other existing loans, how seasoned accounts are, and credit mix). While many consumers may see their FICO score up by about 10 points after the April 16 change, a whole lot more could see their score ascend even higher.

For instance, according to a study of 30 million credit files by credit scorer FICO:

• The majority of consumers will see an increase of about 1 to 19 points.

• But between 1 and 2 million consumers may see their scores skyrocket by 20 to 39 points.

• In the case of about 300,000 consumers, their credit scores could go up by as much as 60 points when multiple liens are removed – or more.

But, it’s important to remember that the vast majority of people won’t see any credit score increase at all, as they don’t have tax liens or judgments. Others point to the fact that the 92-93% of consumers who don’t have a tax lien are somehow unduly being penalized because they won’t see their score go up.

Likewise, various financial watchdog groups have gone on record that the changes won’t make a big impact for consumers, at all. According to Eric Ellman, senior vice president of the Consumer Data Industry Association, “Analyses conducted by the credit reporting agencies and credit score developers FICO and VantageScore show only modest credit scoring impacts.”

But wait, is it possible that the credit scoring changes not only make a minimal impact but even harm consumers? “Lenders and servicers have to hedge for that risk,” says Nick Larson, business development manager for aforementioned LexisNexis Risk Solutions. “Overall, consumers actually get hurt,” he goes on, pointing to the fact that banks, lenders, and creditors will have to adjust their guidelines and regulations accordingly (therefore hurting those who didn’t see a credit score increase from erasing tax liens) just to provide the status quo risk-gauging model.

No matter what the temporary impact may be, remember that the best way to maintain a great credit score over the long term – and save thousands on your credit cards, mortgages, loans, and more – is to make your payments on time, keep your balances low, and keep a good mix of seasoned, responsible accounts.

For more help or if you’d like a great credit score increase of your own, contact Nationwide Credit Clearing for a free report and consultation.

How mortgage lenders (or consumers!) can quickly raise a borrower’s credit score.

In recent years, the housing market has benefited from historically-low interest rates, widely accessible to most homebuyers and homeowners even if they didn’t have the highest credit scores.

In recent years, the housing market has benefited from historically-low interest rates, widely accessible to most homebuyers and homeowners even if they didn’t have the highest credit scores.

However, times are ‘a changing, and with interest rate hikes and storm clouds on the economic horizon, it’s not unrealistic to think that we may see a market – and financial – tightening within a couple of years. While loan officers and mortgage brokers have their fingers on the pulse of these changes as they occur, there is one thing that will return to relevancy: credit score.

In fact, when a borrower or home buyer comes to you and applies for a loan, the difference between a 720, 680, or 620 FICO will make a huge difference in what loan programs they get approved for, and the interest rate. Furthermore, your clients will be able to afford more home when buying, save a lot when refinancing, and generally have better options.

But you don’t want to wait six months to a year to organically improve their credit score (nor will they wait around!). Luckily, we have some tactics and strategies that can help improve a consumer’s credit score in short order. In this blog, we’ll bring you the first five strategies, and look for the next five in our upcoming blog.

And you can always contact Nationwide Credit Clearing for more information on how to improve your credit score (or your client’s score) quickly!

1. Pay down balances quickly.

We know that the ratio of your debt to total available credit – called credit utilization ratio – makes up about 30 percent of your credit score. Therefore, people with maxed out credit cards or high debt loads compared to their available credit will see their scores steadily sinking.

So, the first thing you want to do when improving your credit score is to pay down as much debt as possible.

It’s important to get your credit utilization ratio below 30 percent (so you only owe $3,000 or less on a credit card with a $10,000 available balance). Credit experts even suggest keeping a utilization ratio of 10% or less to achieve a great credit score. However, don’t go all the way to 0% because it won’t show an established payment history they can use in their calculations (since you won’t have any payment).

2. Call today and request a credit line increase.

Don’t have enough money sitting around to pay down your credit balances enough to raise your scores? Another sneaky-good way to improve your credit utilization ratio – without paying down one cent of debt – is to increase your total available credit. For instance, let’s say you had a $10,000 credit line but owed $4,000 (so your utilization ratio was 40 percent).

Instead of paying down your debt, if you could get the credit card company to increase your available limit to $15,000 from 10k, your utilization ratio just went down to about 27 percent – and your score would go up! To do this, simply call the credit card company or lender and make your case over the phone and they’ll either approve or deny your request or approve a lesser increase.

3. Remove authorized-user accounts that are hurting their score ASAP.

Many times, a borrower agrees to become an authorized user on someone else’s credit account to help that person qualify for the loan, whether it’s a credit card, an auto loan, or even a business obligation. However, if that person misses a payment or otherwise mismanages that account, the borrower’s negative hit will affect your credit score, too. Thankfully, it’s easy for us to help your borrower remove themselves from the credit account in question. It usually only takes a call to the credit card company or bank with a formal request that they’re removed from the account, as well as the item deleted from their credit report, removing the negative reporting item and improving their score.

4. Consolidate accounts – virtually overnight.

A good number of consumers find themselves with multiple credit cards or accounts from the same bank. Even if the name on the card is different. By consolidating these multiple accounts with the same parent company into one, it may help their credit score take a big jump forward. That’s the case especially if they can consolidate a newer account with an older one, which will then report as a well-seasoned account. However, we do need to carefully mind their credit utilization rate to make sure this move will positively impact their score, but it can really assist some borrowers, virtually overnight.

5. Dispute any errors or bad information on your credit report.

Most people don’t realize that credit reports often contain mistakes, misreporting, duplicate items, or outdated information. All of these things may be lowering your score, but they can also be removed. Start by contacting Nationwide Credit Clearing for a copy of your credit report, and we’ll help you review it carefully for any errors or inaccuracies.

By reviewing it line-by-line, we’ll be able to highlight inaccuracies or items that are lowering your score. Remember that there are three major credit bureaus and they each may report different information, so it might be a good idea to check all three. Look for errors on larger accounts first, length of history, payments reporting on time, and that your balances are accurate.

The last step is formally disputing each inaccuracy or error with each of the credit bureaus, Equifax, Experian, and TransUnion, separately. They are legally obligated to get back to you in a certain amount of time with proof that the information you’re disputing is correct – or they have to change it or remove it.

***

If you have more questions about improving a borrower’s credit score quickly, contact Nationwide Credit Clearing for a free credit report and consultation.

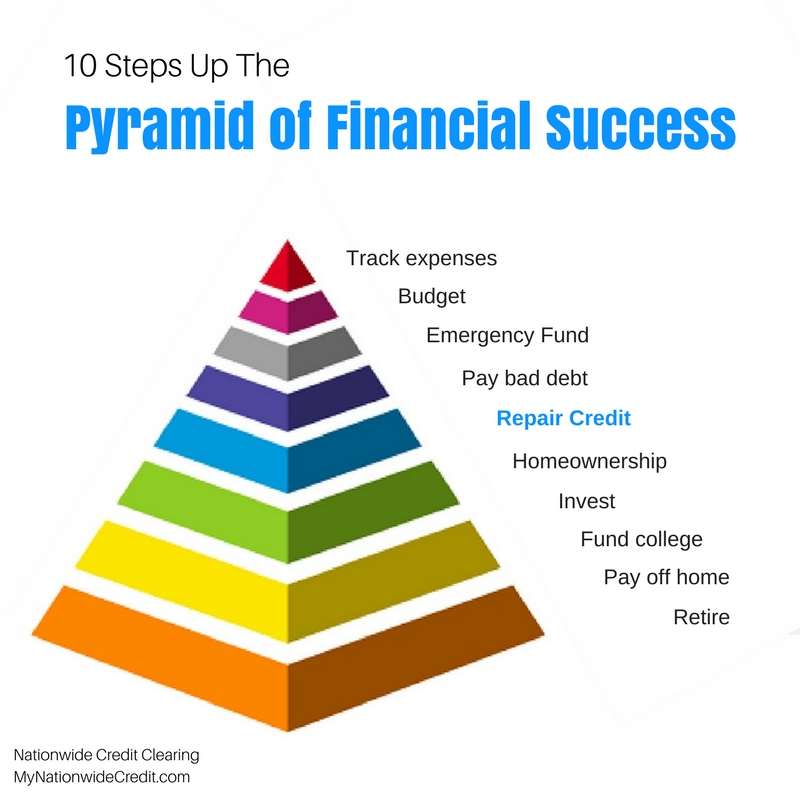

The Pyramid of Financial Success

The Pyramid of Financial Success

The Pyramid of Financial Success

No matter what our financial situations look like, everyone pretty much wants the same thing: low bills, plenty of savings, living in our own home, and enough investments to retire whenever we wish. Achieving that lofty goal is also very obtainable if you follow these 10 steps to climb the Pyramid of Financial Success:

1. Track expenses

Before you do anything else, it’s critical to know exactly how much you’re spending every month, and on what. Sure, you may THINK you know what your bills are and how much you spend, but I bet that you’ll be pretty shocked when you write down every single penny you spend (or use one of the great financial apps that help you record expenses). Try this for a month and then add up the total expenses and you’ll be amazed how much you’re blowing on impulse purchases, things you don’t really need or even want, and items that you didn’t realize are costing you!

2. Set a budget

Now that you know exactly what you’re spending your hard-earned dollars on, it’s time to tighten the belt. Ruthlessly slash everything from your budget that’s not a necessity – and hold yourself accountable to it. This will take some discipline but turn it into a fun game, and keep reminding yourself that by sacrificing NOW, you’ll be able to put yourself in a much better financial situation that lets you spend more on the things you really love and want later on.

3. Build an emergency fund

Did you know that 40 percent of Americans couldn’t come up with $400 in cash if faced with an emergency today, and two-thirds don’t have even $1,000 saved? As we’ve turned to debt more and more, the savings deficit in the U.S. has grown. However, it’s so important that you accumulate a rainy-day fund, which is a fair bit of cash that you can use when the car breaks down, you miss work because of a medical problem, or some other challenge. Start by putting $400 away, then $1,000, and keep saving until soon, you’ll have at least a few month’s total expenses saved as a cushion.

4. Pay debt

This is a big one! Once you’ve set a budget and put aside a few bucks as a safety net, it’s time to tackle the hardest part of all: paying off debt. In fact, the average American household now has $16,883 in credit card debt, $50,626 in student loans, $29,539 in auto loans, and, if they’re lucky, a mortgage on top of all that. But the one that we want to start with is paying off credit cards, as well as other revolving debt and retail installment loans. This is essential if you want to free yourself from a life of struggling and stressing about money and bills, and open up a much more secure and comfortable relationship with money.

There are several ways you can pay off your debt, but one of the best is using the technique of Debt Snowballing which is advocated by financial gurus Dave Ramsey, Suzie Orman and others. We’ll bring you more info on Debt Snowballing soon.

5. Repair credit

In fact, it’s a good idea to tackle #4 and #5 on this list in conjunction so that you’ll end up debt free AND with a fantastic credit score, starting with a free credit report and consultation from Nationwide Credit Clearing. We’ll go over your credit report and debt load with you, identifying which of them should be paid off first since they have the highest interest rates (or smallest balances).

Likewise, we can advise you which of your credit accounts should just be paid down (not off) and kept open. Our service will also attempt to remove negative, incorrect, and outdated items from your credit report, boosting your score to new heights.

How important is a great credit score? These days, just about everything you pay is tied to credit score, from all of your credit cards, your mortgage, and other loans, as well as utilities, cell phone accounts, the ability to rent a home, and even your job!

6. Buy a house

Speaking of (not) renting, once you have some savings and your debt paid off, the next big step in your financial pyramid is buying your own home. In fact, homeownership is still the American Dream, allowing you to build equity, pay down your loan, enjoy lucrative tax breaks, and experience the pride of ownership. These days, down payment programs make it easier than ever to come up with the money needed to buy a house, and you’ll essentially be paying yourself every month instead of your landlord!

7. Invest

Your bad debt is gone, and you’re now in your own home, so it’s time to start investing. Actually, you should be investing from day one in a 401K, mutual fund, or other safe, stable vehicle, as the power of compounding really comes into play the earlier you start. Contact a financial planner or advisor for the best way to invest and save for retirement considering your situation and goals.

8. Fund college

Remember how we mentioned that the average household has $50,000+ in student loan debt? Why not give your children a head start (not extra hurdles) in life by funding as much of their college education as possible instead of piling on more debt?

9. Pay off your home

We paid off your bad debt when we zeroed-out those credit cards, and you’ll get to a point high up the pyramid of financial success where the next logical step will be to pay off your home, too. There are several great strategies to help you do this, such as sending in a 13th payment every year, paying every two weeks instead of monthly, or adding extra funds to pay off principal faster. Either way, once you pay off your home in 20 or even 10 years instead of 30 (like most mortgages), your biggest bill will be knocked off the list.

10. Retire

With little or no debt, plenty of savings, a well-spring of investment income, and your home paid off, you’ll be in the enviable position at the top of the pyramid, where you can choose to retire whenever you like. Of course, that doesn’t mean that you must stop working, as many people opt to pursue their passion or work a lighter schedule just because it’s enjoyable. Either way, you’ll be the master of your financial life – not the other way around! Congratulations on making it to the top of the pyramid!

What the wealthy OVERstand about money that the rest of us may not.

The average person now has more knowledge available to them than any time throughout history, including plentiful wisdom about money, finances, and wealth. However, the income gap keeps growing in the U.S., with the rich getting richer and the typical middle-class family struggling just to make ends meet.

The average person now has more knowledge available to them than any time throughout history, including plentiful wisdom about money, finances, and wealth. However, the income gap keeps growing in the U.S., with the rich getting richer and the typical middle-class family struggling just to make ends meet.So what do the wealthy OVERstand about money that the rest of us may not?

1. Debt is dangerous

The number one principle of money that wealthy people understand is to not misuse debt. In fact, every time you use your credit card to make everyday purchases, you not only spend more than you would with cash (on those impulse purchases). You’re also essentially spending 110, 120, or even 130 cents on the dollar if you factor in interest charges and other fees. Wealthy people pay cash for their purchases and resist the temptation to use debt as a way to afford things they otherwise could not or should not.

Likewise, wealthy people understand that there is good debt (like mortgages, business loans), etc. that helps them achieve assets and investments, and bad debt (credit cards, car loans, etc.) and know how to utilize the former.

2. Your credit score is everything

Let’s say that before you even reached in your pocket and spent a single dollar on groceries, credit card bills, your mortgage or rent, insurance, or any other expenses, there was a number that basically ranked how much or little you should pay for those things. You would probably concern yourself with knowing and improving your ranking so you’d spend less, right?

Well, that’s exactly what credit score does. Rich people understand that credit score dictates so much of what we pay and even opens up remarkable financial opportunities if we have great scores, and therefore, make sure their FICO is fantastic.

3. Compounding and the time value of money

Would you rather have a penny a day that doubles every day for a month, or $1,000,000? Believe it or not, you’d miss out if you chose the quick seven-figure payout, as the first option would yield you $5,368,709.12 in those same 30 days!

Welcome to your first lesson in the time value of money, as your money will grow exponentially over time thanks to the magic of compounding. For that reason, the wealthy aim first to eliminate debt, buy their own home, and obtain assets like stocks, bonds, and other investments that will grow for them over time (more on the ‘time’ part later).

4. Don’t forget about taxes

It’s not what you make but what you keep! What good is a job that pays you $50,000 a year if you give 30% of it away for taxes (for example) when you could have a $40,000 job but pay in a much lower tax bracket? Wealthy people are always aiming to maximize their returns (make more) and minimize their liabilities (spend less) and saving on taxes is a huge part of that.

And when it comes to that yearly tax return you may be getting back, do the right thing with it and pay off debt and put some in savings!

5. Buy a home!

Homeownership always has been (and always will be!) part of the American Dream. It’s not only nicer living in your own place, but the financial advantages are impossible to ignore.

When you ow your own home and pay a mortgage every month, you’re paying off what you owe on the home (over 30 years), so it’s sort of like a forced savings plan.

Likewise, homes have appreciated in value over any 10-year period throughout modern U.S. history, so purchasing a home early and paying it off allows you to retire without having to pay mortgage or rent (and then you can leave it to your children). Likewise, owning a home offers one of the biggest tax breaks you’ll ever get from Uncle Sam, too.

Meanwhile, the alternative is to keep paying rent to your landlord every month, which yields you no appreciation, you’re not paying anything down or building any equity, and you’re missing out on tax breaks. The wealthy aim to be landlords; not pay a landlord!

6. Save first

Sure, we know that when your paycheck arrives once or twice a month, it’s probably already spent and accounted for before you can even cash it. But wealthy people become that way by making sure they save first. In fact, most financially stable people utilize auto-withdrawals from their paychecks to put some money into savings, pay bills, and maximize their investments – before they even see any money from their paycheck. Doing so takes some discipline and sacrifice, but the results will pay off big-time!

7. Education never ends

We all have 24 hours in every day, but instead of gossiping, wasting time arguing on Facebook, and watching funny cat videos, wealthy people invest their time in learning and growing. That can be learning new job skills, going back to school for another degree, or just reading, listening, and watching inspirational and educational messages. Of course, many of those are about improving their finances, so pat yourself on the back for reading this blog!

***

If you’d like more information about credit, debt, and putting yourself in a better financial position, contact us for a free consultation and credit report.