-

-

Quick Contact

Get A free

Consultation Now!

loan

10 Ways to Start Saving Money TODAY!

Do you want to save money?

Do you want to save money?

Of course you do!

In this ongoing series, we’ll point out effective ways you can save a lot of money this year, next month, and even today!

Here are our first 10 ways to start saving money today:

- Cut down on beverage costs.

Did you know that the average American spends about $650 a year just on soda and soft drinks! For a family of four, that adds up to $2,600 – enough to pay off a credit card or put aside for savings, perhaps. Add in bottled waters (when you could just bring your own reusable bottle and fill up at water coolers), energy drinks, and expensive coffee drinks (more on that later), and you may be able to save $300 or $400 every month just by watching what you drink!

- Compare homeowners or renters insurance policies.

Most families purchase a homeowners insurance policy, pay the high premium, and forget about it. But it’s a good idea to contact your agent every six months or so, just to check in if there are new programs, specials, or lower rates available. It’s also prudent (and free!) to shop around a little and see if you could save significant money with another company or agent. Something as simple as installing new smoke detectors, adding an alarm system, or other health and safety upgrades may qualify you for a discount.

- Shop around for a better auto insurance plan.

While you’re at it, contact your insurance agent and ask him or her if there are better deals available for your auto insurance. You may get a discount for signing up with a company that holds your other insurance policies, too. Or, if your driving record has improved (or just stayed uneventful), you live or work in a different zip code, or your credit score has gone up, there may be a price break you’re not currently taking advantage of.

- Hit the OFF switch on electronics and appliances.

Sure, we know to turn lights off when we leave a room and shut off the TV before we leave the house. But even when you’re gone and things are supposedly off, certain appliances still drain a lot of electricity – and run up your energy bills. In fact, toaster ovens, coffee makers, mixers, kitchen radios, some microwaves, cable boxes, video game consoles, and other entertainment systems and appliances STILL draw electricity even if they’re off. As a general rule, if an appliance has. LED light or digital display, unplug it – don’t just turn it off – and you’ll start saving.

- Install a new SMART thermostat.

Heating and cooling costs add up big for most homeowners, whether you live in a place with the coldest arctic-like winters (hello, Chicago!) or sweltering, humid summers (hi again, Chicago!). But most home heating or cooling systems are outdated – and their thermostats are wildly inefficient, too. You don’t have to replace your whole HVAC system to save money, but switch out your old thermostat for an energy-efficient smart model.

In fact, a new Energy Star thermostat allows you to program specific temperatures for different times of the day. You can even program it higher or lower based on different zones of the house or adjust for when you’re not home. How much money will that save you? The U.S. Department of Energy estimates that you can cut back on energy costs by up to 15% per year just by getting a smart thermostat!

- Bundle your cable, internet, and phone services.

It’s ridiculous home much the average person pays for cable TV, Wi-Fi at home, home phone, and cell phone service every month. While you may not think you can live without all of those, you may be able to save a pretty penny just by bundling your services. In fact, most telecom companies are so motivated to get your business (and keep it), that they’ll give big discounts and special pricing for consumers that sign up for all of these services with them. Just by calling around and comparing bundled packages and offers, you may save $100 a month or more!

- Take a close look at your memberships and subscriptions.

From monthly magazine subscriptions to membership clubs, internet sites that require a monthly fee and smartphone apps with recurring monthly payment. In fact, the average household pays $129 in memberships and subscriptions like this every month! That’s well and good if you use them and like them, but most of us don’t even realize all of the things we’re paying for! Take a careful look at all of your memberships, subscriptions, and online recurring payments, cutting the fat where necessary

- Cut out those ATM fees.

The average American spends at least $290 in ATM fees every year. That’s not banking fees, but just the cost to access their own money at ATM machines. In fact, the average out-of-network ATM fee is now $4.52. There are even ATM operator fees of $2.50 to $3 for non-members, and steep international fees. Some opportunistic banks even charge ridiculous ATM fees based on location, such as many Las Vegas money machines that charge $10! In total, you may be wasting $30 or $40 every month in your household just by using the wrong ATM and the wrong bank.

- Pack your lunch most days of the week.

Of course, everyone loves to eat out when they’re at work. But the cost really adds up. Let’s do the math – if the average brown bag lunch costs about $4, but going out to a restaurant, sandwich shop (or even fast food) comes to about $9 a meal, you’ll be saving $5 a day by not eating out. Add that up over 20 working days, and you’re at $100 savings a month, or $1,200 a year. However, realistically, you probably spend more on nicer sit-down restaurants, tips, beverage costs, snacks, etc. So make it a policy to brown bag it Monday through Thursday and then splurge on Friday. You’ll save a lot of money and not feel you’re missing out!

- Request that your credit card companies lower their APRs.

Credit cards will often reward good customers with lower APRs, reduced interest rates, or by fixing a low interest rate if you’re currently paying a variable rate. It doesn’t hurt to call them and ask for some sort of better terms, rate, or savings. The worst they can say is “no!” But if you’ve paid on time and they value your business, they’ll often do something to keep you. Do this for all of your credit cards, and you may start saving significant money every year!

- Know your credit score.

About one-third of Americans have no idea what their credit score is right now, and nearly 45% of us haven’t checked our score or report in the last twelve months. That lack of attention can cost us big money. In fact, errors, inaccuracies, duplicates, and even ID theft cost American consumers countless millions of dollars each year.

To make sure you save as much money as possible, pull your credit report at least three times a year.

***

Contact Nationwide Credit Clearing for a free credit report and consultation to make sure you aren’t overpaying!

25 Facts about the U.S. auto industry (including how a good credit score will save you a lot of money when buying!)

Since 1908 when Henry Ford rolled out the first Model T from his Detroit production line, America has been one of the world leaders in manufacturing and selling cars.

Since 1908 when Henry Ford rolled out the first Model T from his Detroit production line, America has been one of the world leaders in manufacturing and selling cars.

Here are 25 facts about the auto industry – including car loans and how a good credit score can save you a lot of money when buying!

1. In 2017, we bought a lot of cars! In fact, 6.2 million new cars were sold, as well as 11.1 million SUVs and light trucks, adding up to approximately 17.3 automobile transactions.

2. Considering that there are approximately 323 million people in the United States, that means more than 1 out of every 18.6 people bought a brand new car…just this year!

3. While those numbers are impressive, they’re slightly off of the high point of auto sales in 2016, when nearly 17.5 million light passenger vehicles sold, as well as 17.4 million in 2015.

4. Worldwide, 78.6 new cars sold in 2017!

5. In 2017, the motor vehicle industry (including manufacturers, dealerships, used part dealers, service centers, etc.), employed almost one million U.S. workers (approximately 940,000).

6. In fact, the auto industry is responsible for about 3 to 3.5% of our entire U.S. gross domestic product.

7. We also manufacture a lot of cars in the United States these days. In fact, nearly 12 million light passenger vehicles were built in the good ‘ole U.S. of A last year.

8. At least 2.1 million of those automobiles were exported and sold abroad, spanning almost every country in the world for a total value of $57 billion.

9. Additionally, the secondary automobile parts export market is worth an impressive $80 billion, and we also exported $5.5 billion in used cars.

10. While that’s a whole lot of new cars, the U.S. is still second to China for automobile markets, both in terms of sales and production.

11. Of course, a lot of car sales mean a lot of car sales dealerships. In fact, there are currently 18,250 new vehicle dealerships in the United States.

12. According to government estimates, there are about 222 million licensed drivers in the United States, which means that about 69% of our country has a driver’s license.

13. We also know that there are approximately 260 million passenger cars, trucks, and SUVs on the roads, which adds up to 1.24 automobiles for every person with a driver’s license in the U.S.!

14. In fact, there are 260,350,940 registered vehicles in the United States, which is an all-time high.

15. That also accounts for 20 million more automobiles than 2007, and in 1990 there were only 193 million registered autos in the U.S.

16. But the car market is still heating up around the world, with new car dealers expected to bring in 916 billion by 2020, with used car sales following with 106.6 billion in sales.

17. An interesting data point is the Scrappage Rate, which measures the number of cars sent to junkyards and put out of service every year. Over the last couple years, the Scrappage

18. Rate fell to only 11.5 million annually, a record low when compared to the number of cars on our highways and roads.

19. If we look at the monthly budget of the average America, their rent or mortgage payment tops the list, but transportation costs (including car payments) comes in second.

In fact, when added together, housing and transportation account for about 50% of the typical American’s income.

20. The average American’s monthly spending chart looks like this (based on a $51,442 per capita): income:

33% Housing, $16,887

17% Transportation, $8,998

13% Food, $6,599

11% Insurance, $5,591

7% Health Care, $3,556

5% Entertainment, $2,605

3% Clothing, $1,736

11% Total other expenses, $5,470

21. While we may be buying new cars at record rates, we’re still using financing to purchase the vast majority of them. In fact, in 2017, auto lending hit a new record with more than $1.1 trillion in car loans owed by consumers!

22. In fact, the average person with a car loan now has $18,694 in auto debt, and the average new car came with a sticker price of about $35,000 in 2017.

23. But last year, the average person who financed their car purchase borrowed $30,032 in loans (the first time that average exceeded $30,000). The average monthly payment for a new car loan is now $503, the first time that number has risen over $500.

The average loan term is now 67 months (5.58 years) for new automobiles and 62 months (5.16 years) months for used autos, both record highs.

24. However, car loans are being extended to people with marginal or even poor credit scores like never before. These days, almost 20% of all auto loans go to people with credit scores of 620 or less – called “subprime” (a score of 680 is typically considered good.)

According to Experian, 19.3% of auto loans now go to consumers with subprime or deep subprime credit scores. That means less than two-thirds of auto loan borrowers (61.3%) have prime or super-prime credit.

25. There’s no denying that it’s a great feeling to buy a new car, and reliable transportation is a must for most of us. However, subprime auto loans tend to come with sky-high interest rates and cost us way too much in total interest. For example, a person financing a $23,000 car might spend $9,615 just in interest with a 66-month loan at 14.99 percent!

***

So, in order to get a great car loan, have a better monthly payment, save a lot in total interest, AND get that beautiful new car you love (and deserve), talk to Nation Wide Credit Clearing first about improving your credit score!

Just how much money will you save with a good credit score? The answer may shock you!

Most people don’t think about their credit score on a daily basis, even as they use their credit cards, make their auto loan payment, or write a sizable check for their monthly mortgage. However, there’s a direct correlation between a good credit score and saving on all of these accounts – and more.

Most people don’t think about their credit score on a daily basis, even as they use their credit cards, make their auto loan payment, or write a sizable check for their monthly mortgage. However, there’s a direct correlation between a good credit score and saving on all of these accounts – and more.

The top credit scorers typically save tens (or even hundreds!) of thousands of dollars over their lives, helping them pay off debt, amass savings, invest to retire comfortably, or achieve their other financial goals.

Meanwhile, consumers with subprime or even average credit scores get charged higher interest rates, fees, and see a lot of doors closed when they apply for new loans.

So how much money will a great credit score actually save you? Let’s take a look:

Credit Cards:

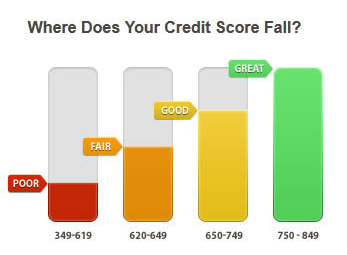

According to Bankrate.com, if your credit score falls between 600-679, the average U.S. credit card APR (annual percentage rate) is 22.9%

But if your score is in the 680-739 range, your APR drops significantly to 17.99%.

However, for the highest credit scores in the 740-850 range, the average APR is only 12.99%.

So how much can those lower credit card interest rates save you?

Looking at a popular tiered credit card with a $10,000 balance as an illustration, we see that with the lower 12.99 percent APR for high-score consumers, the monthly payment would be $297 for over five years to pay it off. But if you had that that higher 22.9% rate because your credit score was mediocre, that monthly payment would jump up to an astronomical $715…and for more than 7 years!

Therefore, keeping a great credit score could be the difference between paying $18,414 total to pay off this card or $44,330 – a whopping $25,000+ savings!

Auto financing:

When it’s time to purchase a car and apply for auto financing, your rates and terms can vary widely. But one thing is for sure: a great credit score will save you a lot of money when you’re paying off that shiny new auto month-after-month.

According to VantageScore, which is the main purveyor of credit scoring for auto lenders, a typical $25,000 auto loan for a 5-year term:

- Below 550 Vantage Score (poor credit): 18.9% with $13,828 interest paid

- Below 620 score (subprime credit): 17.9% with $13,009 interest paid

- 620 to 680 credit score (average): 11% with $7,614 interest paid

- 680-740 credit score (good): 6.5% with $4,350 interest paid

- 740-850 credit score (excellent): 5.1% with only $3,375 interest paid

While a 760 is considered a top-notch credit score for mortgage lending, you’ll probably qualify for the best auto financing with a 720 or higher score. In fact, consumers with excellent credit scores may even qualify for 0% financing on new car purchases.

Mortgage:

One of the biggest ways your credit score will save you huge bucks is when it’s time to buy a home. And unless you’re paying cash for that home, you’ll be applying for a home loan, with rates and pricing based heavily on credit score.

Assuming that the average sales price of a house is $343,300, with a mortgage of $274,640 (20% down payment) and a 30-year fixed mortgage:

Let’s start with a 5% interest rate just for illustration purposes (historically, that’s low, but right now it could be a little high):

Your monthly payment will be $1,474

Total payoff over 30 years is $530,758 (interest and principal payments)

But if you have a better-than-average credit score and qualify for a 4.5% interest rate on that same loan, your monthly payment will be $1,392 with a total payoff of $500,962.

And if you have a great credit score that grants you a 4% interest rate, that means you’ll only pay $1,311 per month with a $471,960 payoff

So how much will a good credit score save you when it comes to this typical mortgage illustration?

-Savings in 1 year (compared to a 5% rate)

4.5% $984

4% $1,956

-Savings in 5 years

4.5% $4,920

4% $9,780

-Savings in 10 years

4.5% $9,840

4% $19,560

-Savings in 30 years

4.5% $29,796

4% $58,736

And for a $500,000 home, the difference between a 760 and a 620 credit score could cost you about $150,000 or more in additional interest payments due to higher rates!

In fact, according to Michelle Chmelar, the vice president of mortgage lending with Guaranteed Rate, every 20-point step down from a 760 credit score could cost the borrower 25 basis points when it comes to pricing, as well as higher fees and closing costs.

Other ways a good credit score will save you money:

Qualify for the best credit cards:

With a top score, you’ll have the best credit cards jockeying for your business, offering the lowest interest rates (sometimes even 0% for a period), options for low or no annual fees, and great perks and rewards. The credit card companies will also gladly extend you higher balances. Together, this can save you hundreds of dollars every year.

Better car insurance deals:

You may not have known that car insurers also rate and apply coverage based on credit scores. While some states, like California, Hawaii, and Massachusetts, don’t allow car insurance companies to look at credit, in most states, you’ll see much lower premiums with a better credit score – saving you money.

Cheaper cell phone plans:

If you’ve walked into a store recently to buy a new cell phone, you were probably asked to authorize a credit score check. In fact, cell companies will require a hefty security deposit and might even charge you higher rates – or outright deny you a contract – if you have enough blemishes on your credit report.

Get approved for rental housing and apartments:

Most landlords include an authorization for a credit check when you submit an application, and your payment history is a pivotal factor in approving you for a lease. Likewise, if you have judgments from past landlords or collections from utility companies on your credit history, you can probably kiss your chances of getting that nice apartment goodbye.

Utility bill savings:

When it’s time to sign up for a new electricity, heating, water, or trash account, a bad credit score can cause some serious problems, In fact, most utility companies will charge increased security deposits – sometimes hundreds of dollars – for bad credit consumers.

Make the grade with student loans:

The average college graduate now leaves school with $37,172 in student loan debt, an increase of 6% (or +$2,200) over just last year. You better believe that a great credit score will help you qualify for lower-interest student loans!

Don’t miss out on your dream job:

A bad credit score can hurt you in ways that have nothing to do with taking out a loan. In fact, employers are screening their potential employees for credit score, especially with government jobs or those in the financial sector. It’s estimated that 1 in 4 Americans have been subjected to a credit score check when applying for a job, and 1 in 10 have actually been denied a job because of a bad score or something on their credit report!

***

Are you ready to start saving money? Let’s start with your credit score! Contact us for a free consultation and credit report.

6 Financial Mistakes Young People Make

Whether you just graduated from college or are moving out on your own, it can be hard to keep track of your personal finances as a young adult. Read through these 6 common financial mistakes and learn how you can avoid them.

1. Not Taking Advantage of Discounts: There is a world of special prices for students and young people out there, from banks to movie theatres – take advantage of them! Do your research beforehand, find out what discounts are available to you. Check out Groupon or Retail Me Not.

1. Not Taking Advantage of Discounts: There is a world of special prices for students and young people out there, from banks to movie theatres – take advantage of them! Do your research beforehand, find out what discounts are available to you. Check out Groupon or Retail Me Not.

2. Misunderstanding Credit Cards: Whether it be cash advances, large balances, late fees, or only playing the minimum balance, credit cards can lead to much more trouble than realized. The fine print and details of credit cards are often times misunderstood by young people. Read into what you are signing up for and ask plenty for questions when you do not understand something.

3. Signing Up For A Rental Or Mortgage That Is Too Expensive: Signing a lease for rent or applying for a mortgage that leaves you with little money to do anything else, will not only leave you at home but put you at risk for debt. You have no cash at hand, so what do you do? Sign up for credit cards to make up the difference in order to enjoy your lifestyle and pay for unexpected costs. Avoid making this mistake, sign up for a lease or mortgage that is within your budget in order to avoid creating debt for yourself.

4. No Rainy Day Fund: Setting aside money for emergencies gives you cushion for unexpected events and helps you avoid adding to your credit card balance. Maybe your car got towed, or you get injured, having a “rainy day” fund keeps you prepared for the most unexpected events. Including a “rainy day” fund as a part of your budget, will eventually help the money add up.

5. Failure To Realize How “Little Things” Add Up: Your daily coffee stops, eating lunch out, or weekly shopping trip of $100, can all add up to thousands of dollars a year. Cutting back can help you save a lot of money for savings, retirement or paying down your debt.

6. No Financial Planning Or Budget: Some young people are tainted by the idea that saving for the future is only for people thinking about retirement. Everyone can benefit from financial saving whether you are planning for retirement, purchasing a home, or traveling around the world. It is also important to budget your daily expenses. Sit down and look at what is left after your wages and fixed expenses. Not knowing how much you have can easily lead to spending more than you can afford. A budget will help you determine what you need to do to pay for your next vacation.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

Can I get a Home Loan with Bad Credit?

The answer is: YES

To be quite honest, though, it’s not going to be easy to get a loan if:

- Your Credit Score is Low

- You Have Late Payments

- Derogatory Items on your Credit Report

- Excess Debt

- Anything else Related

Don’t get discouraged because there is a solution. Depending on your personal situation, it may take some work on your part to make your dreams happen, but for piece of mind, even if your credit is bad, the possibility of getting approved for a mortgage is there. You just have to take the correct steps and actions that will allow you to get approved. Below is some interesting information:

GUIDELINES FOR PEOPLE WHO HAVE CREDIT ISSUES BUT ARE TRYING TO GET A MORTGAGE:

If you have recently or in the past been denied for a mortgage, Nationwide Credit Clearing can help. We have been helping people remove negative items from credit reports for over 20 years. If a mortgage broker has a client that cannot get approved, often times they will send their client to Nationwide Credit Clearing, we will take the appropriate actions to help increase their client’s score, and send them right back through the approval process knowing that this time the end result will be different.

Just as well, if you are looking into getting a home loan, but are not in the process because you are afraid you may get denied, you will want to contact Nationwide Credit Clearing initially. We offer absolutely free no obligation credit report and consultations for all new or potential clients.

If you or someone you know is having a hard time getting approved for a home loan, contact us today.

After all, we are ” The home of the free Credit Report and Consultation”

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

CLICK BELOW FOR YOUR…

![]()

Why Is My Overall Credit Score Important?

What Is A Credit Score?

A credit score is a three-digit number, typically between 300 to 850, which credit bureaus calculate based on information in your credit report. It is a simple, numeric expression of your credit worthiness. Although the three credit reporting bureaus (Equifax, Experian, and Trans Union), use similar methods to determine a credit score, the formulas they use are not exactly the same and your credit score will vary from bureau to bureau.

How is My Overall Credit Score Calculated?

Your credit score is calculated based on a number of factors listed in your credit history that describe components of your financial life including the number and type of credit accounts you have, the amount of available credit, the length of your credit history and your payment history. Each of these factors is assigned a numerical value, and then weighted based on how prominently they affect your credit worthiness.

How Do My Actions Impact My Score?

The good news is that no matter where your credit score is today, there are a number of different steps you can take now that can change your credit history and help impact your credit score. You should take all the steps you can to help establish a good credit score.

Why Should I Check my Credit History and Overall Credit Score?

In today’s digital economy, your credit history and credit score are vital pieces of information that are key to helping you secure your financial life. Credit card companies, mortgage lenders, and insurance companies will pull copies of your credit report and score in order to decide whether to extend credit or how much to charge for your insurance premium.

Financial services companies tend to group borrowers into segments according to their credit score. These credit score ranges may determine how much you’ll be charged for your insurance coverage or the interest rate you pay on your mortgage, student or car loan or the type of credit card you’ll be offered.

If you haven’t checked your score lately, or have interest in improving your overall credit score, contact Nationwide Credit Clearing.

We offer Free (no credit card required) consultations after we pull your free credit report. Contact us Today!!

Can’t get a loan because of low credit score?

If you have a low credit score or credit problems as a result of declaring bankruptcy or foreclosing on a home, or if your credit scores have dropped because of late payments or failure to pay, do not despair.

Although a good credit score can drop very quickly, at times taking a hit of as much as 150 points or more, it is possible to improve your credit over time and to qualify for a new mortgage loan. Boosting low credit scores is not the only means for people with deficient credit to get a home loan. The Federal Housing Administration (FHA), in an effort to promote homeownership, has made it easier for people with a damaged credit history to qualify for a mortgage loan. Under certain circumstances, people who have foreclosed or declared bankruptcy can obtain an FHA loan several years earlier than a conventional loan, and these people can buy a home with a smaller down payment.

Credit Scores & Lenders

Credit scores indicate to lenders how well you manage money. You can improve bad credit by demonstrating that you can now handle money more responsibly. Furthermore, since poor credit scores translate into high interest rates on home loans, an improved score will help you get lower interest rates when you are ready to qualify.

How to improve credit scores to qualify for a loan

Here are a few ways people with a negative credit history can raise their credit scores and ultimately obtain financing for a new mortgage loan:

- Improve payment history by making payments on time

- Do not open new lines of credit Use credit cards sparingly, and without overextending credit lines

- Make payments in full Have up to four different kinds of credit accounts

- Show evidence of steady employment for a period of one to two years

- Come up with a budget plan and stick to it

- Build up savings

Insider’s tip: Credit experts advise not spending more than 25 percent of your available credit on any credit card account. If you have a $1,000 maximum in a given account, the balance should not be more than $250-$300. Better yet, wipe the slate clean and carry no balance whatsoever.

Other options to consider

Credit Repair? Nationwide Credit Clearing can help you eliminate any incorrect or negative items on your report, ultimately allowing you to qualify for that home loan.

Give us a call today.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail:support@mynationwidecredit.com