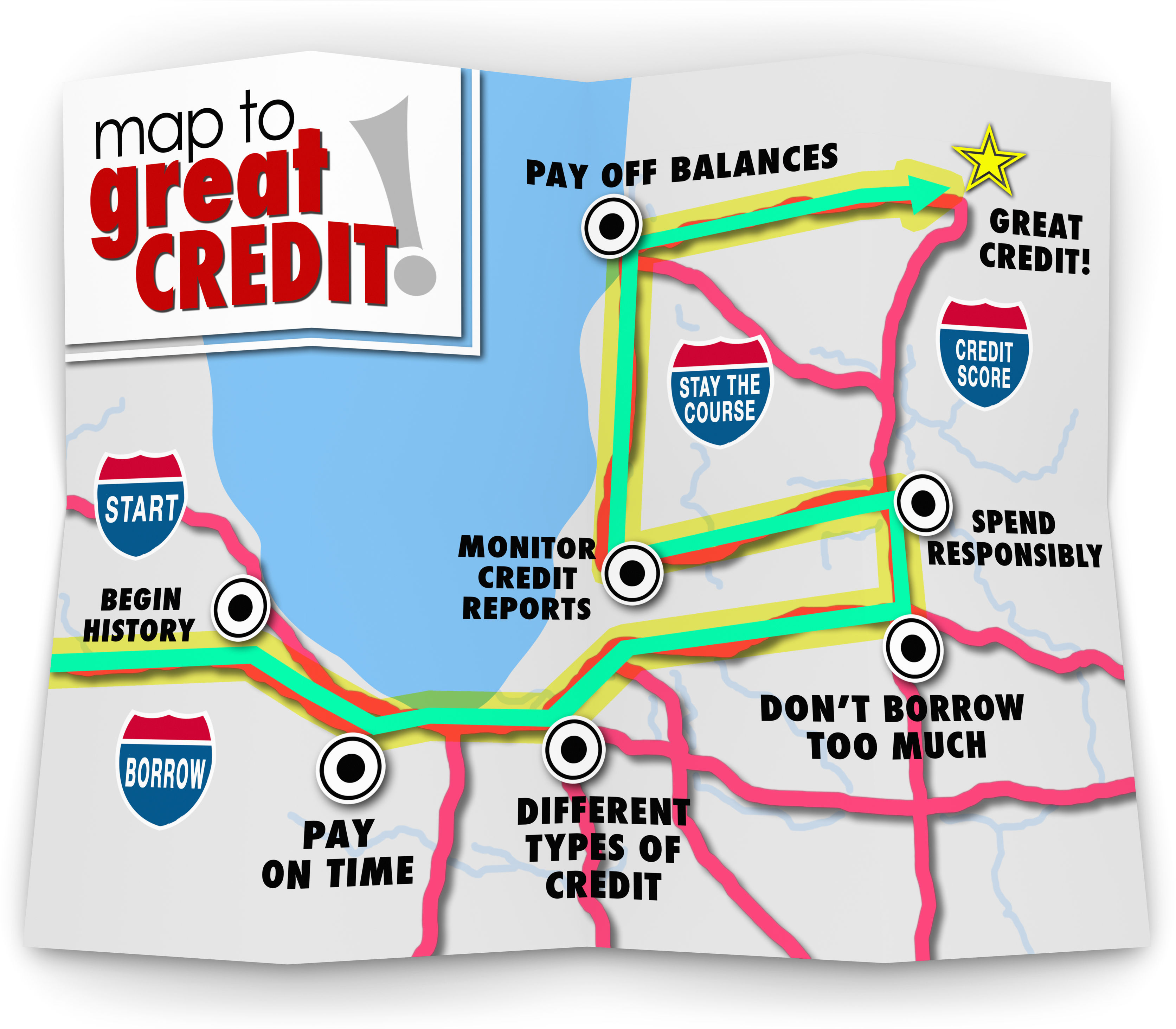

What are derogatory items?

Derogatory items are significantly damaging marks that show up on credit reports as a result of poorly managed credit scores or identity theft. Measures such as late/skipped payments can ultimately lead to the existence of derogatory marks on your reports. Each mark corresponding to a particular circumstance or outcome. Below are a few examples of several key derogatory items you should know about:

Charge-off: A charge-off is one of the worst marks a person can get on his or her credit report, as they happen when a lender determines that someone isn’t able (or unwilling) to pay off a debt they’ve been delinquent on for many months of payments. Although the lender determines the borrower is unable to pay, the lender is still able to legally demand payment entirely for as long as the state’s statute of limitations allow. It needs to be noted that it’s possible for charged-off financial debt to be settled for under its full worth, but credit reports will often note that the debt was not paid in full should this happen.

Collections: Sometimes debt goes to a collections bureau after a lender or service fails to receive payments. With this designation on your own credit report is quite severe; it is possible to work with a collections agency to make paying the money a bit easier. You can also negotiate conditions on your mark to disappear from your information completely once you make the agreed-upon payments.

Court Judgement: Judgements make reference to civil court rulings typically made against one person who owes money to someone else (similar to a lawsuit from a creditor or any other lawsuit regarding money). Since judgements are a case of public record, they could easily show up on credit reports.

Default: A default, particularly on certain kinds of loans (home, student, car), can create a serious problem on credit reports. Oftentimes, a default can be a precursor to several of the other items on this checklist, as it is one of the very first derogatory items that will show up on a past due individual’s credit report. For example, a default might appear onto your credit reports prior to the account being sent to collections. This is why it is extremely crucial to take non-payments seriously and address the problem that caused them right away.

Repossession: Repossession typically occurs when you default on a secured loan, i.e.. You presented something in collateral. If this occurs, everything you offered as collateral for this loan will be taken by way of the lender. This most frequently happens for mortgages and car loans, where the car or home you purchased with this loan is taken away. It’s worth noting that if the current amount of the repossessed item does not cover the entire remaining account balance on this loan, you might still be on the hook for future payments. These things are in no way an exhaustive list of derogatory marks; however they are several of the worst and most damaging, which is why you need to be aware of them.

How can I tell if my credit reports have derogatory marks?

The easiest way to find out if your credit reports include any derogatory marks would be to check your credit report & score. If you do not already know, federal law enables you to get one free copy of all the three of your credit reports – Equifax, Experian, and TransUnion – one time per year through most online services.

Can someone really improve their credit after receiving multiple derogatory marks?

If you do have any of the neg marks mentioned above, do not give up hope. While none of these issues is good for your credit, in time they will eventually just go away. Most derogatory items merely remain on your credit report for about 7 years, along with some having the potential to disappear even sooner. As your credit history grows, the weight that these items are specified also decreases, even if they are still physically found on your report. In addition, there is a whole lot that you can do to start building your credit again nearly immediately. Considering that most of these marks are the direct result of failed payments, working out a payment strategy to pay off any balances is a solid initial step toward restoring your own personal credit.

If you struggle with this, we encourage you to take a look at our top quality X5 Credit Repair system, exclusively from Nationwide Credit Clearing. If you or someone you know has derogatory items on their report, ones that should be disputed, please give us a call. We have been helping people for 28 years improve the quality of their lives simply by working with Nationwide Credit.

Money cannot buy happiness, but it sure makes living life a lot easier. Don’t Wait, Call Now!

Nationwide Credit Clearing

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

follow us on…