-

-

Get A free

Consultation Now!

credit score

How men and women differ when it comes to credit and debt.

How men and women differ when it comes to credit and debt.

How men and women differ when it comes to credit and debt.

There are some profound differences between men and women when it comes to men and women, from what we earn, to what we spend our money on, and even how we go about investing. When it comes to credit and debt, there are some interesting comparisons between males and females, too – although it might not always be what you think.

For instance, when it comes to credit score, would you guess that men or women are leading the way with better scores?

In fact, according to surveys by Experian, women have a higher average credit score (675) than men (674).

Men have more debt, with an average of $26,227 compared to $25,095 for women.

The average man owes $5,282 in credit card debt, compared to only $4,867 for women in credit card balances.

Women have 4.1 credit cards on average, while the average man only carries 3.7 cards.

But at least part of that debt total for men can be attributed to home loans. Of all people who are mortgage holders, men have an average of $187,245 in home loans compared to $178,140 for females.

In fact, the average U.S. man has $50,425 in mortgage debt versus only $35,116 for the average American woman.

Another check in the “Men” column is that 60% of men have more savings than credit card debt, while only 49% of women have more in their savings account than their credit card balances.

While both sexes sometimes exhibit less than stellar use of credit cards, women lead the way in a metric called “problematic behaviors” when it comes to cards.

In fact, only 33% of men display two or more problematic behaviors with credit card usage, compared to 38% of women.

But men carry a larger total of debt than women (+4.3%), and females also use only 30% of their available credit, while men use 31% or higher on average.

Men comparison shop for better rates and terms on their credit cards more than women (37% to 31%).

Women also carry a bigger balance from month to month on their cards (60% do so) compared to men (55%).

And 42% of women only make the minimum payment every month, compared to only 38% of men (a big no-no for your credit score).

Backing up that statistic, 45% of men pay their balance in full every month, compared to only 39% of women.

Women also pay late fees on their credit cards far more than men, at a rate of 29% (of women who have to pay late fees) versus only 23% of men.

Despite having lower credit scores (slightly), men also have better interest rates on their credit cards than women. In fact, the average rate for men is 14.3%, compared to 14.9% for women’s credit cards.

How about student loan debt? On a per-student basis, women have far more student loan debt than men. In fact, the average woman has $11,786 in student loans, compared to only $8,187 for men.

But men finance far more for their cars, with an average auto loan tally of $8,249, while women only owe $6,693 on their car loans on average.

While the one-point credit point advantage favors women by a small margin, the data reveals that women do have a better understanding of credit scores and credit reporting. The Experian study concluded that:

48% of men incorrectly believe that marital status factors into credit scores, compared to only 38% of women who mistakenly think the same thing.

46% of men mistakenly think marital status is a factor in scoring, versus only 34% of women who get that wrong.

74% of women understand that the credit bureaus collect the information that’s used for scoring, while only 68% of men realize that.

Women are more apt to know when scores are free (65%) than men do (60%), know when lenders are mandated to discloses scores (53% to 46% for men), and better understand the importance of regularly checking and monitoring their credit reports (77% to 72% for men).

***

So which gender wins the title of “Best with Credit and Debt?” It seems like women win out over men on average in certain important factors, but men are profoundly better in a few others. Overall, well call it a tie and just say that BOTH men and women need to work hard, educate themselves, and do better with credit and debt if they want to improve their finances and get ahead!

And you can start with a free credit report and consultation from Nationwide Credit Clearing! Contact us to get started.

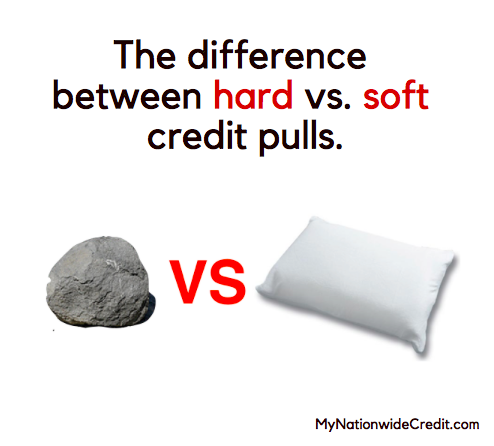

The difference between hard and soft credit inquiries.

Most people check their credit periodically, such as when they’re about to apply for a big loan, once a year, or every four months (like you should). But you may not realize that a whole lot of others are checking your credit – and probably on a more frequent basis. In fact, every time you apply for a credit card, submit an application for a student loan, take out a store discount card, or even apply for insurance or rent a new apartment, your credit is probably being pulled.

Most people check their credit periodically, such as when they’re about to apply for a big loan, once a year, or every four months (like you should). But you may not realize that a whole lot of others are checking your credit – and probably on a more frequent basis. In fact, every time you apply for a credit card, submit an application for a student loan, take out a store discount card, or even apply for insurance or rent a new apartment, your credit is probably being pulled.

Those credit pulls also can ding your credit score, if not handled correctly. Sometimes, that’s inevitable, and other times it’s avoidable. But it’s important to understand the facts about hard and soft credit inquiries, or credit “pulls.”

In fact, only 26% of women and 31% of men know the difference between “hard” and “soft” credit inquires, or credit “pulls.”

So today, we’ll give you some fundamental information about credit inquiries, both hard and soft. Contact Nationwide Credit Clearing if you have further questions about credit pulls, and would like a free copy of your credit report and consultation with a credit expert!

Hard credit pulls:

Hard credit pulls only take place when you apply for new credit accounts.

Or, a hard pull will occur when one of your existing creditors decides to pull your credit. In fact, most creditors can access your credit any time, for any reason they deem, without needing your permission first.

Creditors commonly do this when they’re reviewing your account to consider an increase to your credit line.

Soft credit pulls:

Sofer credit pulls, however, can occur either with inquiries where the consumer voluntarily agreed to have their credit accessed, or other involuntary inquiries.

For instance, soft pulls usually take place when you’re applying for a new job, a cell phone account, trying to rent an apartment, etc.

Effect on credit score:

There is no one set rule for how credit pulls will affect your score. But, typically, hard credit pulls will only have a slightly negative impact on your credit score, possibly dropping your score a few points in the short term.

Typically, your FICO score can go down about 5 points per inquiry if you have your score pulled too much by the wrong vendors. The drop could be greater if you have few accounts or a short credit history without seasoned, positive factors to compensate.

In fact, the negative effect of hard pulls usually last only one year, but most of the damage disappears within the first 90 days.

Are all credit score pulls considered equal?

Since credit scoring is primarily a means of gauging the risk of default, consumers with high credit scores will suffer a little more damage from hard credit pulls. That’s because the credit algorithms consider the fact that they’re getting their credit pulled atypical, and more of a red flag.

So the higher your score to begin, the more damage a hard credit may do.

Additionally, unsecured credit inquiries, like you’ll find with personal credit cards, retail cards, and in-store accounts, will cause the most damage to your score.

When current creditors pull your credit:

We are certain that soft credit pulls have a negligible negative effect on credit scoring – or none at all. That’s the reason why most of your current creditors will only order soft credit pulls on your account, not hard pulls.

Current creditors usually also do a soft pull every month or so, although some check up on their consumers much more frequently.

Some credit pulls always act as hard inquiries, some are always soft injuries, and some can show up as either/or.

Hard pulls are most often found with:

• Applications for new credit cards

• Requests t activate a pre-approved credit offer (such as you receive in the mail)

• Applying for a new cell phone account and contract

Soft pulls are most often found with:

• Background checks by potential employers

• Your bank verifying your identity

• Initial credit checks by credit card companies that want to issue you preapprovals

Who can pull your credit, whether through hard or soft inquiries?

Lenders

Mortgage companies

Student lenders

Banks

Credit card companies

Financing departments of retail stores

Auto dealerships financing departments

Utility companies

Cell phone companies

Employers

Landlords

Insurance companies

Collection agencies

Child support agencies

Court agencies

Anyone with “Permissible Purpose,” as deemed by the Federal Credit Reporting Act.

Timing is everything with credit pulls:

Timing is so important when it comes to credit pulls. The more “bad” inquiries that appear on your report within a short time, the bigger hit to your score. For instance, if you apply for five new credit cards within a two-week period, it definitely is seen as risky to the credit bureaus, and your score will drop accordingly.

However, the credit bureaus do account for consumers who want to “shop around” for large and important loans, like mortgages, business loans, etc. Of course, shopping for the best rate on a single loan (not applying for multiple loans at once) means getting your credit score pulled several times within a short period, but the good news is that this practice won’t hurt your credit score.

In fact, the credit bureaus typically just count this group or batch of inquiries as one if they’re within a 30-day period (or a 45-day period with some credit scoring versions).

So, if you’re shopping around for the best rate on an important loan, try to contain all credit pulls to within a 30-day period to keep your score in good order!

***

Contact Nationwide Credit Clearing if you have further questions about credit pulls, and would like a free copy of your credit report and consultation with a credit expert!

50 things you didn’t know about credit scores, credit reporting, and debt. (Part 1)

1. The first credit card ever was released in 1951 and issued by the American Express company.

1. The first credit card ever was released in 1951 and issued by the American Express company.

2. People often talk about their “credit score” as if they had just one. In fact, there are more than 100 credit scoring models used by banks, lenders, and financial institutions.

3. But FICO is the biggest and most recognizable credit scoring model. FICO is an acronym for the “Fair Isaac Corporation” and is based on the risk-predicting algorithms developed by mathematician Earl Isaac and engineer Bill Fair in 1956, and then rolled out in the 1980s as a credit scoring system.

4. Did you know that these days, credit scores are even influencing people’s dating decisions? It’s true, as surveys show that the majority of people would consider someone’s credit score before dating them or getting in a relationship. There’s even an online dating site called CreditScoreDating.com with the motto, “Credit Scores are Sexy!”

5. Millennials – and especially college kids – are really missing the boat when it comes to keeping good credit scores. In fact, Millennials have the lowest Vantage credit scores of any generation, including Gen X (ages 30-46), Baby Boomers (47-65), and the Greatest Generation (66+).

6. Speaking to that point, surveys show that 85% of U.S. college students don’t even know their own credit score!

7. These days, your credit score impacts far more than just buying a house or getting a good rate on your credit card, as many employers now check the credit reports of their potential applicants. In fact, 1 in 4 Americans looking for a job have been subjected to a credit check, and 1 in 10 has been disqualified from getting hired because of something on their credit report!

8. According to reports by the Department of Labor, occupations that routinely check a job applicant’a credit include: 1) parking booth operator, 2) the military, 3) accounting, 4) mortgage loan originator, 5) Transportation Security Administrator (TSA), 6) law enforcement and 7) temporary service positions and many more.

9. FICO scores are based on a complex (and secretive_ algorithm that factors every nuance of credit behavior from tens of millions of consumers. Their programs then look for patterns that will help them predict future defaults (or on-time payments) for borrowers, which they then translate as a numeric spectrum of risk for lenders, or your credit score.

10. These days, an estimated 33% (one out of every three) of all American adults do not pay their bills on time every month!

11. How much bad credit card debt do the big banks take a loss on every year? Last year, the top 100 banks in the U.S. had an average charge-off rate of 3.87%, which means that nearly 4 out of every 100 people don’t pay,

12. Last year, the average Annual Percentage Rate (APR) for all U.S. credit cards was 13.14% – another great reason to build up your credit score and get out of debt this year!

13. About 19 countries around the world use some form of FICO scores, and many more have their own credit scoring system.

14. Nearly two-thirds of U.S. adults – or 144 million people – haven’t even looked at their credit report within the last 365 days.

15. And one-third of working-age Americans don’t even have a clue what their credit score is!

16. Visa is by far the biggest credit card in the U.S., with 278 million cards at home (that’s about one for every adult in our population!). Mastercard is next with 180 million cards

But while Visa has 522 million cards across the globe, MasterCard just beats them out with 551 million cards abroad.

17. Visa is also the largest credit card in the U.S. by sales volume, with $981 billion in annual charges. MasterCard is second with about $534 billion in yearly debt from cardmembers.

18. The average U.S. consumer has 13 credit accounts listed on their credit report, which includes 9 credit cards and 4 installment loans. (But remember, that doesn’t mean they’re all open and active, just reporting.)

19. In the 1990s, America saw an explosion of personal debt levels that was unprecedented. One of the main causes was the fact that banks, lenders, and financial institutions starting using credit scores en masse to help them gauge risk and make faster, more accurate decisions.

20. In fact, in 1995, the nation’s two largest mortgage financing agencies, Fannie Mae and Freddie Mac, started advising lenders to use FICO scores for their borrowers, allowing the floodgates on lending to tens of millions of Americans.

21. But at first, FICO didn’t want to reveal how they calculated a consumers credit score, opting to keep it a secret. But under intense pressure from financial advocates and governmental influence, in 2003 they released a list of 22 factors that go into their credit scoring model. That same year, the U.S. Congress passed a new law that granted consumers the right to access their credit score.

22. Remember that credit scoring systems weren’t designed to help consumers and the general public, but lenders and companies. Therefore, credit scoring models, reports, and computations weren’t supposed to be easy for the average person to understand!

23. Insurance companies are using credit scores and reporting like never before. In fact, insurance actuarials prove that the lower a customer’s credit score, the more likely they are to file an insurance claim – costing their insurer money.

24. These days, 90% of homeowners and auto insurance companies use credit score as a factor when assigning and rating premiums! Therefore, insurance companies reward customers with good credit scores, and your premiums will be much lower than for those with a low credit score.

25. If you want to improve your credit score (and keep it high), then try to only keep credit cards from well-respected, major banks, like VISA, Mastercard, American Express, etc.). They’ll show that you’re a better steward of your finances and a more responsible debt holder than if you open accounts with lesser known finance companies, retail cards, etc., and your credit score will reflect that.

***

Look for part 2 of this blog, with 25 more things you didn’t know about credit scores, credit reporting, and debt!

10 Credit and financial tips for the holidays

The holidays are here, and while it’s a golden time to enjoy family, friends, give back to others and the many blessings in our lives, it’s also a time of year that can be dangerous financially. In fact, most households see a huge spike in spending and debt over between Thanksgiving, Christmas or Hanukkah, New Years – so much so that many retailers make 15-20 percent of their total annual sales during that period. Add in Valentines Day, winter family vacations and possibly a couple of birthdays, and it’s a time of year that could break the budget and crash your credit score.

The holidays are here, and while it’s a golden time to enjoy family, friends, give back to others and the many blessings in our lives, it’s also a time of year that can be dangerous financially. In fact, most households see a huge spike in spending and debt over between Thanksgiving, Christmas or Hanukkah, New Years – so much so that many retailers make 15-20 percent of their total annual sales during that period. Add in Valentines Day, winter family vacations and possibly a couple of birthdays, and it’s a time of year that could break the budget and crash your credit score.

The good news is that the holidays don’t have to time to see your debt and spending spin out of control. Here are 12 tips to help you save money, plan responsibly, keep your debt level down, and protect your credit score.

1. Set a budget

Did you know that the average American plans on spending $812 on Christmas or holiday gifts? While that is a significant amount of money, the reality is that we often shoot far past what we intended to spend, especially if you add in extra holiday meals, entertainment, decorating, parties, etc. So this holiday season, set a realistic budget and stick to it, skipping those extra money wasters that are necessary.

2. Consider spending cash

Studies show that we spend far more when we pay for purchases with a credit or debit card compared to cash. So this holiday season, visit the bank and take out the cash you’ll need for each gift on your list. You’ll end up spending less overall and also won’t have a big credit card bill come January or February – or a potential hit to your credit score.

3. Set gift limits

Have you ever given someone three presents totaling $150, only to receive a $20 gift in return? Have a conversation with your friends and family to determine if you’ll exchange gifts, how many, and set a spending limit. You may be refreshed to hear that many of your friends would rather spend time with you or go out to dinner than receive a gift, which means you’ll have more money to spoil the kids!

4. Don’t open store cards

You’re at the cash register at your favorite store at the crowded mall, doing some late Christmas shopping, when the friendly cashier asks the inevitable question, “Would you like to open a store card and get an additional 20 percent off your purchase today?”

You look at the pile of your things and do the math – saving 20 percent on the bill would add up to enough to buy you a nice lunch AND a Starbucks for the ride home.

Wait! Stop! This scenario is played out millions of times during the holiday season and throughout the year, with virtually every big retailer offering store credit cards these days. But even though it seems like a hospitable offer for a generous discount, applying for additional credit may really hurt your credit score. Store retail credit accounts often have high interest rates, low balances, hidden fees, and aren’t looked at favorably by the credit bureaus. Instead, skip the store cards and keep a responsible, low-interest card that gives you cash back or rewards points.

5. Be wary of identity theft

Identity theft and crimes of financial and data theft are more prevalent than ever in the United States, especially with the recent Equifax hack. Each year, approximately 20 million people see their identities used fraudulently, with the bill on that theft upwards of $50 billion dollars. (That’s three times more than the combined $14 billion in losses from all other types of consumer theft – burglary, motor vehicle theft, property theft, etc.) combined.

It also takes a lot of time and often money to clear up the mess identity thieves leave behind, as a compromised credit report will set off a domino effect of raising interest rates and even insurance premiums. On average, each identity theft victim suffers direct losses of $9,650, up from just $3,500 a few years ago.

So review your credit report with the help of Nationwide Credit Clearing, don’t use credit cards on fishy sites, don’t ever make purchases or give your financial details on public or unprotected Wi-Fi networks, change passwords frequently, and generally stay vigilant and protected.

6. Don’t max out credit cards

It’s really easy to max out credit cards during the holidays, but that could cause serious harm to your credit score. In fact, consumers with a score over 760 have an average credit card utilization (aggregate credit card balances relative to credit limits) of only 7 percent, and keeping under 30 percent will keep your score healthy.

7. Have a plan to pay off debt

If you don’t do you your holiday shopping with credit cards, not cash, make sure you have a sound plan how and when you’ll pay them off. It’s best to pay it off in one lump sum before interest charges even kick in, but if that’s not possible, then set a schedule of extra payments you’ll make to get your card paid off at least within the first couple months of the next year.

8. Put some money aside for emergencies

Murphy’s Law dictates that the least convenient time something can go wrong, it will. So put a few hundred dollars aside in case of emergencies or special events over the holidays. That way, if the water heater explodes Christmas morning, the car breaks down on the way to the office holiday party, or you run up your cell phone bill wishing everyone a happy New Year, you’ll be covered. The best part is that if nothing happens that warrants spending your emergency fund money, you can use it to pay off debt, add it to savings, or invest the money.

9. Start saving for next year

Now that you’ve had a great holiday, it’s time to start thinking of next year! Open a separate savings account or out aside an envelope and deposit some money every month once you get paid, not to be used for anything else. Even $25 or $50 a month will add up to big bucks that can cover most of your holiday gift-giving budget come next winter!

10. Keep your resolution to improve your credit score

Our credit scores factor into just about every lending and financial decision we make these days, including even renting a home or getting a job with some employers. Furthermore, just be improving your score from the Fair or Poor range to Great (around 720 or 760 and up), you can save a LOT of money over time. In fact, over your lifetime as a consumer, you could potentially save tens or even hundreds of thousands of dollars in interest payments on mortgages, student loans, credit cards, and auto loans, just by keeping a great score.

Therefore, it’s more important to make a firm resolution to finally improve your credit score The good news is that it’s easy to analyze your credit report and see what needs fixing with the help of Nationwide Credit Clearing – and free!

***

Contact us at MyNationwideCredit.com for to set up your free credit report review and consultation, and make it a happy holiday!

Can your credit score go down because of your social media activity?

Like it or not, social media is a big part of our lives. In fact, 81% of Americans have at least one social media profile, and we now use 2,675,700 GB of Internet data per minute! Twitter, Instagram, Snapchat, LinkedIn, and YouTube are popular social media platforms, but Facebook is still the biggest, with more than 2 billion users worldwide.

Like it or not, social media is a big part of our lives. In fact, 81% of Americans have at least one social media profile, and we now use 2,675,700 GB of Internet data per minute! Twitter, Instagram, Snapchat, LinkedIn, and YouTube are popular social media platforms, but Facebook is still the biggest, with more than 2 billion users worldwide.

People post just about every detail of their lives these days, share droves of links and content from others, and reach far past their circle of friends that they know in real life.

But it might not just be other social media users who are watching your Facebook and social media accounts and judging you. In fact, banks, lenders, and credit bureaus may soon be paying attention to your social media usage – denying you for a loan or lowering your score based on what they see.

Already, the scope that our personal data from social media is collected, shared, and sold is startling. Pretty soon, you might be denied for a loan on a credit card, a car, or even a mortgage because of who you’re friends with on Facebook. For instance, the average credit score of your social media friends and network could be a factor that influences your credit worthiness, too – a scary proposition. It’s not as far-fetched as you may think.

Back in the “good old days,” lending in the U.S. usually took place on a more personal level, with consumers walking into the local branch of their hometown bank. They sat down with a banker whom they already knew a long time and made their case for approving the loan during a conversation, with the bank granting or denying their request based on their character and reputation.

We’ve come a long way since then, and now, lending decisions are made uniformly with mountains of data collected and interpreted by nameless, faceless credit agencies with advanced algorithms – the credit bureaus.

But even with all of our advanced technology, some things never change, as credit bureaus and lenders may well be turning back the clock and trying to gauge your character, lifestyle, and reputation before approving you for a loan. Not only can they look at what you post, but check-ins, what content you like and share, and even the groups or brand pages you belong to.

The U.S. Patent office recently granted an updated patent on technology that combs social media for evidence of a person’s closest network of friends. It then relays that information to potential creditors, who can make lending decisions based on the friends’ perceived financial stability.

The patent, which Facebook first acquired from Friendster and inventor Christopher Lunt in 2010, actually has a much broader scope of intended use than just data mining for lenders. In fact, the main purpose of the patent is to protect technology that formulates and tracks how social media users are connected in a social network, protecting them from spam

But another use in the patent’s official application (called use cases in patent-speak) definitely outlines that same technology functioning as a way for lenders to aggregate credit scores and financial data from your Facebook friends when you apply for a loan.

All of this can eventually factor into their complex algorithms that gauge you as a solid candidate for a new loan – or a big credit risk.

However, there are several reasons why credit risk monitoring via social media may not be practical, ethical, or even legal.

First off, we have the Equal Credit Opportunity Act, a federal law that states that credit must be granted to all creditworthy applicants without paying credence to their race, religion, gender, marital status, age and other personal characteristics. That’s the exact reason you aren’t asked your race, religion, etc. on any loan application or credit form. But that information is often readily available on many Facebook and social media profiles, which opens the door for discriminatory practices.

Next, credit decisions are all supposed to be transparent and disputable. That means you’re supposed to know why your score goes up and down, and there can’t be mysterious or secret factors that play into your score that are disclosed on your credit report. Likewise, you have the right and ability to dispute incorrect items on your credit such as duplicate items, bad information, or even accounts opened and used by ID thieves.

But when credit bureaus track and use your social media usage to help determine your credit worthiness, they’re using factors that are neither transparent or disputable.

Furthermore, pundits point out that social media accounts can be easily manipulated. For instance, if a social media user knows that creditors are watching, they might purposely post certain things, like certain brands, check-in at certain places, etc. that would reflect positively upon them in the eyes of creditors. Basically, they could also set up fake or duplicate social media accounts, or you have the risk of someone else setting up a social media profile in another real person’s name.

Lenders will always look for “alternative data” to improve the accuracy of their credit lending decisions, some things. Cell phone usage, paying rent on time, and even bank account activity could possibly impact your credit score shortly.

But the potential for creditors to track your social media usage raises some serious concerns.

Can you achieve a perfect credit score? We’ll show you how!

When you get together with your friends, family, and coworkers, there’s always one person who loves to brag about how well they’re doing. It may be about their new car, high-paying job, or even the amazingly low interest rate they just got on their mortgage.

When you get together with your friends, family, and coworkers, there’s always one person who loves to brag about how well they’re doing. It may be about their new car, high-paying job, or even the amazingly low interest rate they just got on their mortgage.

So wouldn’t it be great if the next time they opened their mouth to be braggadocious, you could one-up them by reporting that you had a perfect credit score? There’s no topping that!

But there are plenty of financial benefits to a perfect (or excellent) credit score, too.

FICO, the most popular credit scoring model, issued by the Fair Isaac Corporation, ranges from 300 all the way up to 850. Generally, a score above 680 or so is considered “good,” and once you hit the 720 to 740 range, your score is considered “excellent.”

But there’s another level or two above that for consumers to strive for. In fact, 32.8 million people have FICO scores between 700 and 749, but approximately 70 million consumers have FICOs above 760.

Don’t stop there, because it’s possible to raise your credit score even higher. An estimated 36.4 million people have scores between 750 and 799, and 38.6 million are in the 800+ FICO range.

Only about 1% of consumers, around 2 million people, ever reach high-end 800-850 scores.

In fact, FICO estimates that only about .5% (half of one percent) of all consumers with a credit score have a perfect 850 FICO. To put in in context, the average FICO score in the United States has just reached 700 for the first time.

Remember that FICO isn’t the only credit scoring model, as there are dozens of other scoring models that banks and lenders use to make lending decisions, and then different versions of each depending on what kind of loan or even consumer they’re vetting.

So let’s say you reach an 800 credit score, or even an enviable 850 – a perfect credit score. Beyond bragging to your friends, what are the benefits?

An 850 credit score may not help as much as you think IF you compare that to another great score, like an 800, 780, or even lower. That’s because FICO uses algorithms that rate scores within “brackets,” which means that if you have above 750 or maybe 780, there really won’t be an additional benefit the higher you go.

“It’s important to understand,” reports FICO spokesman Anthony Sprauve, “that if you have a FICO score above 760, you’re going to be getting the best rates and opportunities.”

For instance, a consumer with an 850 FICO will most likely be offered the same mortgage interest rate, auto loan rate, or 0% interest credit card offer as another consumer that “only” has a 780 score.

While you may expect little perks, additional beneficial terms, and premium services with a perfect credit score, you most likely won’t see any huge benefit once you reach the “super-prime” scoring bracket.

So why strive for a perfect score? Remember that credit scores are dynamic, constantly going up and down, so today’s perfect score may be a little less next month. Furthermore, it certainly doesn’t hurt to aim for a perfect score and still have an excellent FICO even if you fall a little short. And since your credit score is a good indicator of your financial acumen and dealings with debt, a perfect credit score most likely means that your financial house is well in order.

Whether you want a perfect credit score – or just trying to improve your score until you reach 700 or even 800 – here are ten important strategies:

- Pay on time (and never miss a payment)

Even one late payment can hurt your score, and paying on time is about 35% of how FICO calculates your score. In fact, 96% of people with a FICO score of 785 or greater have no late payments on their credit reports.

- Pay down your balances

Your credit utilization ratio – how much debt you keep compared to total available balances – makes up about 30% of your credit score calculation. While you commonly hear that you should pay your credit cards and debt down below 30% of the available balances, to shoot for that perfect credit score, you’ll want to pay then down to 10% or below. In fact, a survey of consumers with 800+ scores revealed that their average credit utilization rate was just 7%.)

- Keep older and seasoned accounts

About 15% of your credit score is calculated by the length of your accounts, so older is better. According to FICO research, the average credit super scorer has an account that’s 19 years old. Likewise, the average age of their accounts is between 6 and 12 years, and they opened their most recent account 27 months ago or more.

- Keep a good mix of credit

10% of your credit score depends on managing a healthy mix of credit, including mortgages, installment loans, and high-quality revolving accounts. Consumers with FICO scores 760 and up have an average of six accounts that are currently “paid as agreed,” and an average of three accounts with a balance.

- Shop around in clusters

When you have your credit pulled to “shop around” for a loan, make sure it’s within a 30-day window and FICO won’t factor those pulls into your score. Even if they are spread out within 45 days, they’ll only be treated as one credit inquiry.

- Check your credit report often

About 25% of all credit reports contain errors, and ID theft and fraud affect about 1 in 8 American consumers. So to achieve a great score, check your score frequently and consider a credit monitoring service.

- Make payments before the due date

To earn an 800+ credit score, make payments well before you receive your bill and the due date. Try paying off (or down) your purchases at the end of every week for the best credit score.

- Increase your credit limit when offered

Another way to improve your credit utilization rate and boost your score is to take advantage of any offers to increase your credit line.

- Stick to one or two good credit cards

It’s best if you only use one or two cards on a regular basis. American Express is a great choice, as the balances don’t report to FICO since you pay them off in full every month.

- Improve your score with Nationwide Credit Clearing!

We’re the trusted leader in credit repair done right. Contact us at (773) 862-7700 or MyNationWideCredit.com for a free report and consultation so we can get you started on the way to a perfect credit score!

Answering the top-10 Google searches about credit and credit scores

Google is by far the world’s biggest search engine, with about 63% of all search traffic and 30 billion inquiries every month. In fact, type in “credit score” and you’ll get more than 69 million results! While we won’t try to answer all of those queries, here are the top 10 Google searches about credit and credit scoring:

Google is by far the world’s biggest search engine, with about 63% of all search traffic and 30 billion inquiries every month. In fact, type in “credit score” and you’ll get more than 69 million results! While we won’t try to answer all of those queries, here are the top 10 Google searches about credit and credit scoring:

- How is my credit score calculated?

There are several versions of your credit score, but the most common is issued by the Fair Isaac Corporation (FICO). While FICO keeps its credit scoring algorithms secret, we do know that the fundamental building blocks of any credit score are:

30% Credit utilization.

Your ratio of debt to available credit. It’s recommended you keep all of your debt balanced within 30% or less of your total available credit.

35% Payment history.

FICO and the other credit bureaus want to see that you’ve paid on time and in full every month, an important predictor of future payment behavior.

15% Length of credit history.

The longer your accounts have been open and in good standing, the better it reflects on your credit score.

10% Mix of credit.

A good mix of quality revolving accounts, mortgage debt, and installment debt, etc.

10% New credit.

Opening new accounts – or the wrong credit – is deemed risky and can lower your score.

- How much will a late payment hurt my credit score?

Since 35% of your credit score is based on your payment history, you always want to avoid paying any credit card or account late. Generally, if you do pay after the due date, your score will drop about 80-100 points. But you definitely don’t want to miss a payment for 60 days or even 90 days, which will cause serious damage to your credit score.

- What credit score do you need to buy a house?

If your goal is to buy a house, you’ll want to start with the mortgage process, and that means making sure your credit score is good enough to qualify for a loan, among other factors. While you’ll always have access to the best programs, terms, and the lowest interest rates with a great credit score (above 720, or even about 760 are considered “prime” scores), there are options for homebuyers with lower scores.

The Federal Housing Authority (FHA) has a great loan program that allows you to put only 3.5% down and qualify with a credit score in the 600’s, or possibly even lower in some circumstances. However, it’s always a good idea to come talk to us about six months before you plan on applying for a mortgage so we can increase your credit score and save you money.

- Will it hurt my score if my credit is pulled several times while I shop for a loan?

When you apply for new credit cards or loans with multiple creditors at the same time, it may signal to the credit bureaus that you’re recklessly taking on new credit – an indicator of future default. Therefore, your credit score may drop with these “hard” credit inquiries.

But the credit bureaus also understand they most consumers want to “shop around” for the best rates and terms when they’re making big purchases, like mortgage or auto loans, and that means having your credit pulled more than once.

To make allowances for this common consumer practice, the credit bureaus don’t ding you a batch of inquiries, as long as they’re within a 30-day period or less. Just don’t overdo it, or have your credit pulled from different kinds of debts (credit card, retail, etc.) or it will signal to them that you’re desperate to take on new debt, and your score will drop.

- Why is it important to check my credit report often?

The news these days is filled with reports of data leaks and hacks, such as the recent one of Equifax’s database that saw 235 million records compromised. Identity theft is the fastest growing crime, and most of that sensitive financial information is obtained online. For that reason, you should be checking your credit report often to screen for accounts that have been opened in your name. Likewise, the credit bureaus make a lot of mistakes when it comes to credit reporting – which could impact your score. In fact, it’s estimated that 50% of all credit reports contain errors, duplicates, or misreported information!

- How long will a bankruptcy/foreclosure/judgment stay on my credit?

Most delinquent items will report on your credit for 7 years before falling off, but there a few exceptions:

Charge-offs stay on your report for 7.5 years from the first missed payment.

Chapter 7 bankruptcies remain for 10 years from the date filed.

Chapter 13 bankruptcies remain for 7 years from the date discharged or a maximum of 10 years.

Student loans can remain on your credit until they’re paid.

Foreclosures and short sales will probably report for the full 7 years, but the negative impact will diminish over time. But changes in the industry now make it possible for some people to buy another home in as little as 1-2 years.

If you’ve experienced one of these negatives, contact Nationwide Credit Clearing.com so we can start repairing your credit and get you on the track!

- What happens if my husband/wife or cosigner on a loan and the other person defaults?

When it comes debt responsibility among married couples, different states have different laws. Community property states (include Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin) deem that you’re responsible for your partner’s debts if they were charged up during the marriage. Even if you get divorced, you’re both accountable for the debt, and it will show on both credit reports.

That’s also the case when you co-sign for a loan with someone else – the debt obligation is shared, but both parties are fully responsible. So if the other person fails to pay, or even misses a payment, your credit score will go down, and the creditor will pursue you, too.

- Why is a good credit score important?

A good credit score can save you thousands or tens of thousands of dollars on mortgage loans, credit card interest rates, car and student loans, and even insurance. Many employers are even now looking at credit reports when screening applicants!

- What is credit repair/How can credit repair help me?

Credit repair is a process where you try to clear up inaccurate, outdated, or other misreported negative items on your credit history so that your score will go up. Credit repair entails a formal procedure where we send dispute letters to the credit reporting agencies to challenge the validity of negative information. The credit bureaus are governed by the Fair Credit Reporting Act, which requires them to either fix the problem or respond with evidence that it’s true within a certain timeline. Either they will fix the inaccurate negative credit item, or, if they don’t have evidence or don’t respond in time, the item will be removed. Both outcomes help your credit score rise to where it should be.

Credit repair done through an experienced and trustworthy firm like Nationwide Credit Clearing can increase your score, remove incorrect information, and save you a lot of money in the long run.

- Do I have to pay to check my credit score?

According to the Fair and Accurate Credit Transactions Act (the FACT Act), you are eligible to receive a free copy of your credit report once each year from each of the three major credit bureaus by going to www.annualcreditreport.com. This will show your credit history, not your score, but at least you’ll be able to monitor your credit activity and make sure you’re on track.

***

For a more in-depth look at your credit score, credit report, and what you need to do to improve and save money, contact Nationwide Credit Clearing.com for a FREE credit report and consultation! We’re here to help you!

The 5 Factors That Go Into Your FICO Score

Your FICO® score is a major factor when it comes to getting approved for a loan or new credit. In fact, the Fair Isaac Corporation (FICO) is used by 90% of top lenders and banks around the country to help gauge whether you’re a good candidate for new credit, as well as the interest rate they’ll offer. In total, it’s estimated that FICO scores are used for up to 10 billion decisions about credit around the world each year!

However, FICO has closely guarded their credit scoring algorithms, so we don’t know exactly how their computations will raise or lower our scores. But the good news is that FICO does publicize the specific factors that play into a credit score.

“FICO scores give the most attention to how you have paid back lenders in the past,” says FICO spokesman Craig Watts, “and how much you are using of the credit available to you, as shown on your credit report. Those two factors contribute roughly two-thirds of a typical person’s FICO score.”

Let’s take a closer look at those five factors that go into your FICO score:

Payment History

Payment History

35 % of your total FICO credit score.

The single most important factor that influences your FICO score is your record of replaying past debts. This makes perfect sense, considering that past behavior of paying off debts on time and in full is the biggest predictor of future repayment.

When it comes to your payment history, FICO looks at both revolving loans, such as your credit cards, and installment loans, like mortgages or student loans. In fact, we do know that your FICO score will drop more if you miss a payment on a large installment loan, like your home mortgage, over a smaller credit card, for instance.

To achieve a great credit score:

The single best way to improve your FICO or keep it high is to make all of your payments on time every single month.

Credit Utilization

30 % of your total credit score.

Almost as prevalent as payment history is your credit utilization, or the percentage of available credit compared to what you already owe. Creditors are wary to lend more to consumers who consistently max out their revolving accounts and consistently spend up to their limit without a buffer. Their research shows that these folks are more likely to miss payments or default in the future f they’re already constantly spending every dollar they have available as credit.

To achieve a great credit score:

Common advice is to keep all of your credit cards and revolving debt at around 30% of the total available credit. However, FICO’s research shows that borrowers with the highest credit scores tend to have a credit utilization ratio around 7 percent or so.

Length of Credit History

15 % of your total credit score.

All accounts aren’t created equal when it comes to credit scoring, with the accounts that have been open the longest helping your score more than recently opened ones. This factors into your length of credit history, as well-seasoned accounts are a better indicator of a consumer’s responsible payment pattern. Therefore, even if they’ve never missed a payment or done anything wrong, a borrower with only new tradelines on the credit report will never have a perfect score.

To achieve a great credit score:

Make sure to keep older accounts in good standing and think twice about paying off and closing any well-seasoned accounts (including with balance transfers), as it may hurt your score.

New Credit

10 % of your total credit score.

About 1/1oth of your FICO score is determined by what kinds of new credit you’re adding – and applying for. When consumers start applying for credit cards and other credit too often within a short period of time, it indicates financial desperation or risky spending patterns, and their score may drop accordingly. The exception is when borrowers are applying for a big purchase like a mortgage or auto loan, as it’s expected that they’ll “shop around” a little.

To achieve a great credit score:

Don’t apply for new credit frivolously, and mind the quality of the new tradeline, too. Just because every retail store, department store, and credit card mailer is offering you more credit, you probably don’t want to take it.

Credit Mix

10 % of your total credit score.

To show a healthy mix of credit and financial acumen, FICO looks for a mix of different credit accounts, including credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. If a consumer has all credit cards, for instance, it may indicate a risky imbalance, and their score would be dinged accordingly. FICO’s data has shown that if a borrower has a good mix of credit, they have a higher chance of paying on time in the future.

To achieve a great credit score:

Take a look at the type of credit accounts on your report and balance it out with an installment loan, paying off an unneeded credit card, etc.

***

We now know the five factors that go into your FICO score, and what best practices to follow to keep a great credit score. However, your situation could be a little different based on what’s on your credit report and your credit history, so you should get help from a credit professional to maximize your score.

If you’d like help with your FICO score, contact us for a free consultation today!

Tips to Improve Your Credit Score this Year!

It’s the beginning of a brand new year and we wonder,, have thought about your credit score yet? A New Year means new opportunities for you financially! For those of you seeking a more financially secured life, take these tips, read them, and begin to implement them into your daily routine.

- Keep your credit card balances low. The most effective way to improve your credit score is to pay down your revolving (credit card) debt. Your credit utilization ratio accounts for 30 percent of your credit score. While you may hear that paying debt down to 30% of the available balance is a good mark, an ideal credit utilization ratio is actually around 10% or lower.

- Pay your bills on time.

- Don’t allow outdated or inaccurate information to remain on your credit report. If you see something incorrect listed on your report, you should take actions to have it removed.

- Sending your payments in early may also help your credit score. Different creditors have different report dates when they send the information to the credit bureaus.

- Check your credit report annually. It’s important to make sure that there are no errors on your credit file. A significant number of credit reports do have these errors, which can lower your score. These days, you also need to make sure that your identity hasn’t been stolen or compromised, which affects up to 1 in 8 Americans every year.

- Don’t be tempted by new credit card offers or take on new debt. You can have these solicitations stopped being sent to you by “opting out” of these offers.

- Paying off a collection will NOT increase your score. It’s not the balance, but the fact that the account went into collection status is what is essentially hurting your score. But your score will increase if the collection agency is willing to delete the account off your credit report.

- Don’t go without credit. You only have a credit score if you have an active credit history. Some credit scoring systems cannot calculate a score if no balance is reported to the credit history within the last six months.

- If you want a high score, do not pay all your debt down to zero. FICO calculates a significant portion of your score by your credit utilization ratio, so it’s important to simply keep them all under 30% of their limit

- Request an increase to your credit line. Then make sure not to use the excess credit because this will improve your overall credit % usage

- Add missing accounts to your credit report. A perfect way to build your credit is to add positive accts that are not currently being reported. Unfortunately Cell phone companies, Internet providers, utility companies, and medical billers are not required to and often don’t bother reporting credit. But if you ask them to do so, they sometimes will post a new but well-seasoned, positive new trade line to your credit report.

- If you’ve missed payments and have an account in collections, they will often agree to erase any negative credit reporting for that account as long as you pay it off in full.

- Call Nationwide Credit Clearing if you have any questions in regards to your credit or want to see how you can improve it. We’re the nation’s leader in credit repair, with our clients enjoying a lifetime of financial freedom

Nationwide credit Clearing has been the leader in credit repair for over 20 years. We can help anyone in the United States increase their credit score. Give us a call today to find out how it all works!

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

follow us on…

![]()

![]()

![]()

![]()

![]()

Secure a Solid Loan by Improving your Credit

Everyone knows that personal credit scores are crucial when it comes to obtaining a loan for a car, house, or anything that is a large purchase; however a business credit score is just as vital for small business loans. Understanding the ins and outs of building or regaining good credit may seem complicated, and here at Nationwide Credit Clearing, we want to help by providing you with these simple tips to be familiar with.

KEEP THE UTILIZATION % AT A LOW

The optimal proportion of utilization is 30% which means, if you have a $10K limit on your charge card, try to keep the exact balance below $3K. In a nutshell, you want to have a lot more credit available than you actually need. The more connected you allow yourself to reach your max amount, the higher risk you look like.

ORGANIZE MORE THAN ONE CARD

10% of one’s credit score will be based upon the mix of credit you ACTUALLY use as well as how effectively you manage them all, so be sure to have multiple cards open as well as spread utilization equally amongst them. Do NOT cancel your cards in an effort to improve your credit score. Your cards need to be kept open with a low utilization rate.

TIMING IS PRETTY MUCH EVERYTHING

Every time you submit an application, your credit score is checked. The greater number of applications you submit, the more reduced your credit score is going to b, unless you do all of your applying within a short period of time. Still, if all inquiries are set up within about 30 days or less, the reporting agencies will consider multiple inquiries as just one inquiry regarding a single purchase, so you want to keep your credit application window of this time as short as you possibly can.

MONITOR YOUR CREDIT SCORE OFTEN

Everyone is entitled to a free copy of their credit report from each one of the top 3 reporting agencies one time per year, meaning you can request a copy from a different agency every four months.

RECORD & TRACK ALL PAID OFF DEBTS

The more positive history you have of paid off debts, the better you look to prospective lenders, so make sure you keep those gold stars on your credit history as long as possible.

DON’T BE LATE

Your credit report doesn’t just cover credit cards & loan payments but it also includes every other payment you have made or are currently making. That unpaid $30 copay or electric bill will hurt you just nearly as much as a balance of $1k that hasn’t been paid on a loan or card (if it goes beyond 60 days that is).

Nationwide Credit Clearing recommends you check your report often and ensure you don’t possess unknown outlying debt..

If your credit score is not as solid as you would like it to be, start implementing these pointers and you will see your score begin to go up. Keep in mind, the right loans can in fact help develop your credit, and we can help get you there. Even though you may seem to have a hiccup and overlook a payment, do not let it discourage you. Pay the bill, and then keep moving forward; that dimple won’t be there for long.

If you still feel uncertain about how to even begin with these steps, Nationwide Credit is here to help guide you. We offer a free credit report and consultation. If it’s been a while since you have checked your credit score, please give us a call.

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

follow us on…

![]()

![]()

![]()

![]()

![]()