Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

When you make a purchase using your credit card, you are typically not thinking about the affect it will have on your future. You probably aren’t thinking of the purchase as a test of your personal integrity or reliability. You are more than likely thinking about that new television you are purchasing or how your new watch will look on your wrist. In contrast, your creditors don’t care how your new watch will look or how much joy your new television will bring you. They want to recover the money they lent you, with interest. Lenders do not like borrowers with elevated credit risk (the risk that you will not repay the money you owe). To determine your credit risk, lenders will rely on your credit score.

Your credit score is based on the information that is provided in your credit report. It will include data on past loans, foreclosures, credit utilization, bankruptcies, credit applications, and more. Credit scores follow a scale ranging from 300 (most risky) to 850 (least risky). Lenders will often times segment the score ranges into classifications such as A, B, and C.

Your credit score will affect more than just your personal finances. Credit scores influence many aspects of your personal and public life, even including situations that do not involve borrowing money. The following are situations that can be affected by a bad credit score:

Here at Nationwide Credit Clearing we will professionally assess your credit situation by procuring basic information that will allow us to obtain a copy of your current credit report. We will do this by a “soft inquiry” so that it will not affect your credit score. Our team of professionals will determine the best method of credit clearing to utilize on your case. Learn more about how we can help you!

Source: Money Crashers

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

follow us on…

![]()

![]()

![]()

![]()

![]()

Whether you are opening your first credit card or need a refresher, these credit card best practices are essential to maintaining a healthy credit score. While you may think you have your credit cards under control, there may be a few items on this list that can help you to improve.

Here’s the Rundown..

Look For A Low Interest Rate: When you are on the market for a new credit card, be sure to check the interest rate and annual fee. Read the cardholder agreement! It will give you insight into all the fees you can be charged. Don’t be afraid to ask questions before opening a new card.

Don’t Spend More Than You Can Afford: Don’t buy a TV that costs as much as your credit limit, just because you can. Purchase what you can afford to pay off at the end of that month. This will enable you to avoid interest fees.

Pay On Time: Show lenders you’re reliable, pay your credit card on time! You don’t want to pay that late fee. Also, be sure to check when your payment is due each month, it can change from time to time

Pay Off As Much As You Can: At the very least pay the minimum balance. Pay off the entire balance whenever you can, to reduce the finance charges you pay. As a rule of thumb, pay off as much as you can to avoid high interest payments. When you do have to keep a balance on your credit card try to keep it below 30% or less.

Avoid Cash Advances: When you choose to do a cash advance, a fee and interest rate is typically part of the deal. Interest rates for cash advances tend to be much higher. Only do a cash advance if it is an emergency.

Stay Within Your Limit: Keep track of what you are purchasing each month. If you stay within your limit, you’ll avoid over limit fees. Keep your credit card balance below 70% of your limit at all times. This shows lenders that you have control over how much credit you use.

Use Your Credit Card Regularly: Use your credit card regularly with the mindset that you will pay it off at the end of the month. This will show lenders that you have a proven history with being able to handle your money responsibly.

If you have tried time and time again to put these steps into play in your daily life but can’t seem to get anywhere, there is help.

Don’t wait! Better Credit is just a click away! Call the experts at Nationwide Credit Clearing. “Home of the Free Credit Report and Consultation”

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Follow us …

![]()

![]()

![]()

![]()

Your credit score is made up of a calculation of different factors obtained from your credit report.

Below are the most important points to know when considering what makes up a credit score.

1. Credit Card Utilization

This percentage is calculated by taking your total credit card balances divided by your total credit card limits. It essentially shows creditors how much of your available credit you use on average. A good rule of thumb is that lower credit card utilization rates are better.

2. Percentage of On Time Payments

This is the % of payments you’ve made on time during your credit history. It’s a factor that often weighs heavily into your creditworthiness, so just one or two late payments could negatively impact your credit score. If you have missed payments, it’s best to set up automatic bill pay or create calendar reminders for bill due dates to ensure you pay on time.

3. Total Accounts

As a general rule, the more accounts you have open, the higher the likelihood that your credit score will be good. This factor indicates that more credit cards means more lenders that have been willing to take a chance on loaning to you. Having a good mix of different types of credit is important for your overall credit health. A General rule of thumb: only open accounts that you need, not ones you want!

4. Age of Credit History

The longer your credit history and the older your accounts the better. That is why it can be a good idea to keep older credit cards open and active.

5, # of Hard Inquiries

Whenever you submit an application for credit such as a credit card, mortgage or auto loan a hard credit inquiry is started on your credit report. One hard inquiry will usually have little effect, but multiple inquiries can have a larger impact. A soft inquiry happens when you check your rate to find out what you are eligible for. When you check your rates through Nationwide Credit Clearing, this is considered a soft inquiry and won’t impact your credit score in any way shape or form.

6. Derogatory Remarks

Derogatory marks are negative and represent things such as collections, tax liens or bankruptcy. These records usually stay on your credit report for Seven to Ten years. This basically tells a lender that you may have been irresponsible in the past. Unfortunately, you have to wait out the length of time in order for it to go away.

Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

The general population doesn’t know enough about Credit in general to be able to determine what exactly is and is not factored into your overall credit score. Nationwide Credit Clearing has compiled a list of these factors for you to review on your own. This is good information for everyone to understand.

Federal laws including The Consumer Credit Protection Act and the Equal Credit Opportunity Act prohibit some things from being factored into overall credit scores.

These things include:

If you or someone you know is having trouble with their credit, and needs some guidance on how to increase a credit score, Nationwide Credit Clearing can assist you.

Stop letting bad credit affect your finances! At Nationwide Credit Clearing, We help you work on your credit report and dispute unfavorable or inaccurate/outdated information. In Turn, this it will help to improve your credit score and ultimately allow you reach your future financial goals.

Don’t wait! Better Credit is just a click away! Call the experts at Nationwide Credit Clearing. “Home of the Free Credit Report and Consultation”

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

The media, newspapers, tv and the web are full of information, but sadly, most of the information regarding credit happens to be completely innacurate.

Below you will find 3 very common credit myths.

Credit Myth #1: “If I get one credit bureau to remove an item from my credit report, the rest of the bureaus will remove it just as well..Unfortunately, this is not the case. Each of the three bureaus are independent companies. They don’t automatically work together with each other when considering deletion of items on your credit report, the truth is that all 3 of them are competitors of one another. You will have to contact & work with each bureau separately to get any negative, outdated or incorrect items removed from your credit report. All this redundant work is a significant reason so many Americans consider using credit repair companies such as Nationwide Credit Clearing to help them with this lengthy and very complex process.

Credit Myth #2: “Your yearly income or salary plays a role in your credit score.” Believe it or not, the credit scoring models don’t take salary as a consideration in any way. They do not want to discriminate based upon wages or personal income, and because of this, you could have a high paying job, but still have a very poor credit score.

Credit Myth #3: “Including a consumer statement to your credit profile can make a large difference.” Unfortunately this does not make a difference in your credit scoring at all. To be quite honest, the reality is that there’s no point in adding any type of consumer statement mainly because if you’re in a dispute with the way an item is reported, you have the ability to, by law, add a statement. However, if you are able to get the item corrected or removed because of its inaccurate reporting, having that statement would likely reaffirm the fact that it should have ended up there in some way, shape, or form. So, it’s better to just not tell your personal story, because the likelihood of anyone reading it is slim to none.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Your Credit History plays a huge role in everything you do in life. From getting a job to applying for loans, your credit score is factored in everywhere. A credit score is a screenshot taken by the 3 major credit bureaus, Experian, TransUnion, and Equifax. This gives lenders the ability to determine whether or not you will be given credit, the total amount of credit you are granted as well as the terms on your loan, (loan amount, interest rate and repayment schedule).

Below you will find information about credit scores as well as some simple steps to keep them high, all which are crucial for you in determining your financial future.

What is a credit score and how is it calculated?

Your credit score is usually a number that ranges between 300 & 850 and it’s used by creditors to determine if you are responsible and worthy of obtaining credit based on many factors. Many of the businesses that you have a credit line or a loan will send reports to these 3 bureaus of credit info such as whether or not you pay bills on time, your total credit amount, and even your credit history going back many years. A credit score is calculated simply from your individual credit history. Someone with a higher credit score, will have the ability to borrow more money. However, when your credit score is low, you may be able to obtain loans, but your interest rates will be much higher. Generally, a score of 700+ is considered GOOD while a score of 600 or below is considered very POOR.

Everyone has the ability and should take the opportunity to get a free credit report from each of the 3 bureaus once per year. All three bureaus offer this to us, but many of us don’t take advantage nor pay attention. It’s important to check your credit score to determine if it’s accurate because your score will be used to determine your financial future.

So How do I increase my credit score?

This is not a quick fix, when trying to increase your credit score, however, you can take steps to repair your score over time.

Here is our advice:

*Payment history is important so always pay your bills on time

*You never want to max out any of your credit cards. In fact, keeping your balance at 30% of your total limit is ideal.

*Don’t apply for new credit unless it’s absolutely necessary.

*Even when you pay off a card, keep it open to increase the length of your credit history

*Pay your high balance cards first, and never just transfer debts among a variety of lenders.

*If you have collections or past due accounts, settle them

*If you find inaccurate items in your credit report, make sure to dispute them.

*Usually, The last 2 years of your credit history are the most valuable

Your Credit Score will affect your life in many ways.. good or bad!

Credit scores are often used in determining prices for home or car loans as well as homeowners insurance. Employers will also check your credit score as part of background checks when making the final decision as to whether to hire you or not. Although it may not seem fair, credit scores have become more prevalent and are now used in nontraditional ways to judge you as a person.

Nevertheless, It’s more important than ever to become educated about Credit Scores.

This leads us to the final question.. When was the last time you checked your credit score?

If it’s been a while, Nationwide credit Clearing can help. We are the leaders in Credit Repair and are here to help you in making your future financial decisions or correcting mistakes you have made in the past.

So what are you waiting for? Call Nationwide credit Clearing today and get started with your free credit report and consultation.

Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

At one time in our lives, we have all made financial decisions, good or bad, that have come to affect our overall credit score. Our Credit Score ends up determining the path of our financial future.

Whether you have bad credit, bankruptcy, delinquencies, derogatory remarks or even wrong information on your credit report, watch some of these videos for your own personal knowledge or to see how Nationwide Credit Clearing can help you.

CHECK YOUR CREDIT REPORT AT LEAST ONCE/YEAR

THERE IS HELP AFTER BANKRUTPCY

HOW TO IMPROVE YOUR CREDIT AND SAVE ON INTEREST PAYMENTS

SIGNING UP FOR CREDIT CARDS AT DEPARTMENT STORES

WHAT IS A CREDIT REPORT?

Nationwide Credit Clearing is the leader in Credit Repair in the United States.

We always have to ask, When was the last time you checked your credit report? If it’s been over a year, this is where Nationwide Credit Clearing can help. Nationwide Credit Clearing has over 20 years of experience repairing credit for thousands of individuals. We have helped so many people improve their credit score by removing inaccurate, misleading or unverifiable information, ultimately changing their lives forever. We deleted over 25,000 items from credit reports in the past year.

There’s no reason to put this off and there certainly is no time like the present. Give us a shout here at Nationwide Credit. After all, We are the home of the free credit report and consultation!!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

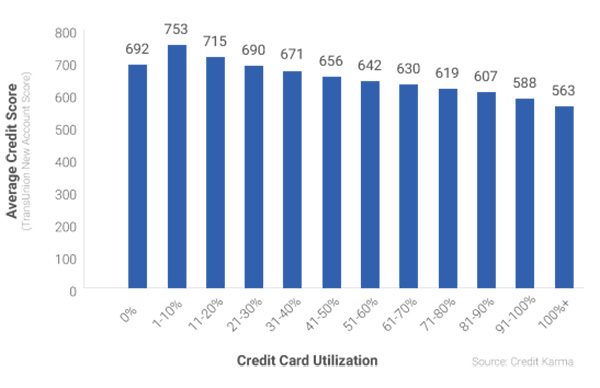

One of the most important things credit companies do to factor in your total credit score is they look at your balance to limit ratio. Your rate of utilization is simply the percentage of the total limit based upon your current balance.

To illustrate how important this factor is, Credit Karma sampled approximately 15 million Credit Karma members who visited the site in 2014 and compared their credit scores and corresponding credit card utilization rates. (Graph Provided by Creditcarma.com)

The Facts:

The correlation here is very easy to see. If you max out your card, and don’t pay it down, you are going to have problems. The lower the utilization rate, the higher your score, that is, with the exception zero utilization. As you can also see, not using your card at all is not the best option. The better choice would be to use the card for purchase during the month, then always keep that utilization at about 30%. This gives you credibility and proves to creditors that you can be responsible with money.

What this Means…

Lenders don’t like high utilization rates because it tends to indicate there’s a higher chance of you not being able to repay debt. Keeping your credit card utilization low at about 30% is the most ideal range. Creditors need to see proof, long term, that you can manage money and credit–something you can’t do without using the credit you’re granted.

If you’re uncomfortable with the idea of using your card for large purchases, you can still show an active credit profile by paying for small items with your card. It’s important that you practice good habits when managing your credit cards. Charge what you can pay back and make sure your payments are on time. In order to keep your utilization rate greater than 0%, you’ll need to let your charges show up on your billing statement, and then you can pay it off in full. This does not mean you need to carry a balance from one month to the next–doing so may just cost you money in the form of interest.

Credit utilization is just one of many factors when generating an overall score

Credit card utilization % is definitely an important aspect of your credit worthiness, and more than likely will have a significant impact on credit health, but it’s not the only factor these lenders care about. Basically, and what it comes down to, is it is not impossible for people who have high credit utilization rates to still have good credit scores, just as long as the other factors are all good– but it’s definitely not something that typically happens.

Question: When was the last time you even Checked your Credit Score?

If it’s been a while, it’s probably time to catch up. Nationwide Credit Clearing is the home of the free credit report and consultation. Not only will we provide you with an accurate view of where you stand as far as credit worthiness, but we can then help you by taking the existing derogatory items, late payments, etc.. and helping to remove them from your credit altogether.

We have helped thousands live a better life, free from credit hangups. Call today for your free report!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

![]()

How is it that you can actually get a lower credit score when you feel like your spending habits have gotten better? Learn why your credit scores might have dropped since you last checked them by using this informative infographic below:

In summary, here are 5 solid reasons your credit score may have recently dropped:

1. 30 plus days late on payments

2. Credit Card balances exceed 30% total

3. Closing an old account

4. Too many Credit Card Inquiries

5. Identity Theft may have racked up debt without you knowing.

If this seems overwhelming to you, it’s important to call a credit repair company such as Nationwide Credit Clearing

Our Family of Experts is Ready To Get You Back To Healthy Credit

LET US HELP YOU SOLVE YOUR CREDIT TROUBLE (773) 862-7700

Nationwide Credit Clearing, the home of the Free Credit report and Consultation.

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

CLICK BELOW FOR YOUR…

![]()

This video explains why it’s important not to be fooled by department store discounts given to people just for opening up a new card. Todd Stern, founder of Nationwide Credit Clearing, explains “I do not advise people opening several credit cards just to get discounts”

Tips: if you do ask them if you can charge it on your main credit card which they WILL SAY YES.

Then wait a few days and call to cancel.

How to Score:

Get your 10% and be done. You don’t want to have several open credit cards it leads to nothing but confusion and possible late payments.

The Bottom Line:

Too many open cards will decrease your credit score and increase your debt.

Already have too many?

Contact Nationwide Credit Clearing for your free credit report and consultation today.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com/index.php/contact-us/