Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

Do you think you have a pretty good grasp of the topic of credit scoring? When it comes to credit reporting and scores, what we don’t know can hurt us!

Do you think you have a pretty good grasp of the topic of credit scoring? When it comes to credit reporting and scores, what we don’t know can hurt us!

That’s because your credit score impacts so much in your life these days, from rent and homeownership to credit card approvals, interest rates on student and auto loans to even employment. But too often, we’re still in the dark when it comes to credit scores, credit reporting, and general financial knowledge about debt management.

As the nation’s leader in credit repair solutions, Nationwide Credit Clearing is committed to helping educate you about these important topics. This is part three of our ongoing series as we count up to 50 things you didn’t know about credit score, credit reporting, and debt.

Look for part one and part two here and contact us if you have any questions or credit issues at all!

1. A survey by the Consumer Federation of America (CFA) discovered that the majority of consumers (just over 50%) had no clue that their credit scores can be checked and monitored by anyone other than credit bureaus. Only 53% of respondents knew that electric utilities checked credit scores and only 68% knew that home insurers, cell phone companies, and landlords regularly do the same.

2. However, even you may be shocked to hear that 90% of home and auto insurance companies check credit scores to help determine your coverage options and also what premiums you’ll pay.

3. A 2016 survey conducted by VantageScore found that only 32% of Americans (less than one-third) had received a copy of their free credit report within the last year, and 16% hadn’t even received a free report within the last three years.

4. Not to pick on college students, but they still have a lot to learn – about their classroom subjects as well as about credit scoring. In fact, a study by Equifax found that only 45% of college kids have any idea what their credit score is! It seems the majority of college students check their credit when applying for a credit card (41%), a new debit card or bank loan (33%) compared to only 4% who request and receive a paid copy.

5. Not only is credit score a crucial factor when you want to apply for a new loan or a mortgage, but employers are screening their potential employees for credit score like never before. It’s estimated that 1 in 4 unemployed Americans have been subjected to a credit score check when they applied for a job, and 1 in 10 has been denied a job because of a bad score or something on their credit report!

6. Adding to the credit score confusion, 45% of respondents think that age is a factor in credit scoring, and 38% believe marital status plays into their credit score. (Do they believe single or married people get a score bump?)

7. On the other end of the spectrum, about 26 million people – or 14% of the adult U.S. population – has no credit score at all, called “credit invisible.” Some of them are immigrants who haven’t had the chance to establish credit lines in the U.S., while others are from low-income or unstable environments and never have taken out a credit card or loan.

8. We all know the Big Four credit card companies now (Visa, MasterCard, Discover, and Amex), but the first ever credit card that allowed a member to purchase anything they’d like and then pay it back over time was called BankAmericard. Issued in 1958, they changed their name to the more-familiar “Visa” in 1977.

In 1966, the Interbank Card Association bought the rights to “Master Charge” from the California Bank Association, which they renamed “MasterCard” in 1979.

9. Americans may be buying new cars, homes, and fancy electronics, but how are we paying for everything? Too often, the answer is with debt. In fact, 52% of Americans spend more money than they earn every single month, and 21% have regular monthly bills that are more than their take-home pay! 1 in 4 Americans have more debt than savings, and the average American spends $1.33 for every dollar they earn.

10. The American Bankers Association found that 44% of Americans surveyed thought that credit scores and credit reports were the exact same thing! That’s probably why a study by the National Foundation for Credit Counseling (NFCC) revealed that a significant portion of consumers thought that they didn’t need to know their credit score because they already had a copy of their credit report.

Online fraud is one of the fastest growing forms of crime, reaching epidemic proportions in a nexus of technology and cruel anonymity that defies international borders. The highest instance of fraud attempts is now aimed at businesses, violating their often-weak or nonexistent firewalls to access customer financial data, and using it with impunity.

You are at the register paying for a pair of new shoes at your favorite department store. The cashier asks if you would like to sign up their rewards program to save 10%. You are thinking who wouldn’t want to save 10%, of course you want to sign up. So you sign up for the stores credit card to get a discount on your purchase. Is that 10% off and a new credit card really benefiting you?

Stop and ask yourself if you really need another credit card. The more credit cards you have the greater chance you have of getting deeper into debt. It is important to remember that credit cards are not a form of supplemental income. The annual fees of the credit cards can also add up, so that 10% you saved will eventually cancel out.

Your credit score can also be negatively impacted by having too many credit cards. Which will in turn impact your ability to borrow money. Learn more about how a bad credit score can affect your life in our recent blog post (Little Known Causes for Bad Credit

In contrast, adding more cards can help your score by decreasing your credit utilization ratio (the amount of debt you carry compared to your available lines of credit). However, if you have a lot of credit cards with high limits and you go to a lender to take out a loan, the lender will take into consideration a situation where you ran those credit cards up and what your debt-to-income ratio would look like then.

So, how many credit cards is too many? There are people who are very successful using a single credit because it is easiest to manage one card. Having 3-5 cards is typically not a problem. But if you find all your credit card balances are increasing, that is a danger signal.

Source: CreditCards.com

If it’s been a long time since you have checked your credit report, give us a shout here at Nationwide Credit Clearing. Our Initial Credit Report and Consultation is Free of Charge! Call Today!

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

Most consumers are responsible – the kind who pay their bills every month and never borrow more than they can reasonably pay back. However, even the most responsible person who feels that he or she is excellent with personal finance can find him- or herself with bad credit. The reasons may be surprising, and not all of us are aware of just how much can have long-term effects on our credit reports. Here are just a few little known causes for bad credit.

Persistent Late Payments

While most consumers know how missed bill payments can negatively impact their credit reports, many don’t know that persistently paying their bills late can also have a detrimental affect. Paying a day or two late once in a while won’t be fatal, but even if you miss your payment by just one day each month, it can play a huge role in watching your credit rating plummet.

Too Many Credit Applications

Having too many credit cards or too many lines of credit can ruin your credit. Even if you pay each off each month, on time, it still makes you look like a risk to other lenders. With the higher debt you could potentially have, the worse your credit can be. You may feel responsible enough not to max out each card or each line of credit, but lenders don’t always think that way. Limiting the total credit balance available to you will go a long way in making you look more attractive to other financial institutions.

Maxing Out Your Credit Limit

Be sure not to limit yourself too much when it comes to credit cards, however. If you find that you are constantly maxing out your credit card, you will look like a credit risk, causing your credit rating to fall. Even if this limit is paid in full each month, it still indicates to other banks that you could potentially miss a payment, making you a lending risk.

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

For many of us, opening a credit card is our first chance to start building a credit history. We believe that obtaining a credit card and using it responsibly will give us a head start on a long life of positive financial habits. Millions of credit card users are fulfilling their goal of swiping their card and paying it off each month. However, there are others who are struggling to get the money together to pay of the minimum balance. We all have a tight month every once in awhile, and paying the total balance seem so optional, compared to other bills. But what really happens when you pay the minimum balance?

How The Minimum Balance Works: Interest

As you are probably aware, you can swipe your credit card as you please, as long as you do not exceed the credit card limit. As with all debt instruments, the credit issuer gives you the option to pay the bill in its entirety or to pay a small amount to deal with at a later time. Interest will be added to the remainder, which in return will increase the price of your purchases. What is interest exactly? It is what the credit card issuer chargers their cardholders to extend the loan past the finance-free grace period. The lower your interest rate or annual percentage rate (APR), the less debt you will roll over month to month.

How Does The Minimum Balance Affect Me

Aside from the obvious, of having to pay more for your purchases due to the interest rate, there are other negative consequences to paying only the minimum balance.

What Should You Do?

Keep track of what you are spending. Make sure that you do not swipe for more than you can comfortably pay off at the end of each month. Credit cards are a great tool for building good credit. However, don’t give in to the temptation to rely on them to cover the balance of a purchase you can not afford. Just because you can spend the amount of your credit limit, does not mean that you should. Remember that your credit card activity is being watched. The credit card company will send the date of your opening to consumer credit bureaus, and every month report your activity. If you charge regularly, keep the balance at $0 and make all payments by the due date.

If you have high credit card balances, deragatory remarks, or even late payments and you just can’t seem to get yourself together enough to increase your overall credit score, there is help.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

Your credit score is made up of a calculation of different factors obtained from your credit report.

Below are the most important points to know when considering what makes up a credit score.

1. Credit Card Utilization

This percentage is calculated by taking your total credit card balances divided by your total credit card limits. It essentially shows creditors how much of your available credit you use on average. A good rule of thumb is that lower credit card utilization rates are better.

2. Percentage of On Time Payments

This is the % of payments you’ve made on time during your credit history. It’s a factor that often weighs heavily into your creditworthiness, so just one or two late payments could negatively impact your credit score. If you have missed payments, it’s best to set up automatic bill pay or create calendar reminders for bill due dates to ensure you pay on time.

3. Total Accounts

As a general rule, the more accounts you have open, the higher the likelihood that your credit score will be good. This factor indicates that more credit cards means more lenders that have been willing to take a chance on loaning to you. Having a good mix of different types of credit is important for your overall credit health. A General rule of thumb: only open accounts that you need, not ones you want!

4. Age of Credit History

The longer your credit history and the older your accounts the better. That is why it can be a good idea to keep older credit cards open and active.

5, # of Hard Inquiries

Whenever you submit an application for credit such as a credit card, mortgage or auto loan a hard credit inquiry is started on your credit report. One hard inquiry will usually have little effect, but multiple inquiries can have a larger impact. A soft inquiry happens when you check your rate to find out what you are eligible for. When you check your rates through Nationwide Credit Clearing, this is considered a soft inquiry and won’t impact your credit score in any way shape or form.

6. Derogatory Remarks

Derogatory marks are negative and represent things such as collections, tax liens or bankruptcy. These records usually stay on your credit report for Seven to Ten years. This basically tells a lender that you may have been irresponsible in the past. Unfortunately, you have to wait out the length of time in order for it to go away.

Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

The general population doesn’t know enough about Credit in general to be able to determine what exactly is and is not factored into your overall credit score. Nationwide Credit Clearing has compiled a list of these factors for you to review on your own. This is good information for everyone to understand.

Federal laws including The Consumer Credit Protection Act and the Equal Credit Opportunity Act prohibit some things from being factored into overall credit scores.

These things include:

If you or someone you know is having trouble with their credit, and needs some guidance on how to increase a credit score, Nationwide Credit Clearing can assist you.

Stop letting bad credit affect your finances! At Nationwide Credit Clearing, We help you work on your credit report and dispute unfavorable or inaccurate/outdated information. In Turn, this it will help to improve your credit score and ultimately allow you reach your future financial goals.

Don’t wait! Better Credit is just a click away! Call the experts at Nationwide Credit Clearing. “Home of the Free Credit Report and Consultation”

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

At one time in our lives, we have all made financial decisions, good or bad, that have come to affect our overall credit score. Our Credit Score ends up determining the path of our financial future.

Whether you have bad credit, bankruptcy, delinquencies, derogatory remarks or even wrong information on your credit report, watch some of these videos for your own personal knowledge or to see how Nationwide Credit Clearing can help you.

CHECK YOUR CREDIT REPORT AT LEAST ONCE/YEAR

THERE IS HELP AFTER BANKRUTPCY

HOW TO IMPROVE YOUR CREDIT AND SAVE ON INTEREST PAYMENTS

SIGNING UP FOR CREDIT CARDS AT DEPARTMENT STORES

WHAT IS A CREDIT REPORT?

Nationwide Credit Clearing is the leader in Credit Repair in the United States.

We always have to ask, When was the last time you checked your credit report? If it’s been over a year, this is where Nationwide Credit Clearing can help. Nationwide Credit Clearing has over 20 years of experience repairing credit for thousands of individuals. We have helped so many people improve their credit score by removing inaccurate, misleading or unverifiable information, ultimately changing their lives forever. We deleted over 25,000 items from credit reports in the past year.

There’s no reason to put this off and there certainly is no time like the present. Give us a shout here at Nationwide Credit. After all, We are the home of the free credit report and consultation!!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

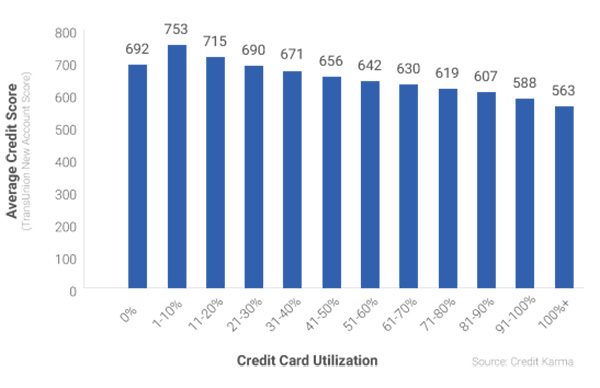

One of the most important things credit companies do to factor in your total credit score is they look at your balance to limit ratio. Your rate of utilization is simply the percentage of the total limit based upon your current balance.

To illustrate how important this factor is, Credit Karma sampled approximately 15 million Credit Karma members who visited the site in 2014 and compared their credit scores and corresponding credit card utilization rates. (Graph Provided by Creditcarma.com)

The Facts:

The correlation here is very easy to see. If you max out your card, and don’t pay it down, you are going to have problems. The lower the utilization rate, the higher your score, that is, with the exception zero utilization. As you can also see, not using your card at all is not the best option. The better choice would be to use the card for purchase during the month, then always keep that utilization at about 30%. This gives you credibility and proves to creditors that you can be responsible with money.

What this Means…

Lenders don’t like high utilization rates because it tends to indicate there’s a higher chance of you not being able to repay debt. Keeping your credit card utilization low at about 30% is the most ideal range. Creditors need to see proof, long term, that you can manage money and credit–something you can’t do without using the credit you’re granted.

If you’re uncomfortable with the idea of using your card for large purchases, you can still show an active credit profile by paying for small items with your card. It’s important that you practice good habits when managing your credit cards. Charge what you can pay back and make sure your payments are on time. In order to keep your utilization rate greater than 0%, you’ll need to let your charges show up on your billing statement, and then you can pay it off in full. This does not mean you need to carry a balance from one month to the next–doing so may just cost you money in the form of interest.

Credit utilization is just one of many factors when generating an overall score

Credit card utilization % is definitely an important aspect of your credit worthiness, and more than likely will have a significant impact on credit health, but it’s not the only factor these lenders care about. Basically, and what it comes down to, is it is not impossible for people who have high credit utilization rates to still have good credit scores, just as long as the other factors are all good– but it’s definitely not something that typically happens.

Question: When was the last time you even Checked your Credit Score?

If it’s been a while, it’s probably time to catch up. Nationwide Credit Clearing is the home of the free credit report and consultation. Not only will we provide you with an accurate view of where you stand as far as credit worthiness, but we can then help you by taking the existing derogatory items, late payments, etc.. and helping to remove them from your credit altogether.

We have helped thousands live a better life, free from credit hangups. Call today for your free report!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

![]()

We all make mistakes, especially regarding our credit and money management. Below you will find some ideas on how to rectify past financial sins you may or may not have made. It’s never too late.

Nobody’s flawless – especially when it comes to money management. There’s a pretty good chance that by now, you have control of your current finances, however, most of us have made some serious mistakes when we were younger. We have never had an owners manual on how to manage money, so chances are you have made some serious mistakes while you were younger or perhaps in college. Those previous mistakes can and will come back to haunt you today in many ways. Nationwide Credit Clearing recommends that you face your money issues head-on as well as make up for those wrong doings before being able to move on in the future..

LOOK WHAT’S GOING ON

When confronted with past financial faults, it’s easy to turn your head and hope that they disappear. But when you must pay back your money or fall behind on loans, creditors are still looking to get a way to get paid. This will definitely affect your ability, long term, to gain new credit and have financial freedom moving forward. Nationwide Credit Clearing recommends that you collect all of your records & go through them thoroughly, to allow yourself to see the bigger picture of which mistakes you have made and which ones can actually be corrected..

DEVISE A PLAN

As soon as you know where your situation stands as of now, it’s a great time to also create a plan to remove incorrect information from your credit report, as well as pay back past creditors. This is not going to be easy, but if it is important to you, we recommend that you make the time. Consider your plan as you would a project given to you at work. Focus on the plan, then look forward to the outcome.

START WITH THE BASICS

We don’t recommend that you use your savings to pay off old debt. Actually, starting with small debts – old credit cards for example – will allow you get rid of some of your smaller mistakes as well as help give you a sense of achievement. Start with the ones you can manage and control. This way, you’ll have leg room and information when it comes to time to repair your credit.

NEVER GIVE UP

Once you make progress on some of your little money issues, it will then be important to take the correct measures. The first thing you can and should do is get an accurate and up to date credit report. Nationwide Credit Clearing offers a service that provides anyone with an absolutely free, no credit card required credit report and consultation. Once we evaluate your current financial situation, we can then move forward and help you with a plan.

In conclusion, Now that you know more about how to rectify past financial sins, there’s no time like the present to get your free credit report and score.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Making late payments on your, mortgage, credit cards or loans will affect your overall credit health as well as hurt your credit score. Regardless of how late you pay, even one day late will count against you. Generally speaking, if your bills are not paid on or before the due date, this could affect you in the long haul.

Late Payments: How they Affect Your Credit

Banks as well as issuers consider the history of your payments especially after evaluating your overall credit risk & deciding if they should or should not approve you for the loan. A lengthy history of payments (on-time ) demonstrates that you are a reliable & responsible borrower.

However, a lengthy history of late payments will suggest that you are not qualified nor responsible to borrow money from a bank. The inability to be reliable is a huge red flag to banking institutions, and here are just a few things that can easily occur when you pay late.

Making late payments is a habit that could end in more damaging credit actions.

If you neglect an account until it is sent to collections or becomes delinquent, that will play a huge factor in your credit score drop. An account in collections may remain on your credit report for 7 years & cause more damage than a single late payment.

What to Do if You Have Late Payments on your Credit Report

A Simple Solution!

Credit Repair. Credit Repair is the process of identifying, disputing, and monitoring negative information on your credit report. Nationwide Credit Clearing has been helping people all over the US delete negative information from their credit past. Whether you have late payments, medical bills, or even bankruptcy, Nationwide Credit can help you get back to a state of healthy Credit.

Contact Nationwide Credit Clearing for your free credit report and consultation today.

Nationwide Credit Clearing

“HOME OF THE FREE CREDIT REPORT AND CONSULTATION”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com/index.php/contact-us/