-

-

Quick Contact

Get A free

Consultation Now!

Credit Education

How Many Credit Cards Is Too Many?

You are at the register paying for a pair of new shoes at your favorite department store. The cashier asks if you would like to sign up their rewards program to save 10%. You are thinking who wouldn’t want to save 10%, of course you want to sign up. So you sign up for the stores credit card to get a discount on your purchase. Is that 10% off and a new credit card really benefiting you?

Stop and ask yourself if you really need another credit card. The more credit cards you have the greater chance you have of getting deeper into debt. It is important to remember that credit cards are not a form of supplemental income. The annual fees of the credit cards can also add up, so that 10% you saved will eventually cancel out.

Your credit score can also be negatively impacted by having too many credit cards. Which will in turn impact your ability to borrow money. Learn more about how a bad credit score can affect your life in our recent blog post (Little Known Causes for Bad Credit

In contrast, adding more cards can help your score by decreasing your credit utilization ratio (the amount of debt you carry compared to your available lines of credit). However, if you have a lot of credit cards with high limits and you go to a lender to take out a loan, the lender will take into consideration a situation where you ran those credit cards up and what your debt-to-income ratio would look like then.

So, how many credit cards is too many? There are people who are very successful using a single credit because it is easiest to manage one card. Having 3-5 cards is typically not a problem. But if you find all your credit card balances are increasing, that is a danger signal.

Source: CreditCards.com

If it’s been a long time since you have checked your credit report, give us a shout here at Nationwide Credit Clearing. Our Initial Credit Report and Consultation is Free of Charge! Call Today!

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

Little Know Causes for Bad Credit

Most consumers are responsible – the kind who pay their bills every month and never borrow more than they can reasonably pay back. However, even the most responsible person who feels that he or she is excellent with personal finance can find him- or herself with bad credit. The reasons may be surprising, and not all of us are aware of just how much can have long-term effects on our credit reports. Here are just a few little known causes for bad credit.

Persistent Late Payments

While most consumers know how missed bill payments can negatively impact their credit reports, many don’t know that persistently paying their bills late can also have a detrimental affect. Paying a day or two late once in a while won’t be fatal, but even if you miss your payment by just one day each month, it can play a huge role in watching your credit rating plummet.

Too Many Credit Applications

Having too many credit cards or too many lines of credit can ruin your credit. Even if you pay each off each month, on time, it still makes you look like a risk to other lenders. With the higher debt you could potentially have, the worse your credit can be. You may feel responsible enough not to max out each card or each line of credit, but lenders don’t always think that way. Limiting the total credit balance available to you will go a long way in making you look more attractive to other financial institutions.

Maxing Out Your Credit Limit

Be sure not to limit yourself too much when it comes to credit cards, however. If you find that you are constantly maxing out your credit card, you will look like a credit risk, causing your credit rating to fall. Even if this limit is paid in full each month, it still indicates to other banks that you could potentially miss a payment, making you a lending risk.

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

Paying only the Minimum Credit Card Balance

For many of us, opening a credit card is our first chance to start building a credit history. We believe that obtaining a credit card and using it responsibly will give us a head start on a long life of positive financial habits. Millions of credit card users are fulfilling their goal of swiping their card and paying it off each month. However, there are others who are struggling to get the money together to pay of the minimum balance. We all have a tight month every once in awhile, and paying the total balance seem so optional, compared to other bills. But what really happens when you pay the minimum balance?

How The Minimum Balance Works: Interest

As you are probably aware, you can swipe your credit card as you please, as long as you do not exceed the credit card limit. As with all debt instruments, the credit issuer gives you the option to pay the bill in its entirety or to pay a small amount to deal with at a later time. Interest will be added to the remainder, which in return will increase the price of your purchases. What is interest exactly? It is what the credit card issuer chargers their cardholders to extend the loan past the finance-free grace period. The lower your interest rate or annual percentage rate (APR), the less debt you will roll over month to month.

How Does The Minimum Balance Affect Me

Aside from the obvious, of having to pay more for your purchases due to the interest rate, there are other negative consequences to paying only the minimum balance.

- Your Credit Score Will Fall: Making a minimum payment on your credit card is a quick solution for when you are short on cash. But the debt that you rack up over the course of a few months of minimum payments, will really mess up your credit score. 30% of your credit score is determined by how much debt you carry. Accruing charges on your credit card and failing to pay them off is like putting a dent in your credit score every month. Over time, this will add up to a lot of damage.

- Your Monthly Bills Will Pile Up: As a result of the damage you will be doing to you credit score with minimum payments, other monthly bills will expensive to. These include obligations such as insurance, rent, and loans. Lenders and insurance companies tend to charge people with poor credit more.

- Credit Card Costs Will Skyrocket: One of the most obvious impacts of minimum payments, is the unpaid balance building up. The average interest rate on a credit card is 15%, it will become very expensive to fail to pay off your balance in full. Additionally a lot of credit card companies charge a fee for exceeding your credit limit. When you are only paying off the minimum balance, this is quite easy to do.

What Should You Do?

Keep track of what you are spending. Make sure that you do not swipe for more than you can comfortably pay off at the end of each month. Credit cards are a great tool for building good credit. However, don’t give in to the temptation to rely on them to cover the balance of a purchase you can not afford. Just because you can spend the amount of your credit limit, does not mean that you should. Remember that your credit card activity is being watched. The credit card company will send the date of your opening to consumer credit bureaus, and every month report your activity. If you charge regularly, keep the balance at $0 and make all payments by the due date.

If you have high credit card balances, deragatory remarks, or even late payments and you just can’t seem to get yourself together enough to increase your overall credit score, there is help.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

6 Financial Mistakes Young People Make

Whether you just graduated from college or are moving out on your own, it can be hard to keep track of your personal finances as a young adult. Read through these 6 common financial mistakes and learn how you can avoid them.

1. Not Taking Advantage of Discounts: There is a world of special prices for students and young people out there, from banks to movie theatres – take advantage of them! Do your research beforehand, find out what discounts are available to you. Check out Groupon or Retail Me Not.

1. Not Taking Advantage of Discounts: There is a world of special prices for students and young people out there, from banks to movie theatres – take advantage of them! Do your research beforehand, find out what discounts are available to you. Check out Groupon or Retail Me Not.

2. Misunderstanding Credit Cards: Whether it be cash advances, large balances, late fees, or only playing the minimum balance, credit cards can lead to much more trouble than realized. The fine print and details of credit cards are often times misunderstood by young people. Read into what you are signing up for and ask plenty for questions when you do not understand something.

3. Signing Up For A Rental Or Mortgage That Is Too Expensive: Signing a lease for rent or applying for a mortgage that leaves you with little money to do anything else, will not only leave you at home but put you at risk for debt. You have no cash at hand, so what do you do? Sign up for credit cards to make up the difference in order to enjoy your lifestyle and pay for unexpected costs. Avoid making this mistake, sign up for a lease or mortgage that is within your budget in order to avoid creating debt for yourself.

4. No Rainy Day Fund: Setting aside money for emergencies gives you cushion for unexpected events and helps you avoid adding to your credit card balance. Maybe your car got towed, or you get injured, having a “rainy day” fund keeps you prepared for the most unexpected events. Including a “rainy day” fund as a part of your budget, will eventually help the money add up.

5. Failure To Realize How “Little Things” Add Up: Your daily coffee stops, eating lunch out, or weekly shopping trip of $100, can all add up to thousands of dollars a year. Cutting back can help you save a lot of money for savings, retirement or paying down your debt.

6. No Financial Planning Or Budget: Some young people are tainted by the idea that saving for the future is only for people thinking about retirement. Everyone can benefit from financial saving whether you are planning for retirement, purchasing a home, or traveling around the world. It is also important to budget your daily expenses. Sit down and look at what is left after your wages and fixed expenses. Not knowing how much you have can easily lead to spending more than you can afford. A budget will help you determine what you need to do to pay for your next vacation.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

Credit Q & A from Nationwide Credit Clearing

At one time in our lives, we have all made financial decisions, good or bad, that have come to affect our overall credit score. Our Credit Score ends up determining the path of our financial future.

Whether you have bad credit, bankruptcy, delinquencies, derogatory remarks or even wrong information on your credit report, watch some of these videos for your own personal knowledge or to see how Nationwide Credit Clearing can help you.

CHECK YOUR CREDIT REPORT AT LEAST ONCE/YEAR

THERE IS HELP AFTER BANKRUTPCY

HOW TO IMPROVE YOUR CREDIT AND SAVE ON INTEREST PAYMENTS

SIGNING UP FOR CREDIT CARDS AT DEPARTMENT STORES

WHAT IS A CREDIT REPORT?

Nationwide Credit Clearing is the leader in Credit Repair in the United States.

We always have to ask, When was the last time you checked your credit report? If it’s been over a year, this is where Nationwide Credit Clearing can help. Nationwide Credit Clearing has over 20 years of experience repairing credit for thousands of individuals. We have helped so many people improve their credit score by removing inaccurate, misleading or unverifiable information, ultimately changing their lives forever. We deleted over 25,000 items from credit reports in the past year.

There’s no reason to put this off and there certainly is no time like the present. Give us a shout here at Nationwide Credit. After all, We are the home of the free credit report and consultation!!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Set yourself on the path to Financial Freedom: Mistakes can be corrected

We all make mistakes, especially regarding our credit and money management. Below you will find some ideas on how to rectify past financial sins you may or may not have made. It’s never too late.

Nobody’s flawless – especially when it comes to money management. There’s a pretty good chance that by now, you have control of your current finances, however, most of us have made some serious mistakes when we were younger. We have never had an owners manual on how to manage money, so chances are you have made some serious mistakes while you were younger or perhaps in college. Those previous mistakes can and will come back to haunt you today in many ways. Nationwide Credit Clearing recommends that you face your money issues head-on as well as make up for those wrong doings before being able to move on in the future..

LOOK WHAT’S GOING ON

When confronted with past financial faults, it’s easy to turn your head and hope that they disappear. But when you must pay back your money or fall behind on loans, creditors are still looking to get a way to get paid. This will definitely affect your ability, long term, to gain new credit and have financial freedom moving forward. Nationwide Credit Clearing recommends that you collect all of your records & go through them thoroughly, to allow yourself to see the bigger picture of which mistakes you have made and which ones can actually be corrected..

DEVISE A PLAN

As soon as you know where your situation stands as of now, it’s a great time to also create a plan to remove incorrect information from your credit report, as well as pay back past creditors. This is not going to be easy, but if it is important to you, we recommend that you make the time. Consider your plan as you would a project given to you at work. Focus on the plan, then look forward to the outcome.

START WITH THE BASICS

We don’t recommend that you use your savings to pay off old debt. Actually, starting with small debts – old credit cards for example – will allow you get rid of some of your smaller mistakes as well as help give you a sense of achievement. Start with the ones you can manage and control. This way, you’ll have leg room and information when it comes to time to repair your credit.

NEVER GIVE UP

Once you make progress on some of your little money issues, it will then be important to take the correct measures. The first thing you can and should do is get an accurate and up to date credit report. Nationwide Credit Clearing offers a service that provides anyone with an absolutely free, no credit card required credit report and consultation. Once we evaluate your current financial situation, we can then move forward and help you with a plan.

In conclusion, Now that you know more about how to rectify past financial sins, there’s no time like the present to get your free credit report and score.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Department Stores Credit Cards. Good or Bad Idea?

This video explains why it’s important not to be fooled by department store discounts given to people just for opening up a new card. Todd Stern, founder of Nationwide Credit Clearing, explains “I do not advise people opening several credit cards just to get discounts”

Tips: if you do ask them if you can charge it on your main credit card which they WILL SAY YES.

Then wait a few days and call to cancel.

How to Score:

Get your 10% and be done. You don’t want to have several open credit cards it leads to nothing but confusion and possible late payments.

The Bottom Line:

Too many open cards will decrease your credit score and increase your debt.

Already have too many?

Contact Nationwide Credit Clearing for your free credit report and consultation today.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com/index.php/contact-us/

Own up to your Credit : Good or Bad

We all have made major mistakes either currently or in the past, especially when it’s regarding Money, Credit and Financial well being. Understand how you can set your self on a more effective financial route by owning up to most of your undesirable $$$ mistakes.

No one’s perfect – particularly when you are looking at managing your hard earned dollars. As you may always keep track of your funds, budget intelligently & spend well now, you may have made some significant money errors while you were young. Since having money does not come with an owner’s manual, you may have had lackadaisical spending ways or went wild with credit before you smartened up & began taking money as serious as you need to. Still, those past sins may come directly back to haunt you .. by way of creditors or really low credit scores. Your best bet would be to face money concerns head-on & compensate for those missteps before you can move on to more positive spending patterns in the future.

While confronting financial mistakes from your past, it is easy to turn a blind eye and hope they simply go away. However when you must pay back money or go into default on loans, not just are those creditors still looking to get paid, it will probably affect your long-term ability to secure funding & have what we like to call, Financial Freedom, in the near future. Rather, gather up all of your statements and read through them with a microscope to give you a general picture of which mistakes you’ve created & which can be easily rectified with a little bit of knowledge as well as hard work.

Understanding your credit is crucial.

So is a great score.

Get your credit report & Consultation NOW. Why wait? Call Today!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

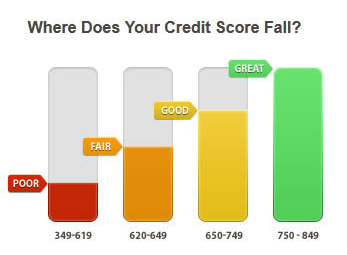

Why Is My Overall Credit Score Important?

What Is A Credit Score?

A credit score is a three-digit number, typically between 300 to 850, which credit bureaus calculate based on information in your credit report. It is a simple, numeric expression of your credit worthiness. Although the three credit reporting bureaus (Equifax, Experian, and Trans Union), use similar methods to determine a credit score, the formulas they use are not exactly the same and your credit score will vary from bureau to bureau.

How is My Overall Credit Score Calculated?

Your credit score is calculated based on a number of factors listed in your credit history that describe components of your financial life including the number and type of credit accounts you have, the amount of available credit, the length of your credit history and your payment history. Each of these factors is assigned a numerical value, and then weighted based on how prominently they affect your credit worthiness.

How Do My Actions Impact My Score?

The good news is that no matter where your credit score is today, there are a number of different steps you can take now that can change your credit history and help impact your credit score. You should take all the steps you can to help establish a good credit score.

Why Should I Check my Credit History and Overall Credit Score?

In today’s digital economy, your credit history and credit score are vital pieces of information that are key to helping you secure your financial life. Credit card companies, mortgage lenders, and insurance companies will pull copies of your credit report and score in order to decide whether to extend credit or how much to charge for your insurance premium.

Financial services companies tend to group borrowers into segments according to their credit score. These credit score ranges may determine how much you’ll be charged for your insurance coverage or the interest rate you pay on your mortgage, student or car loan or the type of credit card you’ll be offered.

If you haven’t checked your score lately, or have interest in improving your overall credit score, contact Nationwide Credit Clearing.

We offer Free (no credit card required) consultations after we pull your free credit report. Contact us Today!!

The Twelve Days of Credit

The Twelve Days of Credit: A guide to unanswered questions about your Credit Report and History….

The Twelve Days of Credit: A guide to unanswered questions about your Credit Report and History….

1. Did you know an FTC study found that about 25 Percent of Credit Reports could contain errors?

2. Some credit scoring models essentially count multiple hard inquiries, as one. As long as both loans are for the same type – ie auto or mortgage – and within a short period of time.

3. Loans you have co-signed for could appear on your credit report the same as your other accounts do. If you are thinking of co-signing, consider your own credit score as well.

4. If you are concerned about Identity Theft, a Fraud alert could make it more difficult for someone to open a new account in your name.

5. Make sure to track your Credit Utilization Rate. Try keeping your Credit Card Utilization Rate below 30%. Higher utilization rates could negatively affect your overall Credit Score

6. Lenders could close your accounts due to inactivity. To keep your current credit accounts active, try to use them regularly for at least small purchase. Of Course you should never forget to pay your bills!

7. Adverse Accounts are accounts in which information may lead potential creditors to view you as a risk. Account information includes name, address and phone number of creditor, your account number, current balance and highest balance, account limit, account status, account type and the date you opened the account. The report lists how much money is past due and how many times the account a payment has been made 30/60/90 days late. Bankruptcies, liens, foreclosures and judgments will be listed in this section.

8. Debt Validation is a consumer’s right to challenge a debt and/or receive written verification of a debt from a debt collector.

9. If you are considering using Credit Cards to earn cash back or rewards points this

Season, be sure to read the fine print. Some cards require you to enroll in rotating categories or have other limits on rewards. Always check and ask your credit card issuer for specific Details.

10. Most bankruptcies filed in the Unites States are either Chapter 7 or Chapter 13 cases.

So what is The Difference?

• Chapter 7 is a liquidation bankruptcy designed to wipe out your general unsecured debts such as credit cards and medical bills. To qualify for Chapter 7 bankruptcy, you must have little or no disposable income.

• Chapter 13 is a reorganization bankruptcy designed for debtors with regular income who can pay back at least a portion of their debts through a repayment plan. If you make too much money to qualify for Chapter 7 bankruptcy, you may have no choice but to file a Chapter 13 case.

11. Late or missed payments Can and Will reduce your overall credit score. Considering enrolling in auto-pay if you are a busy person who tends to be forgetful.

And on the TWELFTH day of Credit …someone brought up Credit Repair….

12. Credit Repair is the easiest and fastest way to increase your overall Credit Score. We work hard to dispute unfavorable or derogatory items that currently exist on your Credit Report. One should consider Credit Repair when looking to buy a new car, a new home, or anything that involves the need to present your personal credit score.

About Nationwide Credit Clearing…

Nationwide Credit Clearing has been in the credit repair business for 28 years. Nationwide Credit is the “high end boutique” of credit repair. We handle all of the work for the clients from start to finish. We give the client a free credit report consultation on day one. For us. however, It’s not just about signing up clients- we want to help them reach their goals. We Care!

Nationwide Credit is the largest credit repair company in Chicago and was told by one of the major credit bureaus six years ago that we were one of the top 3 largest companies in the country. Having such volume going through our company has opened up the doors with the credit bureaus. Two out of the three updated credit reports are sent directly to the Nationwide Credit corporate office.

Now, isn’t it time you checked your current credit score? It’s easy, just Contact us Below:

![]()