-

-

Quick Contact

Get A free

Consultation Now!

Tag Archives: mortgage broker

5 More ways to jump start your credit score (Part 2)

When a home buyer comes to a mortgage broker and applies for a loan, the difference between a 720, 680, or 620 FICO will make a huge difference in which loan programs they get approved for and the interest rate. Furthermore, consumers will be able to afford more home when buying, save a lot when refinancing, and generally have better options.

When a home buyer comes to a mortgage broker and applies for a loan, the difference between a 720, 680, or 620 FICO will make a huge difference in which loan programs they get approved for and the interest rate. Furthermore, consumers will be able to afford more home when buying, save a lot when refinancing, and generally have better options.

In part one of this blog, we covered 5 ways consumers can jump-start a borrower’s credit score.

Mortgage brokers understand that improving a borrower’s credit score is one of the most important things that will benefit their clients. But they haven’t really had to worry about credit scores in recent years, as the housing market has seen historically-low interest rates, widely accessible to most homebuyers and homeowners even if they didn’t have the highest scores.

However, times are ‘a changing, and with interest rate hikes and storm clouds on the economic horizon, it’s not unrealistic to think that we may see a market – and financial – tightening within a couple of years. While loan officers and mortgage brokers have their fingers on the pulse of these changes as they occur, there is one thing that will return to relevancy: credit score.

But you don’t want to wait six months to a year to organically improve their credit score (nor will they wait around!). Luckily, we have some tactics and strategies that can help improve a consumer’s credit score in short order. In this blog, we’ll bring you the first five strategies, and look for the next five in our upcoming blog.

And you can always contact Nationwide Credit Clearing for more information on how to improve your credit score (or your client’s score) quickly

- Pay for deletion of collections

Many of us have collections on our credit reports, which can do some serious and ongoing damage to your score. But, there may be a way to get it removed. If you’ve missed enough payments to have an account in collections, your creditors may agree to erase any negative credit reporting for that account if you pay it off.

The good news is that you can also negotiate your payoff, and if it’s in collections, they may accept less than the full amount to settle you up – sometimes even 50 percent of your balance or far less!

Once you negotiate the payoff amount AND they agree to remove the item from your credit report, only pay the collection via a mailed certified check, with “Cash only if you delete account from credit report” written above the endorsement line. Also, make sure you get their promise in writing via a letter of deletion. We can use the letter to apply for a rapid rescore instead for you, so you won’t have to wait a month or more to see your credit score rise!

- Add accounts that aren’t showing up

A surefire way to increase credit is to add positive accounts that aren’t currently being reported. Although FICO doesn’t actively publicize this information, you can do that by requesting unreported accounts be reflected on your credit. Of course, only add accounts that were in good standing, but this can add well-seasoned positive credit lines that boost your score.

Think about any company that pulls your credit and you pay the bill on time. For instance, cell phones, Internet providers, utility companies, and medical billers often don’t bother reporting credit (because it’s not mandatory) and even landlords can report rent payments. If you ask them to do so, they very well might comply – posting a well-seasoned, positive new trade line on your credit score.

- Remove federal liens

New rules have been phased in by the credit bureaus that make federal liens like tax liens, judgments, etc. less harmful to a borrower’s credit score. Due to that change, millions of Americans may see an increase to their scores without doing anything. It also may make it easier to remove harmful liens from credit scoring consideration, depending on the type and circumstances.

For instance, the IRS has a program that allows them to withdrawal the lien and deletes it from the consumer’s credit report if it’s paid. Even better, the IRS will now remove their lien from your credit report even if you still owe a balance under $25,000, as long as the taxpayer is making monthly payments as promised.

For any federal lien removal with the IRS, just call them to get the forms you need to apply for a lien withdrawal request. However, it does usually take the IRS 60 days to process lien withdrawals, at which time you’ll be issued a lien-withdrawal letter that you can get to the credit bureaus or use for a rapid rescore.

- Become an authorized user on someone else’s credit card

We talked in part one of this blog about removing authorized-user accounts that are hurting their score. However, you can also flip that. One of the most efficient ways to increase your credit score in short order is by becoming an authorized user on someone else’s credit card. Once you’re authorized, the new positive trade line will show up on your credit within 30 days as if you’ve had it for the duration.

It’s important you do this correctly – it has to be a credit line in great standing and make sure you offer your social security number, so they report it to the credit bureaus correctly. Additionally, it should be someone you trust well (and they trust you!) because if the primary user runs up big debt, has late payments, or defaults, you’ll be on the hook, and your credit will actually be damaged. But FICO knows a lot of parents do this to build their teen or college-aged children’s credit – and it’s a perfectly legal practice, so check to see if the lender has specific requirements or rules for added tradelines.

- Rapid Rescore

A Rapid Rescore is a process that lenders can use that quickly re-calculates a borrower’s credit score after they’ve don’t something to improve it, like pay off a credit card, dispute an incorrect late payment, or the like. Instead of waiting for the correction to appear on the credit score naturally – which will take much longer – a Rapid Rescore is a convenient service that will process that updated score in short order.

A Rapid Rescore fills a need or solves a problem any time you need your score to be accurately updated ASAP. For instance, timing is everything if you’re under contract for a home purchase but can’t go forward with the deal if your mortgage loan isn’t approved due to a subpar credit score. At that point, paying off debt or doing something to improve your credit and then doing a rapid rescore can save the deal.

Bonus tip:

Are you really serious about improving your credit score before buying a home or taking out a loan, and therefore saving yourself a whole lot of money? Mortgage brokers – do your clients desperately need a credit score boost in a short window in order to qualify or access the best rates?

***

If you have more questions about improving credit scores quickly, contact Nationwide Credit Clearing for a free credit report and consultation!

How mortgage lenders (or consumers!) can quickly raise a borrower’s credit score.

In recent years, the housing market has benefited from historically-low interest rates, widely accessible to most homebuyers and homeowners even if they didn’t have the highest credit scores.

In recent years, the housing market has benefited from historically-low interest rates, widely accessible to most homebuyers and homeowners even if they didn’t have the highest credit scores.

However, times are ‘a changing, and with interest rate hikes and storm clouds on the economic horizon, it’s not unrealistic to think that we may see a market – and financial – tightening within a couple of years. While loan officers and mortgage brokers have their fingers on the pulse of these changes as they occur, there is one thing that will return to relevancy: credit score.

In fact, when a borrower or home buyer comes to you and applies for a loan, the difference between a 720, 680, or 620 FICO will make a huge difference in what loan programs they get approved for, and the interest rate. Furthermore, your clients will be able to afford more home when buying, save a lot when refinancing, and generally have better options.

But you don’t want to wait six months to a year to organically improve their credit score (nor will they wait around!). Luckily, we have some tactics and strategies that can help improve a consumer’s credit score in short order. In this blog, we’ll bring you the first five strategies, and look for the next five in our upcoming blog.

And you can always contact Nationwide Credit Clearing for more information on how to improve your credit score (or your client’s score) quickly!

1. Pay down balances quickly.

We know that the ratio of your debt to total available credit – called credit utilization ratio – makes up about 30 percent of your credit score. Therefore, people with maxed out credit cards or high debt loads compared to their available credit will see their scores steadily sinking.

So, the first thing you want to do when improving your credit score is to pay down as much debt as possible.

It’s important to get your credit utilization ratio below 30 percent (so you only owe $3,000 or less on a credit card with a $10,000 available balance). Credit experts even suggest keeping a utilization ratio of 10% or less to achieve a great credit score. However, don’t go all the way to 0% because it won’t show an established payment history they can use in their calculations (since you won’t have any payment).

2. Call today and request a credit line increase.

Don’t have enough money sitting around to pay down your credit balances enough to raise your scores? Another sneaky-good way to improve your credit utilization ratio – without paying down one cent of debt – is to increase your total available credit. For instance, let’s say you had a $10,000 credit line but owed $4,000 (so your utilization ratio was 40 percent).

Instead of paying down your debt, if you could get the credit card company to increase your available limit to $15,000 from 10k, your utilization ratio just went down to about 27 percent – and your score would go up! To do this, simply call the credit card company or lender and make your case over the phone and they’ll either approve or deny your request or approve a lesser increase.

3. Remove authorized-user accounts that are hurting their score ASAP.

Many times, a borrower agrees to become an authorized user on someone else’s credit account to help that person qualify for the loan, whether it’s a credit card, an auto loan, or even a business obligation. However, if that person misses a payment or otherwise mismanages that account, the borrower’s negative hit will affect your credit score, too. Thankfully, it’s easy for us to help your borrower remove themselves from the credit account in question. It usually only takes a call to the credit card company or bank with a formal request that they’re removed from the account, as well as the item deleted from their credit report, removing the negative reporting item and improving their score.

4. Consolidate accounts – virtually overnight.

A good number of consumers find themselves with multiple credit cards or accounts from the same bank. Even if the name on the card is different. By consolidating these multiple accounts with the same parent company into one, it may help their credit score take a big jump forward. That’s the case especially if they can consolidate a newer account with an older one, which will then report as a well-seasoned account. However, we do need to carefully mind their credit utilization rate to make sure this move will positively impact their score, but it can really assist some borrowers, virtually overnight.

5. Dispute any errors or bad information on your credit report.

Most people don’t realize that credit reports often contain mistakes, misreporting, duplicate items, or outdated information. All of these things may be lowering your score, but they can also be removed. Start by contacting Nationwide Credit Clearing for a copy of your credit report, and we’ll help you review it carefully for any errors or inaccuracies.

By reviewing it line-by-line, we’ll be able to highlight inaccuracies or items that are lowering your score. Remember that there are three major credit bureaus and they each may report different information, so it might be a good idea to check all three. Look for errors on larger accounts first, length of history, payments reporting on time, and that your balances are accurate.

The last step is formally disputing each inaccuracy or error with each of the credit bureaus, Equifax, Experian, and TransUnion, separately. They are legally obligated to get back to you in a certain amount of time with proof that the information you’re disputing is correct – or they have to change it or remove it.

***

If you have more questions about improving a borrower’s credit score quickly, contact Nationwide Credit Clearing for a free credit report and consultation.

Can I get a Home Loan with Bad Credit?

The answer is: YES

To be quite honest, though, it’s not going to be easy to get a loan if:

- Your Credit Score is Low

- You Have Late Payments

- Derogatory Items on your Credit Report

- Excess Debt

- Anything else Related

Don’t get discouraged because there is a solution. Depending on your personal situation, it may take some work on your part to make your dreams happen, but for piece of mind, even if your credit is bad, the possibility of getting approved for a mortgage is there. You just have to take the correct steps and actions that will allow you to get approved. Below is some interesting information:

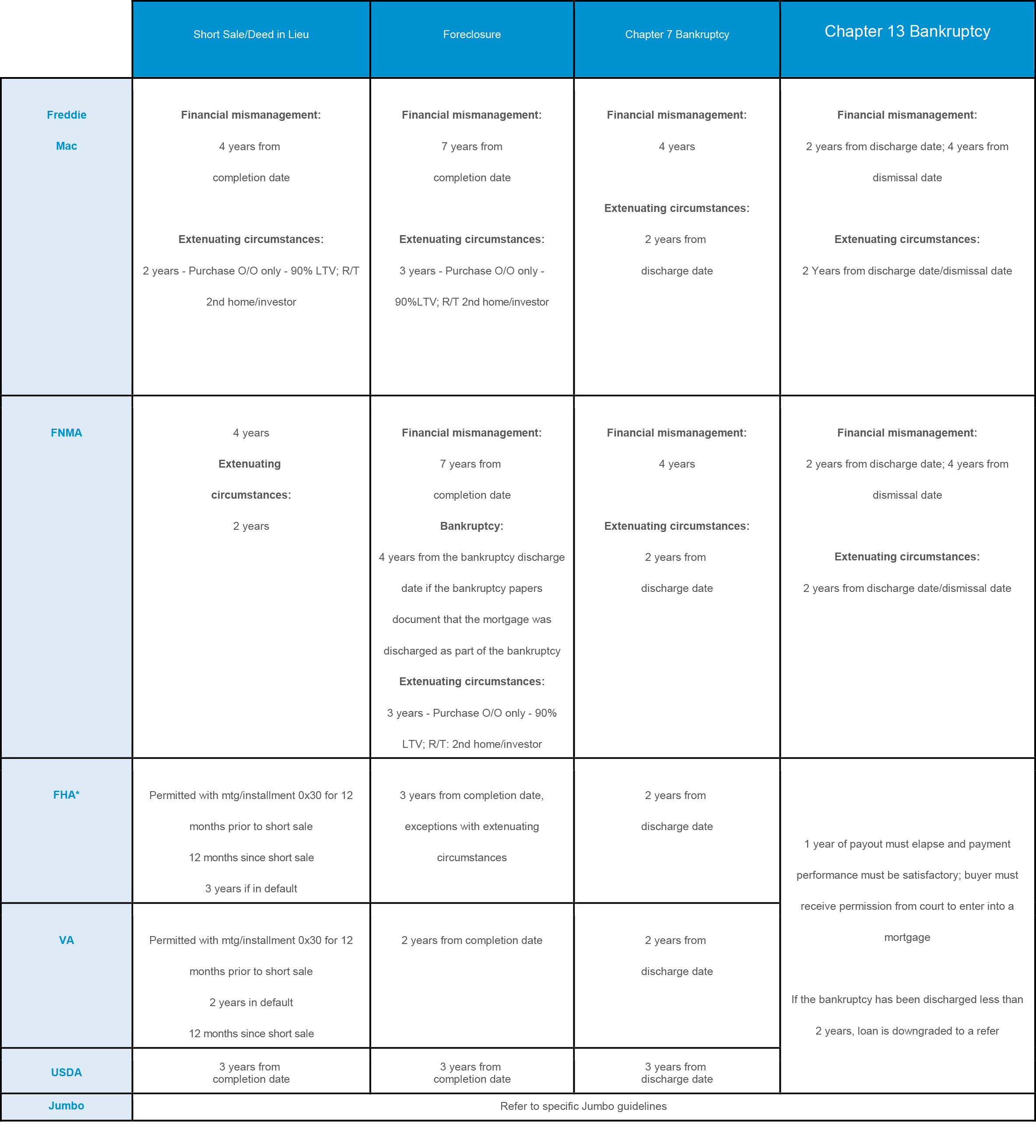

GUIDELINES FOR PEOPLE WHO HAVE CREDIT ISSUES BUT ARE TRYING TO GET A MORTGAGE:

If you have recently or in the past been denied for a mortgage, Nationwide Credit Clearing can help. We have been helping people remove negative items from credit reports for over 20 years. If a mortgage broker has a client that cannot get approved, often times they will send their client to Nationwide Credit Clearing, we will take the appropriate actions to help increase their client’s score, and send them right back through the approval process knowing that this time the end result will be different.

Just as well, if you are looking into getting a home loan, but are not in the process because you are afraid you may get denied, you will want to contact Nationwide Credit Clearing initially. We offer absolutely free no obligation credit report and consultations for all new or potential clients.

If you or someone you know is having a hard time getting approved for a home loan, contact us today.

After all, we are ” The home of the free Credit Report and Consultation”

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

CLICK BELOW FOR YOUR…

![]()