-

-

Quick Contact

Get A free

Consultation Now!

Tag Archives: homeownership

Another 10 facts about credit scores, credit reporting, and debt.

Do you think you have a pretty good grasp of the topic of credit scoring? When it comes to credit reporting and scores, what we don’t know can hurt us!

Do you think you have a pretty good grasp of the topic of credit scoring? When it comes to credit reporting and scores, what we don’t know can hurt us!

That’s because your credit score impacts so much in your life these days, from rent and homeownership to credit card approvals, interest rates on student and auto loans to even employment. But too often, we’re still in the dark when it comes to credit scores, credit reporting, and general financial knowledge about debt management.

As the nation’s leader in credit repair solutions, Nationwide Credit Clearing is committed to helping educate you about these important topics. This is part three of our ongoing series as we count up to 50 things you didn’t know about credit score, credit reporting, and debt.

Look for part one and part two here and contact us if you have any questions or credit issues at all!

1. A survey by the Consumer Federation of America (CFA) discovered that the majority of consumers (just over 50%) had no clue that their credit scores can be checked and monitored by anyone other than credit bureaus. Only 53% of respondents knew that electric utilities checked credit scores and only 68% knew that home insurers, cell phone companies, and landlords regularly do the same.

2. However, even you may be shocked to hear that 90% of home and auto insurance companies check credit scores to help determine your coverage options and also what premiums you’ll pay.

3. A 2016 survey conducted by VantageScore found that only 32% of Americans (less than one-third) had received a copy of their free credit report within the last year, and 16% hadn’t even received a free report within the last three years.

4. Not to pick on college students, but they still have a lot to learn – about their classroom subjects as well as about credit scoring. In fact, a study by Equifax found that only 45% of college kids have any idea what their credit score is! It seems the majority of college students check their credit when applying for a credit card (41%), a new debit card or bank loan (33%) compared to only 4% who request and receive a paid copy.

5. Not only is credit score a crucial factor when you want to apply for a new loan or a mortgage, but employers are screening their potential employees for credit score like never before. It’s estimated that 1 in 4 unemployed Americans have been subjected to a credit score check when they applied for a job, and 1 in 10 has been denied a job because of a bad score or something on their credit report!

6. Adding to the credit score confusion, 45% of respondents think that age is a factor in credit scoring, and 38% believe marital status plays into their credit score. (Do they believe single or married people get a score bump?)

7. On the other end of the spectrum, about 26 million people – or 14% of the adult U.S. population – has no credit score at all, called “credit invisible.” Some of them are immigrants who haven’t had the chance to establish credit lines in the U.S., while others are from low-income or unstable environments and never have taken out a credit card or loan.

8. We all know the Big Four credit card companies now (Visa, MasterCard, Discover, and Amex), but the first ever credit card that allowed a member to purchase anything they’d like and then pay it back over time was called BankAmericard. Issued in 1958, they changed their name to the more-familiar “Visa” in 1977.

In 1966, the Interbank Card Association bought the rights to “Master Charge” from the California Bank Association, which they renamed “MasterCard” in 1979.

9. Americans may be buying new cars, homes, and fancy electronics, but how are we paying for everything? Too often, the answer is with debt. In fact, 52% of Americans spend more money than they earn every single month, and 21% have regular monthly bills that are more than their take-home pay! 1 in 4 Americans have more debt than savings, and the average American spends $1.33 for every dollar they earn.

10. The American Bankers Association found that 44% of Americans surveyed thought that credit scores and credit reports were the exact same thing! That’s probably why a study by the National Foundation for Credit Counseling (NFCC) revealed that a significant portion of consumers thought that they didn’t need to know their credit score because they already had a copy of their credit report.

Online fraud is one of the fastest growing forms of crime, reaching epidemic proportions in a nexus of technology and cruel anonymity that defies international borders. The highest instance of fraud attempts is now aimed at businesses, violating their often-weak or nonexistent firewalls to access customer financial data, and using it with impunity.

The homebuying and mortgage process starts with your credit score.

Homeownership rates are near modern-era lows, but it’s not because people don’t want to buy. But surveys reveal that coming up with a down payment, qualifying for the mortgage, too much debt, and even credit score are holding them back from homeownership.

Homeownership rates are near modern-era lows, but it’s not because people don’t want to buy. But surveys reveal that coming up with a down payment, qualifying for the mortgage, too much debt, and even credit score are holding them back from homeownership.

In fact, the majority of people who are planning to buy a house in the next 12 to 18 months are pretty confused about what credit score they need, and how to improve their score. However, this national survey found that only 45 percent of potential home buyers really understand what their credit score is measuring – their responsible management of debt and risk of defaulting on new loans.

Likewise, less than 50 percent of respondents could identify what their credit score affects in the mortgage process (such as interest rates, program guidelines, and the amount they qualify for.)

Their lack of clarity can actually hurt their score, further delaying or even canceling their plans to buy a home. For instance, 33 percent of consumers polled think that increasing income will help their credit score, and 28 percent believe that closing old accounts will do the same (not the case).

Even more concerning is that they’re unsure of where to even start with the knowledge, actions, and assistance to ready their credit for a home purchase. Only 22% of people polled thought that they should check their credit report in the three months leading up to their mortgage application!

Of course, when people start the process of buying a home, there are a lot of things to focus on: which neighborhood they want to live in, finding the perfect house, getting approved for a mortgage at a great interest rate, and then the all-consuming process of packing and moving. But before any of that happens, there is one more item that should lead off their checklist: taking care of their credit score.

So, keeping your credit score up to par has some very tangible benefits during the home buying process:

• Lower interest rates,

• A greater variety of loan programs available,

• Qualify for loans with less money down,

• Your offer on a house will be seen as more favorable if you have a high credit score, giving you more leverage. During multiple offer situations and bidding wars, the seller sometimes requests additional documentation like proof of the buyer’s credit score and funds.

• But, of course, saving money when you make your mortgage payment every month is the real benefit. Even a credit score increase of a few points may help you qualify for a lower interest rate, adding up to tens of thousands of dollars in savings over the life of your loan.

Consider these three scenarios, where three consumers who are buying a $400,000 home, with a $320,000 mortgage, qualify for interest rates of 4%, 4.5%, and 5%, respectively. Please note this is just an illustration for educational purposes.

Interest Rate: 4%

Monthly Payment: $1,527

Total of 360 Payments: $549,982.42

Total Interest Paid: $229,982.42

Interest Rate: 4.5%

Monthly Payment: $1,621

Total of 360 Payments: $583,701.48

Total Interest Paid: $263,701.48

Interest Rate: 5%

Monthly Payment: $1,717

Total of 360 Payments: $618,418.51

Total Interest Paid: $298,418.51

That means if your credit score was top notch and you qualified for a 4% interest rate (hypothetically), you’d save $190 a month compared to the 5%, and $94 compared to the 4.5% loan. That sounds nice, but doesn’t seem like big money, right?

But when you compare the long-term savings, the person with the 4% loan saves $68,418 in total payments over the life of the loan compared to the 5% loan, and $33,719 compared to the 4.5%

That’s some HUGE savings for just a very small interest rate difference. (For even more information how a good credit score will save you money, read this.

So, how do you make sure your credit score is ready for the home buying process? Here are some tips to make sure your credit score will be as high as possible when you’re ready to buy a home:

1. Always pay on time.

According to FICO, 96% of people with a FICO score of 785 or greater have no late payments on their credit reports, so be one of those people who have a spotless payment history if you want the perfect FICO. Since payment history is 35% of FICO’s scoring model, paying on time is crucial.

2. Check your credit report periodically.

It’s important to make sure that there are no errors on your credit file and everything is in order. These days, you also need to make sure that your identity hasn’t been stolen or compromised, which affects up to 1 in 8 Americans every year.

3. Spend less and pay down your balances.

FICO calculates a significant portion of your score by your credit utilization ratio – how much debt you keep to how much your total available balances are. A survey of those who had the top scores revealed their average credit card balances relative to their limits was just 7%.

FICO calculates 30% of their scoring model by the overall money you owe and how close you are to the limits on your credit cards and revolving debt, so low balances, and healthy ratios are the key to a top score.

4. Keep a good mix of credit.

Consumers with FICO scores above 760 have, on average, six accounts that are currently “paid as agreed” and an average of 3 accounts with a balance.

5. Keep well-seasoned accounts.

Most super scorers also have, on average, an account that’s 19 years old. The average age of their accounts is between 6 and 12 years old and they opened their most recent account 27 months ago or more. 15% of FICO’s scoring is calculated by the credit history.

6. Start early.

Don’t wait until you’re ready to start looking at houses or apply for a mortgage to start working on your credit. Get a copy of your credit report from Nationwide Credit Clearing six months before you’re ready to apply for a mortgage. That will give you plenty of time to pay down debt, close unwanted accounts, or dispute errors and inaccuracies in order to maximize your score – as well as working with Nationwide Credit Clearing to repair your score.

7. Do’s and Dont’s during the home buying process.

It’s important not to make big changes during the mortgage process, as it may trigger a red flag for lenders, who are trying to make decisions based on a static snapshot of your finances. Avoid big purchases on credit, moving large sums of money to and from bank accounts, and applying for any new credit or closing existing accounts.

8. Consider getting help.

Before you even sit down with a mortgage broker or take a ride around town with a Realtor, home buyers would be wise to contact Nationwide Credit Clearing. With a complimentary free credit report and consultation, we can analyze your situation and give you an accurate assessment if your credit is home-buying worthy or needs some work.

Contact us today to get started – and happy home hunting!

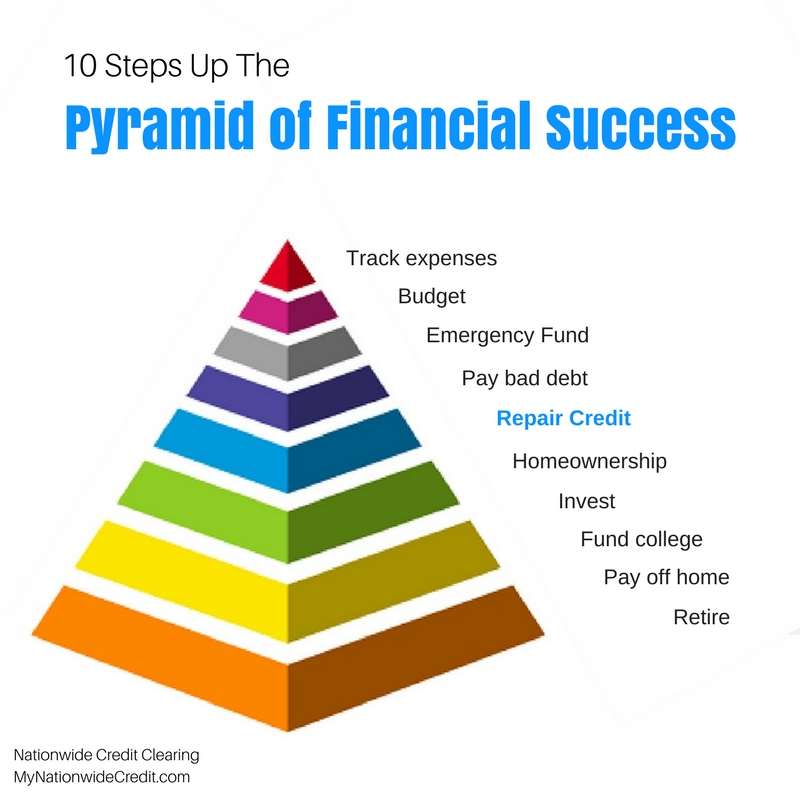

The Pyramid of Financial Success

The Pyramid of Financial Success

The Pyramid of Financial Success

No matter what our financial situations look like, everyone pretty much wants the same thing: low bills, plenty of savings, living in our own home, and enough investments to retire whenever we wish. Achieving that lofty goal is also very obtainable if you follow these 10 steps to climb the Pyramid of Financial Success:

1. Track expenses

Before you do anything else, it’s critical to know exactly how much you’re spending every month, and on what. Sure, you may THINK you know what your bills are and how much you spend, but I bet that you’ll be pretty shocked when you write down every single penny you spend (or use one of the great financial apps that help you record expenses). Try this for a month and then add up the total expenses and you’ll be amazed how much you’re blowing on impulse purchases, things you don’t really need or even want, and items that you didn’t realize are costing you!

2. Set a budget

Now that you know exactly what you’re spending your hard-earned dollars on, it’s time to tighten the belt. Ruthlessly slash everything from your budget that’s not a necessity – and hold yourself accountable to it. This will take some discipline but turn it into a fun game, and keep reminding yourself that by sacrificing NOW, you’ll be able to put yourself in a much better financial situation that lets you spend more on the things you really love and want later on.

3. Build an emergency fund

Did you know that 40 percent of Americans couldn’t come up with $400 in cash if faced with an emergency today, and two-thirds don’t have even $1,000 saved? As we’ve turned to debt more and more, the savings deficit in the U.S. has grown. However, it’s so important that you accumulate a rainy-day fund, which is a fair bit of cash that you can use when the car breaks down, you miss work because of a medical problem, or some other challenge. Start by putting $400 away, then $1,000, and keep saving until soon, you’ll have at least a few month’s total expenses saved as a cushion.

4. Pay debt

This is a big one! Once you’ve set a budget and put aside a few bucks as a safety net, it’s time to tackle the hardest part of all: paying off debt. In fact, the average American household now has $16,883 in credit card debt, $50,626 in student loans, $29,539 in auto loans, and, if they’re lucky, a mortgage on top of all that. But the one that we want to start with is paying off credit cards, as well as other revolving debt and retail installment loans. This is essential if you want to free yourself from a life of struggling and stressing about money and bills, and open up a much more secure and comfortable relationship with money.

There are several ways you can pay off your debt, but one of the best is using the technique of Debt Snowballing which is advocated by financial gurus Dave Ramsey, Suzie Orman and others. We’ll bring you more info on Debt Snowballing soon.

5. Repair credit

In fact, it’s a good idea to tackle #4 and #5 on this list in conjunction so that you’ll end up debt free AND with a fantastic credit score, starting with a free credit report and consultation from Nationwide Credit Clearing. We’ll go over your credit report and debt load with you, identifying which of them should be paid off first since they have the highest interest rates (or smallest balances).

Likewise, we can advise you which of your credit accounts should just be paid down (not off) and kept open. Our service will also attempt to remove negative, incorrect, and outdated items from your credit report, boosting your score to new heights.

How important is a great credit score? These days, just about everything you pay is tied to credit score, from all of your credit cards, your mortgage, and other loans, as well as utilities, cell phone accounts, the ability to rent a home, and even your job!

6. Buy a house

Speaking of (not) renting, once you have some savings and your debt paid off, the next big step in your financial pyramid is buying your own home. In fact, homeownership is still the American Dream, allowing you to build equity, pay down your loan, enjoy lucrative tax breaks, and experience the pride of ownership. These days, down payment programs make it easier than ever to come up with the money needed to buy a house, and you’ll essentially be paying yourself every month instead of your landlord!

7. Invest

Your bad debt is gone, and you’re now in your own home, so it’s time to start investing. Actually, you should be investing from day one in a 401K, mutual fund, or other safe, stable vehicle, as the power of compounding really comes into play the earlier you start. Contact a financial planner or advisor for the best way to invest and save for retirement considering your situation and goals.

8. Fund college

Remember how we mentioned that the average household has $50,000+ in student loan debt? Why not give your children a head start (not extra hurdles) in life by funding as much of their college education as possible instead of piling on more debt?

9. Pay off your home

We paid off your bad debt when we zeroed-out those credit cards, and you’ll get to a point high up the pyramid of financial success where the next logical step will be to pay off your home, too. There are several great strategies to help you do this, such as sending in a 13th payment every year, paying every two weeks instead of monthly, or adding extra funds to pay off principal faster. Either way, once you pay off your home in 20 or even 10 years instead of 30 (like most mortgages), your biggest bill will be knocked off the list.

10. Retire

With little or no debt, plenty of savings, a well-spring of investment income, and your home paid off, you’ll be in the enviable position at the top of the pyramid, where you can choose to retire whenever you like. Of course, that doesn’t mean that you must stop working, as many people opt to pursue their passion or work a lighter schedule just because it’s enjoyable. Either way, you’ll be the master of your financial life – not the other way around! Congratulations on making it to the top of the pyramid!