-

-

Quick Contact

Get A free

Consultation Now!

Tag Archives: credit score

Little Know Causes for Bad Credit

Most consumers are responsible – the kind who pay their bills every month and never borrow more than they can reasonably pay back. However, even the most responsible person who feels that he or she is excellent with personal finance can find him- or herself with bad credit. The reasons may be surprising, and not all of us are aware of just how much can have long-term effects on our credit reports. Here are just a few little known causes for bad credit.

Persistent Late Payments

While most consumers know how missed bill payments can negatively impact their credit reports, many don’t know that persistently paying their bills late can also have a detrimental affect. Paying a day or two late once in a while won’t be fatal, but even if you miss your payment by just one day each month, it can play a huge role in watching your credit rating plummet.

Too Many Credit Applications

Having too many credit cards or too many lines of credit can ruin your credit. Even if you pay each off each month, on time, it still makes you look like a risk to other lenders. With the higher debt you could potentially have, the worse your credit can be. You may feel responsible enough not to max out each card or each line of credit, but lenders don’t always think that way. Limiting the total credit balance available to you will go a long way in making you look more attractive to other financial institutions.

Maxing Out Your Credit Limit

Be sure not to limit yourself too much when it comes to credit cards, however. If you find that you are constantly maxing out your credit card, you will look like a credit risk, causing your credit rating to fall. Even if this limit is paid in full each month, it still indicates to other banks that you could potentially miss a payment, making you a lending risk.

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

Paying only the Minimum Credit Card Balance

For many of us, opening a credit card is our first chance to start building a credit history. We believe that obtaining a credit card and using it responsibly will give us a head start on a long life of positive financial habits. Millions of credit card users are fulfilling their goal of swiping their card and paying it off each month. However, there are others who are struggling to get the money together to pay of the minimum balance. We all have a tight month every once in awhile, and paying the total balance seem so optional, compared to other bills. But what really happens when you pay the minimum balance?

How The Minimum Balance Works: Interest

As you are probably aware, you can swipe your credit card as you please, as long as you do not exceed the credit card limit. As with all debt instruments, the credit issuer gives you the option to pay the bill in its entirety or to pay a small amount to deal with at a later time. Interest will be added to the remainder, which in return will increase the price of your purchases. What is interest exactly? It is what the credit card issuer chargers their cardholders to extend the loan past the finance-free grace period. The lower your interest rate or annual percentage rate (APR), the less debt you will roll over month to month.

How Does The Minimum Balance Affect Me

Aside from the obvious, of having to pay more for your purchases due to the interest rate, there are other negative consequences to paying only the minimum balance.

- Your Credit Score Will Fall: Making a minimum payment on your credit card is a quick solution for when you are short on cash. But the debt that you rack up over the course of a few months of minimum payments, will really mess up your credit score. 30% of your credit score is determined by how much debt you carry. Accruing charges on your credit card and failing to pay them off is like putting a dent in your credit score every month. Over time, this will add up to a lot of damage.

- Your Monthly Bills Will Pile Up: As a result of the damage you will be doing to you credit score with minimum payments, other monthly bills will expensive to. These include obligations such as insurance, rent, and loans. Lenders and insurance companies tend to charge people with poor credit more.

- Credit Card Costs Will Skyrocket: One of the most obvious impacts of minimum payments, is the unpaid balance building up. The average interest rate on a credit card is 15%, it will become very expensive to fail to pay off your balance in full. Additionally a lot of credit card companies charge a fee for exceeding your credit limit. When you are only paying off the minimum balance, this is quite easy to do.

What Should You Do?

Keep track of what you are spending. Make sure that you do not swipe for more than you can comfortably pay off at the end of each month. Credit cards are a great tool for building good credit. However, don’t give in to the temptation to rely on them to cover the balance of a purchase you can not afford. Just because you can spend the amount of your credit limit, does not mean that you should. Remember that your credit card activity is being watched. The credit card company will send the date of your opening to consumer credit bureaus, and every month report your activity. If you charge regularly, keep the balance at $0 and make all payments by the due date.

If you have high credit card balances, deragatory remarks, or even late payments and you just can’t seem to get yourself together enough to increase your overall credit score, there is help.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

Why Is My Overall Credit Score Important?

What Is A Credit Score?

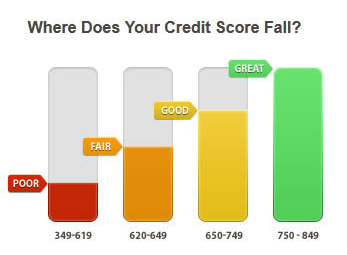

A credit score is a three-digit number, typically between 300 to 850, which credit bureaus calculate based on information in your credit report. It is a simple, numeric expression of your credit worthiness. Although the three credit reporting bureaus (Equifax, Experian, and Trans Union), use similar methods to determine a credit score, the formulas they use are not exactly the same and your credit score will vary from bureau to bureau.

How is My Overall Credit Score Calculated?

Your credit score is calculated based on a number of factors listed in your credit history that describe components of your financial life including the number and type of credit accounts you have, the amount of available credit, the length of your credit history and your payment history. Each of these factors is assigned a numerical value, and then weighted based on how prominently they affect your credit worthiness.

How Do My Actions Impact My Score?

The good news is that no matter where your credit score is today, there are a number of different steps you can take now that can change your credit history and help impact your credit score. You should take all the steps you can to help establish a good credit score.

Why Should I Check my Credit History and Overall Credit Score?

In today’s digital economy, your credit history and credit score are vital pieces of information that are key to helping you secure your financial life. Credit card companies, mortgage lenders, and insurance companies will pull copies of your credit report and score in order to decide whether to extend credit or how much to charge for your insurance premium.

Financial services companies tend to group borrowers into segments according to their credit score. These credit score ranges may determine how much you’ll be charged for your insurance coverage or the interest rate you pay on your mortgage, student or car loan or the type of credit card you’ll be offered.

If you haven’t checked your score lately, or have interest in improving your overall credit score, contact Nationwide Credit Clearing.

We offer Free (no credit card required) consultations after we pull your free credit report. Contact us Today!!

What is Considered a Good Credit Score?

Do you know what is a good credit score?

Still have questions?

Call the experts at Nationwide Credit Clearing

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone

773-862-7700

877-334-3296

Fax:

773-862-7703

E-Mail:

support@mynationwidecredit.com