Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

What are derogatory items?

Derogatory items are significantly damaging marks that show up on credit reports as a result of poorly managed credit scores or identity theft. Measures such as late/skipped payments can ultimately lead to the existence of derogatory marks on your reports. Each mark corresponding to a particular circumstance or outcome. Below are a few examples of several key derogatory items you should know about:

Charge-off: A charge-off is one of the worst marks a person can get on his or her credit report, as they happen when a lender determines that someone isn’t able (or unwilling) to pay off a debt they’ve been delinquent on for many months of payments. Although the lender determines the borrower is unable to pay, the lender is still able to legally demand payment entirely for as long as the state’s statute of limitations allow. It needs to be noted that it’s possible for charged-off financial debt to be settled for under its full worth, but credit reports will often note that the debt was not paid in full should this happen.

Collections: Sometimes debt goes to a collections bureau after a lender or service fails to receive payments. With this designation on your own credit report is quite severe; it is possible to work with a collections agency to make paying the money a bit easier. You can also negotiate conditions on your mark to disappear from your information completely once you make the agreed-upon payments.

Court Judgement: Judgements make reference to civil court rulings typically made against one person who owes money to someone else (similar to a lawsuit from a creditor or any other lawsuit regarding money). Since judgements are a case of public record, they could easily show up on credit reports.

Default: A default, particularly on certain kinds of loans (home, student, car), can create a serious problem on credit reports. Oftentimes, a default can be a precursor to several of the other items on this checklist, as it is one of the very first derogatory items that will show up on a past due individual’s credit report. For example, a default might appear onto your credit reports prior to the account being sent to collections. This is why it is extremely crucial to take non-payments seriously and address the problem that caused them right away.

Repossession: Repossession typically occurs when you default on a secured loan, i.e.. You presented something in collateral. If this occurs, everything you offered as collateral for this loan will be taken by way of the lender. This most frequently happens for mortgages and car loans, where the car or home you purchased with this loan is taken away. It’s worth noting that if the current amount of the repossessed item does not cover the entire remaining account balance on this loan, you might still be on the hook for future payments. These things are in no way an exhaustive list of derogatory marks; however they are several of the worst and most damaging, which is why you need to be aware of them.

How can I tell if my credit reports have derogatory marks?

The easiest way to find out if your credit reports include any derogatory marks would be to check your credit report & score. If you do not already know, federal law enables you to get one free copy of all the three of your credit reports – Equifax, Experian, and TransUnion – one time per year through most online services.

Can someone really improve their credit after receiving multiple derogatory marks?

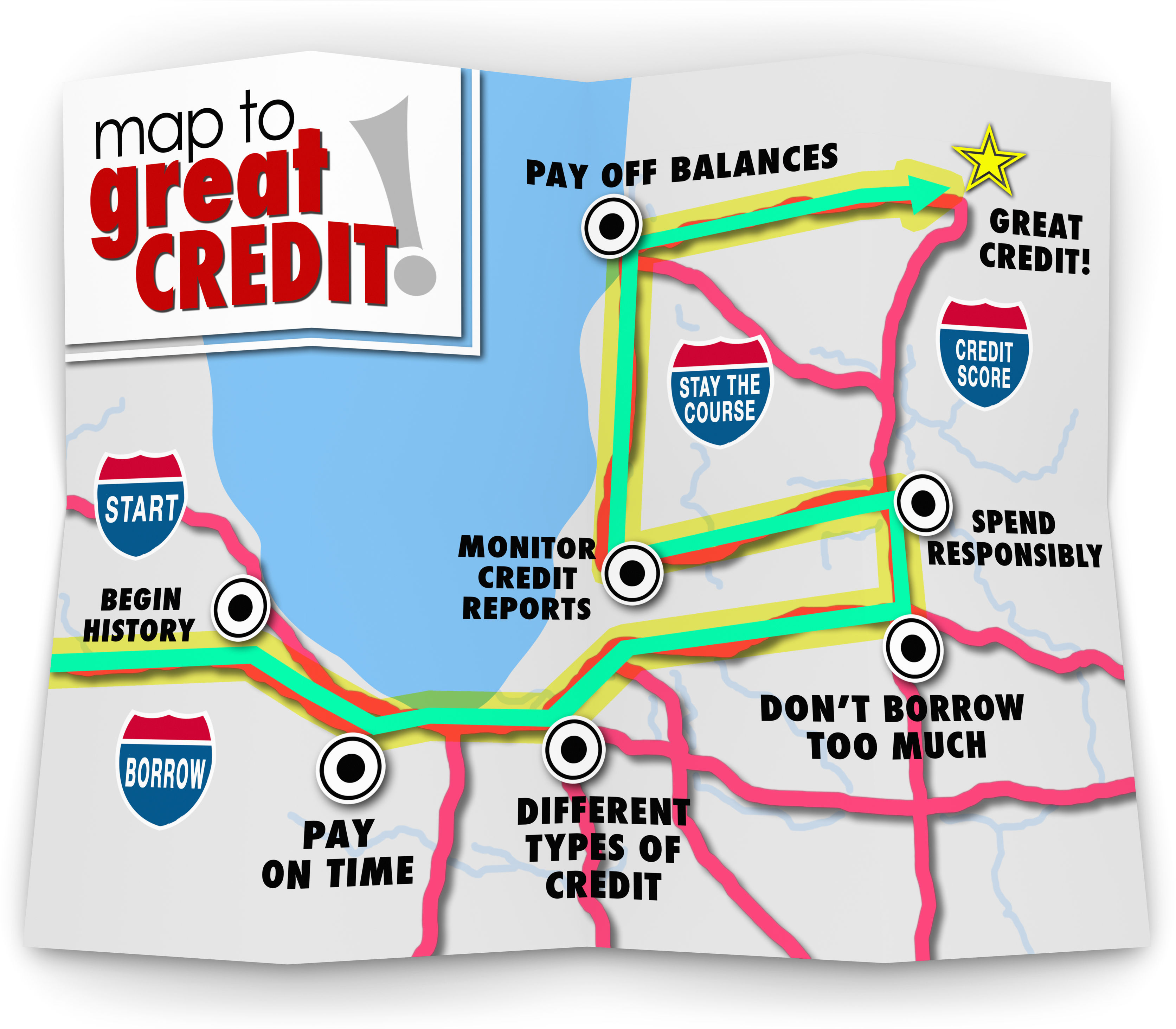

If you do have any of the neg marks mentioned above, do not give up hope. While none of these issues is good for your credit, in time they will eventually just go away. Most derogatory items merely remain on your credit report for about 7 years, along with some having the potential to disappear even sooner. As your credit history grows, the weight that these items are specified also decreases, even if they are still physically found on your report. In addition, there is a whole lot that you can do to start building your credit again nearly immediately. Considering that most of these marks are the direct result of failed payments, working out a payment strategy to pay off any balances is a solid initial step toward restoring your own personal credit.

If you struggle with this, we encourage you to take a look at our top quality X5 Credit Repair system, exclusively from Nationwide Credit Clearing. If you or someone you know has derogatory items on their report, ones that should be disputed, please give us a call. We have been helping people for 28 years improve the quality of their lives simply by working with Nationwide Credit.

Money cannot buy happiness, but it sure makes living life a lot easier. Don’t Wait, Call Now!

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

follow us on…

![]()

![]()

![]()

![]()

![]()

Most consumers are responsible – the kind who pay their bills every month and never borrow more than they can reasonably pay back. However, even the most responsible person who feels that he or she is excellent with personal finance can find him- or herself with bad credit. The reasons may be surprising, and not all of us are aware of just how much can have long-term effects on our credit reports. Here are just a few little known causes for bad credit.

Persistent Late Payments

While most consumers know how missed bill payments can negatively impact their credit reports, many don’t know that persistently paying their bills late can also have a detrimental affect. Paying a day or two late once in a while won’t be fatal, but even if you miss your payment by just one day each month, it can play a huge role in watching your credit rating plummet.

Too Many Credit Applications

Having too many credit cards or too many lines of credit can ruin your credit. Even if you pay each off each month, on time, it still makes you look like a risk to other lenders. With the higher debt you could potentially have, the worse your credit can be. You may feel responsible enough not to max out each card or each line of credit, but lenders don’t always think that way. Limiting the total credit balance available to you will go a long way in making you look more attractive to other financial institutions.

Maxing Out Your Credit Limit

Be sure not to limit yourself too much when it comes to credit cards, however. If you find that you are constantly maxing out your credit card, you will look like a credit risk, causing your credit rating to fall. Even if this limit is paid in full each month, it still indicates to other banks that you could potentially miss a payment, making you a lending risk.

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

Bad credit can affect every area of your life, from home ownership to being able to obtain a good job to replacing your car. Many people in need of credit repair simply avoid the situation, usually out of an abundance of anxiety or simply being uncertain how to proceed. This is where hiring a credit repair company can come in handy – they can help you handle the need for credit repair without putting yourself in an unfamiliar and scary situation.

Expertise and Experience

Credit repair companies have expertise in nearly every situation requiring credit repair. Some people find themselves in need because of a divorce, identity theft, or a sudden loss of employment. Whatever the reason, credit repair companies have experience in handling the situation with tact, sensitivity, and in a way that will work out best for the consumer. Think of how often you do the same task at your job, and how skilled you have become because of it. This same principle applies to credit repair companies. They have dealt with these situations on a daily basis since beginning to operate, making them experts at negotiation and at handling the unreasonable demands of creditors.

Detachment

For a person in need of credit repair, the situation is fraught with high emotions. This leaves the debtor in a bad position when trying to negotiate terms with creditors who know how to take advantage of the situation. A credit repair company is removed from the situation, putting them in a much better position to negotiate without feeling re-victimized by the process. A creditor is going to take demands made by someone who isn’t overly emotional much more serious than one who is, making a credit repair company a huge asset in this situation.

Speed

Credit repair companies help those who are in need of credit repair for a living, meaning they are significantly faster at identifying errors on a credit report and working with creditors than a debtor can. They have the time to answer calls as they come in, rather than going through the voicemail, call back, voicemail game of phone tag many debtors experience. Debtors are often busy working or dealing with other aspects of their life, and cannot handle their credit repair with the timeliness or accuracy of a credit repair company.

If you are someone who has tried to take these steps numerous times, yet can’t seem to keep up with all the chaos, then credit repair is right for you!

Why wait! Better Credit can be yours! Contact our experts at Nationwide Credit Clearing. “Home of the Free Credit Report and Consultation”

“Home of the Free Credit Report & Consultation”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

Find us on …

![]()

![]()

![]()

![]()

For many of us, opening a credit card is our first chance to start building a credit history. We believe that obtaining a credit card and using it responsibly will give us a head start on a long life of positive financial habits. Millions of credit card users are fulfilling their goal of swiping their card and paying it off each month. However, there are others who are struggling to get the money together to pay of the minimum balance. We all have a tight month every once in awhile, and paying the total balance seem so optional, compared to other bills. But what really happens when you pay the minimum balance?

How The Minimum Balance Works: Interest

As you are probably aware, you can swipe your credit card as you please, as long as you do not exceed the credit card limit. As with all debt instruments, the credit issuer gives you the option to pay the bill in its entirety or to pay a small amount to deal with at a later time. Interest will be added to the remainder, which in return will increase the price of your purchases. What is interest exactly? It is what the credit card issuer chargers their cardholders to extend the loan past the finance-free grace period. The lower your interest rate or annual percentage rate (APR), the less debt you will roll over month to month.

How Does The Minimum Balance Affect Me

Aside from the obvious, of having to pay more for your purchases due to the interest rate, there are other negative consequences to paying only the minimum balance.

What Should You Do?

Keep track of what you are spending. Make sure that you do not swipe for more than you can comfortably pay off at the end of each month. Credit cards are a great tool for building good credit. However, don’t give in to the temptation to rely on them to cover the balance of a purchase you can not afford. Just because you can spend the amount of your credit limit, does not mean that you should. Remember that your credit card activity is being watched. The credit card company will send the date of your opening to consumer credit bureaus, and every month report your activity. If you charge regularly, keep the balance at $0 and make all payments by the due date.

If you have high credit card balances, deragatory remarks, or even late payments and you just can’t seem to get yourself together enough to increase your overall credit score, there is help.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

![]()

![]()

![]()

![]()

![]()

Your credit score is made up of a calculation of different factors obtained from your credit report.

Below are the most important points to know when considering what makes up a credit score.

1. Credit Card Utilization

This percentage is calculated by taking your total credit card balances divided by your total credit card limits. It essentially shows creditors how much of your available credit you use on average. A good rule of thumb is that lower credit card utilization rates are better.

2. Percentage of On Time Payments

This is the % of payments you’ve made on time during your credit history. It’s a factor that often weighs heavily into your creditworthiness, so just one or two late payments could negatively impact your credit score. If you have missed payments, it’s best to set up automatic bill pay or create calendar reminders for bill due dates to ensure you pay on time.

3. Total Accounts

As a general rule, the more accounts you have open, the higher the likelihood that your credit score will be good. This factor indicates that more credit cards means more lenders that have been willing to take a chance on loaning to you. Having a good mix of different types of credit is important for your overall credit health. A General rule of thumb: only open accounts that you need, not ones you want!

4. Age of Credit History

The longer your credit history and the older your accounts the better. That is why it can be a good idea to keep older credit cards open and active.

5, # of Hard Inquiries

Whenever you submit an application for credit such as a credit card, mortgage or auto loan a hard credit inquiry is started on your credit report. One hard inquiry will usually have little effect, but multiple inquiries can have a larger impact. A soft inquiry happens when you check your rate to find out what you are eligible for. When you check your rates through Nationwide Credit Clearing, this is considered a soft inquiry and won’t impact your credit score in any way shape or form.

6. Derogatory Remarks

Derogatory marks are negative and represent things such as collections, tax liens or bankruptcy. These records usually stay on your credit report for Seven to Ten years. This basically tells a lender that you may have been irresponsible in the past. Unfortunately, you have to wait out the length of time in order for it to go away.

Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

The general population doesn’t know enough about Credit in general to be able to determine what exactly is and is not factored into your overall credit score. Nationwide Credit Clearing has compiled a list of these factors for you to review on your own. This is good information for everyone to understand.

Federal laws including The Consumer Credit Protection Act and the Equal Credit Opportunity Act prohibit some things from being factored into overall credit scores.

These things include:

If you or someone you know is having trouble with their credit, and needs some guidance on how to increase a credit score, Nationwide Credit Clearing can assist you.

Stop letting bad credit affect your finances! At Nationwide Credit Clearing, We help you work on your credit report and dispute unfavorable or inaccurate/outdated information. In Turn, this it will help to improve your credit score and ultimately allow you reach your future financial goals.

Don’t wait! Better Credit is just a click away! Call the experts at Nationwide Credit Clearing. “Home of the Free Credit Report and Consultation”

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

At one time in our lives, we have all made financial decisions, good or bad, that have come to affect our overall credit score. Our Credit Score ends up determining the path of our financial future.

Whether you have bad credit, bankruptcy, delinquencies, derogatory remarks or even wrong information on your credit report, watch some of these videos for your own personal knowledge or to see how Nationwide Credit Clearing can help you.

CHECK YOUR CREDIT REPORT AT LEAST ONCE/YEAR

THERE IS HELP AFTER BANKRUTPCY

HOW TO IMPROVE YOUR CREDIT AND SAVE ON INTEREST PAYMENTS

SIGNING UP FOR CREDIT CARDS AT DEPARTMENT STORES

WHAT IS A CREDIT REPORT?

Nationwide Credit Clearing is the leader in Credit Repair in the United States.

We always have to ask, When was the last time you checked your credit report? If it’s been over a year, this is where Nationwide Credit Clearing can help. Nationwide Credit Clearing has over 20 years of experience repairing credit for thousands of individuals. We have helped so many people improve their credit score by removing inaccurate, misleading or unverifiable information, ultimately changing their lives forever. We deleted over 25,000 items from credit reports in the past year.

There’s no reason to put this off and there certainly is no time like the present. Give us a shout here at Nationwide Credit. After all, We are the home of the free credit report and consultation!!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

This video explains why it’s important not to be fooled by department store discounts given to people just for opening up a new card. Todd Stern, founder of Nationwide Credit Clearing, explains “I do not advise people opening several credit cards just to get discounts”

Tips: if you do ask them if you can charge it on your main credit card which they WILL SAY YES.

Then wait a few days and call to cancel.

How to Score:

Get your 10% and be done. You don’t want to have several open credit cards it leads to nothing but confusion and possible late payments.

The Bottom Line:

Too many open cards will decrease your credit score and increase your debt.

Already have too many?

Contact Nationwide Credit Clearing for your free credit report and consultation today.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com/index.php/contact-us/

Credit card fraud is a serious matter. For victims, it can be a frightening experience. While no one wants to live a life looking over their shoulder, credit card theft can happen at the most unexpected times. While there is no guarantee that anyone is exempt from becoming a VICTIM OF IDENTITY THEFT, there are certain things you can do to decrease your chances of falling victim to credit fraud.

**Check ATMs and gas pumps for loose partsparts or suspicious keypads. If you find something suspicious, you should inform the gas station or bank, and transact your business at another machine.

**Check your credit card statements for unusual charges. CHECKING YOUR CREDIT REPORT on a regular basis can help you react quicker to fraud or identity theft.

**Be careful when accessing the Internet in public venues. Unlike home or office WiFi networks, there are a large number of WiFi spots that do not encrypt the data being transmitted through them. Your email, bank account, and credit card information could be fair game for a hacker with the right skills. Never share personal information with a stranger on social media sites and try to limit the personal information you share with your friends.

**Don’t carry information in your wallet or purse that you do not need. Birth certificates, Social Security cards, PIN numbers and passwords can be easily stolen. Identity thieves can be long gone before you become aware of any missing information.

**Shred documents with personal information before you throw them away. Identity theft crimes are usually thought of as being high-tech in nature. There are still identity thieves who do not mind foraging through a dumpster for valuable information.

Think You May Be a Victim of Fraud?

IF YOU suspect you are a victim of identity theft or fraud, you may want to consider adding a 90-day fraud alert to your credit report. A fraud alert warns lenders that you may be a victim so they can take additional steps to verify your identity before approving a loan application. Immediately inform creditors when you suspect or have proof of fraud. Take time to document every contact. Make sure you thoroughly understand the process of reporting fraud and what is expected of both you and the creditor.

Preventing credit card fraud takes awareness and effort. Protecting your personal and credit card information is probably one of the most important steps you could take to prevent Credit Card Fraud.

For more information or if you have been a victim of Credit Card Fraud, Contact Nationwide Credit Clearing