-

-

Quick Contact

Get A free

Consultation Now!

Tag Archives: credit cards

All about your Credit Score

Your Credit History plays a huge role in everything you do in life. From getting a job to applying for loans, your credit score is factored in everywhere. A credit score is a screenshot taken by the 3 major credit bureaus, Experian, TransUnion, and Equifax. This gives lenders the ability to determine whether or not you will be given credit, the total amount of credit you are granted as well as the terms on your loan, (loan amount, interest rate and repayment schedule).

Below you will find information about credit scores as well as some simple steps to keep them high, all which are crucial for you in determining your financial future.

What is a credit score and how is it calculated?

Your credit score is usually a number that ranges between 300 & 850 and it’s used by creditors to determine if you are responsible and worthy of obtaining credit based on many factors. Many of the businesses that you have a credit line or a loan will send reports to these 3 bureaus of credit info such as whether or not you pay bills on time, your total credit amount, and even your credit history going back many years. A credit score is calculated simply from your individual credit history. Someone with a higher credit score, will have the ability to borrow more money. However, when your credit score is low, you may be able to obtain loans, but your interest rates will be much higher. Generally, a score of 700+ is considered GOOD while a score of 600 or below is considered very POOR.

Everyone has the ability and should take the opportunity to get a free credit report from each of the 3 bureaus once per year. All three bureaus offer this to us, but many of us don’t take advantage nor pay attention. It’s important to check your credit score to determine if it’s accurate because your score will be used to determine your financial future.

So How do I increase my credit score?

This is not a quick fix, when trying to increase your credit score, however, you can take steps to repair your score over time.

Here is our advice:

*Payment history is important so always pay your bills on time

*You never want to max out any of your credit cards. In fact, keeping your balance at 30% of your total limit is ideal.

*Don’t apply for new credit unless it’s absolutely necessary.

*Even when you pay off a card, keep it open to increase the length of your credit history

*Pay your high balance cards first, and never just transfer debts among a variety of lenders.

*If you have collections or past due accounts, settle them

*If you find inaccurate items in your credit report, make sure to dispute them.

*Usually, The last 2 years of your credit history are the most valuable

Your Credit Score will affect your life in many ways.. good or bad!

Credit scores are often used in determining prices for home or car loans as well as homeowners insurance. Employers will also check your credit score as part of background checks when making the final decision as to whether to hire you or not. Although it may not seem fair, credit scores have become more prevalent and are now used in nontraditional ways to judge you as a person.

Nevertheless, It’s more important than ever to become educated about Credit Scores.

This leads us to the final question.. When was the last time you checked your credit score?

If it’s been a while, Nationwide credit Clearing can help. We are the leaders in Credit Repair and are here to help you in making your future financial decisions or correcting mistakes you have made in the past.

So what are you waiting for? Call Nationwide credit Clearing today and get started with your free credit report and consultation.

Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

How Often is My Credit Report Updated?

When it comes to timing and payment of credit cards, information is not updated as frequently as most consumers would like for it to be.

Credit report lag is a huge cause of confusion for Consumers. Once you pay off a credit card, it becomes exciting to see the changes this makes on your overall score; however, credit reports are not updated right away, meaning you may not see a change for a little while. Ugh… How disappointing!!

Prior to deciding to freak out and believe something must be incorrect understand that, generally, creditors forward info like balance updates and new accounts to credit reporting agencies monthly, not daily. The primary factor to take into account is not that every financial institution reports to all 3 of the credit bureaus unfortunately. Additionally, each creditor updates their system on different days of the month, so although you may have paid off all of the credit cards on the same day, the latest balances most likely are not going to be reported at the same time.

You should always familiarize yourself with how public records & hard inquiries are reported. When it comes to hard inquiries, like applying for loans, credit bureaus update inquiry information right there and then, which means you can view this info pretty much as soon as it is dispatched. However, when it comes to public records such as bankruptcies, tax liens & judgements, the process is never the same. Even if you have addressed a long standing delinquency, the credit bureaus more than likely will not receive the updated info right away, especially since every court has different conditions when reporting public records.. In general, negative marks usually stay on your credit report for many years, so many times; a quick fix just isn’t possible. Of course it’s not what we want, but it just is what it is.

Since changes do take some time, it is very important for you to remain patient in seeing positive changes. If you can give it a month or maybe even 2 before you expect the changes, this will allow you to keep your sense of sanity.. So just keep that in mind. However, it is always to remain mindful about when you have made pmts or had negative marks eliminated, how many accounts you ought to have open along with the info that all 3 bureaus have on your file. In the event that you notice incorrect or outdated information on your credit report, you’ll be able to file a dispute with the 3 credit bureaus that are reporting the wrong information. If you need help figuring out how to dispute something on your credit report, call Nationwide Credit Clearing.

All in all, nothing will help keep you on top of things like a little bit of patience and diligence. So the next time you check on your credit, keep in mind patience is a virtue!!

On another note, if you have not even checked your credit report due to you being afraid to see what is on there, it’s not doing you due diligence. This is where Nationwide Credit Clearing comes in. Nationwide Credit Clearing has over 20 years of experience repairing credit of all types. We have helped thousands of people improve their credit score by removing inaccurate, misleading or unverifiable information. We deleted over 25,000 items last year alone.

So don’t be afraid, there is no time like the present. Give us a shout here at Nationwide Credit. We are the home of the free credit report and consultation!!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

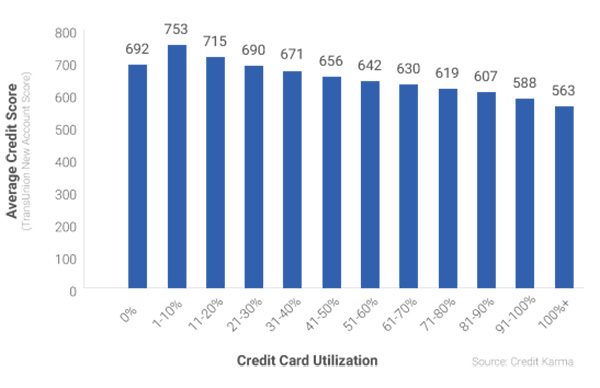

Your Credit Score & Credit Utilization Rates Have A Very Distinct Relationship

One of the most important things credit companies do to factor in your total credit score is they look at your balance to limit ratio. Your rate of utilization is simply the percentage of the total limit based upon your current balance.

To illustrate how important this factor is, Credit Karma sampled approximately 15 million Credit Karma members who visited the site in 2014 and compared their credit scores and corresponding credit card utilization rates. (Graph Provided by Creditcarma.com)

The Facts:

The correlation here is very easy to see. If you max out your card, and don’t pay it down, you are going to have problems. The lower the utilization rate, the higher your score, that is, with the exception zero utilization. As you can also see, not using your card at all is not the best option. The better choice would be to use the card for purchase during the month, then always keep that utilization at about 30%. This gives you credibility and proves to creditors that you can be responsible with money.

What this Means…

Lenders don’t like high utilization rates because it tends to indicate there’s a higher chance of you not being able to repay debt. Keeping your credit card utilization low at about 30% is the most ideal range. Creditors need to see proof, long term, that you can manage money and credit–something you can’t do without using the credit you’re granted.

If you’re uncomfortable with the idea of using your card for large purchases, you can still show an active credit profile by paying for small items with your card. It’s important that you practice good habits when managing your credit cards. Charge what you can pay back and make sure your payments are on time. In order to keep your utilization rate greater than 0%, you’ll need to let your charges show up on your billing statement, and then you can pay it off in full. This does not mean you need to carry a balance from one month to the next–doing so may just cost you money in the form of interest.

Credit utilization is just one of many factors when generating an overall score

Credit card utilization % is definitely an important aspect of your credit worthiness, and more than likely will have a significant impact on credit health, but it’s not the only factor these lenders care about. Basically, and what it comes down to, is it is not impossible for people who have high credit utilization rates to still have good credit scores, just as long as the other factors are all good– but it’s definitely not something that typically happens.

Question: When was the last time you even Checked your Credit Score?

If it’s been a while, it’s probably time to catch up. Nationwide Credit Clearing is the home of the free credit report and consultation. Not only will we provide you with an accurate view of where you stand as far as credit worthiness, but we can then help you by taking the existing derogatory items, late payments, etc.. and helping to remove them from your credit altogether.

We have helped thousands live a better life, free from credit hangups. Call today for your free report!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

![]()

Lower credit score?

How is it that you can actually get a lower credit score when you feel like your spending habits have gotten better? Learn why your credit scores might have dropped since you last checked them by using this informative infographic below:

In summary, here are 5 solid reasons your credit score may have recently dropped:

1. 30 plus days late on payments

2. Credit Card balances exceed 30% total

3. Closing an old account

4. Too many Credit Card Inquiries

5. Identity Theft may have racked up debt without you knowing.

If this seems overwhelming to you, it’s important to call a credit repair company such as Nationwide Credit Clearing

Our Family of Experts is Ready To Get You Back To Healthy Credit

LET US HELP YOU SOLVE YOUR CREDIT TROUBLE (773) 862-7700

Nationwide Credit Clearing, the home of the Free Credit report and Consultation.

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

CLICK BELOW FOR YOUR…

![]()

What impact do late payments have on your Credit Score?

Making late payments on your, mortgage, credit cards or loans will affect your overall credit health as well as hurt your credit score. Regardless of how late you pay, even one day late will count against you. Generally speaking, if your bills are not paid on or before the due date, this could affect you in the long haul.

Late Payments: How they Affect Your Credit

Banks as well as issuers consider the history of your payments especially after evaluating your overall credit risk & deciding if they should or should not approve you for the loan. A lengthy history of payments (on-time ) demonstrates that you are a reliable & responsible borrower.

However, a lengthy history of late payments will suggest that you are not qualified nor responsible to borrow money from a bank. The inability to be reliable is a huge red flag to banking institutions, and here are just a few things that can easily occur when you pay late.

- IT WILL END UP ON YOUR CREDIT REPORT

- INTEREST RATES WILL BE LIKELY TO RISE

- IT CAN DECREASE YOUR CREDIT SCORE

- YOU WILL END UP PAYING LATE FEES

Making late payments is a habit that could end in more damaging credit actions.

If you neglect an account until it is sent to collections or becomes delinquent, that will play a huge factor in your credit score drop. An account in collections may remain on your credit report for 7 years & cause more damage than a single late payment.

What to Do if You Have Late Payments on your Credit Report

A Simple Solution!

Credit Repair. Credit Repair is the process of identifying, disputing, and monitoring negative information on your credit report. Nationwide Credit Clearing has been helping people all over the US delete negative information from their credit past. Whether you have late payments, medical bills, or even bankruptcy, Nationwide Credit can help you get back to a state of healthy Credit.

Contact Nationwide Credit Clearing for your free credit report and consultation today.

Nationwide Credit Clearing

“HOME OF THE FREE CREDIT REPORT AND CONSULTATION”

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com/index.php/contact-us/

Department Stores Credit Cards. Good or Bad Idea?

This video explains why it’s important not to be fooled by department store discounts given to people just for opening up a new card. Todd Stern, founder of Nationwide Credit Clearing, explains “I do not advise people opening several credit cards just to get discounts”

Tips: if you do ask them if you can charge it on your main credit card which they WILL SAY YES.

Then wait a few days and call to cancel.

How to Score:

Get your 10% and be done. You don’t want to have several open credit cards it leads to nothing but confusion and possible late payments.

The Bottom Line:

Too many open cards will decrease your credit score and increase your debt.

Already have too many?

Contact Nationwide Credit Clearing for your free credit report and consultation today.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com/index.php/contact-us/

X-5 Credit Repair System

New X5 Credit Repair is the newest software that has been rolled out by Nationwide Credit Clearing. This software is the most cutting edge on the market today. once you become a client, you will be able to login to your account online to view the status as well as send email updates frequently regarding the status of your deleted items.

Along with that, everytime your file is updated, you will receive a text message regarding the changes.

On another note, if you just happen to be a mortgage broker and you refer a client to Nationwide Credit, you will automatically become an agent so you can check on the status of potential clients credit reports and deletions.

Remember, Nationwide Credit Clearing is the #1 Credit Repair company in the industry, providing you with the ultimate in credit repair technology… contact us today for your FREE credit report and consultation.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

![]()

Debt Solutions: Ways to Begin Eliminating Credit Card Debt

A lot of people end up with staggering credit card debt. Even though it seems overwhelming, trimming your financial allowance through small changes in your lifestyle might help.

Debt Solutions: Day-To-Day Savings

Take a seat and consider the amount of money you would spend throughout the week on coffee, lunches and takeout dinners. Somebody who spends $ 5 each day in the coffeehouse is looking at Hundred Dollar expenditure throughout the course of the month. Invest that first month’s savings on a at home coffee maker and travel mug so you’re able to take the coffee from your home. The same goes for your morning breakfast. You will begin to see extra cash in your pocketbook right away.

For lunch time, take the brown bag with you. The $10 or more you spend every day on one salad or perhaps a sandwich leads to over $200 monthly. Instead, buy salad fixings or lunch meat at the supermarket. For anybody who typically runs late each and every morning, pack your lunch the evening before to prevent adding precious minutes towards your morning routine.

This may be the toughest adjustment for families on the go, but it’s time to cut back on takeout dinners. These quickie meals are budget busters. A few cartons of Chinese food or a couple of pizzas can easily run you $30 or more a pop. Instead, keep frozen prepared meals on hand for those nights when cooking isn’t an option. Double your recipes and freeze batches of soup, chili and casseroles on weekends when you have time to cook. Even frozen prepared foods from the grocery store will save you considerable amounts of money. Avoiding expensive takeout even twice a week can save nearly $250 a month.

Debt Solutions: Monthly Payments

The initial place to search for simple savings is in your mobile phone, cable and Internet fees. Chances are you’re spending money on features you are not using. For people with every cable channel but aren’t big on watching TV, contact your cable company to find out what packages are available that still offer what you need. Your cell phone bill could possibly be another budget drain which can be trimmed through careful research of packages available.

You could search for a bundle package that provides you significantly lower rates on your Internet, mobile phones and cable by utilizing the same company for all those. Comparison-shop between providers and do not hesitate to let them understand what you have been proposed by their competitors. This tactic is known to sweeten many deals.

Debt Solutions: Big-Ticket Items

Make the most use out of your expensive items before replacing them. Keep appliances, cars and electronics until they are no longer useful instead of purchasing every new item that comes on the market. You could be in need of that new tablet, but stick to the existing laptop for a bit — it is not costing you anything at all. Invest a few bucks in repairs to maintain your big-ticket belongings in good condition, and wait to buy new items before you look for a deal you simply can’t pass by.

Now that you know more about how to eliminate credit card debt, get your FREE credit report & consultation from the #1 Chicago Credit Repair Company, Nationwide Credit Clearing.

![]()

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

find us on…

![]()

![]()

![]()

![]()

![]()

The Twelve Days of Credit

The Twelve Days of Credit: A guide to unanswered questions about your Credit Report and History….

The Twelve Days of Credit: A guide to unanswered questions about your Credit Report and History….

1. Did you know an FTC study found that about 25 Percent of Credit Reports could contain errors?

2. Some credit scoring models essentially count multiple hard inquiries, as one. As long as both loans are for the same type – ie auto or mortgage – and within a short period of time.

3. Loans you have co-signed for could appear on your credit report the same as your other accounts do. If you are thinking of co-signing, consider your own credit score as well.

4. If you are concerned about Identity Theft, a Fraud alert could make it more difficult for someone to open a new account in your name.

5. Make sure to track your Credit Utilization Rate. Try keeping your Credit Card Utilization Rate below 30%. Higher utilization rates could negatively affect your overall Credit Score

6. Lenders could close your accounts due to inactivity. To keep your current credit accounts active, try to use them regularly for at least small purchase. Of Course you should never forget to pay your bills!

7. Adverse Accounts are accounts in which information may lead potential creditors to view you as a risk. Account information includes name, address and phone number of creditor, your account number, current balance and highest balance, account limit, account status, account type and the date you opened the account. The report lists how much money is past due and how many times the account a payment has been made 30/60/90 days late. Bankruptcies, liens, foreclosures and judgments will be listed in this section.

8. Debt Validation is a consumer’s right to challenge a debt and/or receive written verification of a debt from a debt collector.

9. If you are considering using Credit Cards to earn cash back or rewards points this

Season, be sure to read the fine print. Some cards require you to enroll in rotating categories or have other limits on rewards. Always check and ask your credit card issuer for specific Details.

10. Most bankruptcies filed in the Unites States are either Chapter 7 or Chapter 13 cases.

So what is The Difference?

• Chapter 7 is a liquidation bankruptcy designed to wipe out your general unsecured debts such as credit cards and medical bills. To qualify for Chapter 7 bankruptcy, you must have little or no disposable income.

• Chapter 13 is a reorganization bankruptcy designed for debtors with regular income who can pay back at least a portion of their debts through a repayment plan. If you make too much money to qualify for Chapter 7 bankruptcy, you may have no choice but to file a Chapter 13 case.

11. Late or missed payments Can and Will reduce your overall credit score. Considering enrolling in auto-pay if you are a busy person who tends to be forgetful.

And on the TWELFTH day of Credit …someone brought up Credit Repair….

12. Credit Repair is the easiest and fastest way to increase your overall Credit Score. We work hard to dispute unfavorable or derogatory items that currently exist on your Credit Report. One should consider Credit Repair when looking to buy a new car, a new home, or anything that involves the need to present your personal credit score.

About Nationwide Credit Clearing…

Nationwide Credit Clearing has been in the credit repair business for 28 years. Nationwide Credit is the “high end boutique” of credit repair. We handle all of the work for the clients from start to finish. We give the client a free credit report consultation on day one. For us. however, It’s not just about signing up clients- we want to help them reach their goals. We Care!

Nationwide Credit is the largest credit repair company in Chicago and was told by one of the major credit bureaus six years ago that we were one of the top 3 largest companies in the country. Having such volume going through our company has opened up the doors with the credit bureaus. Two out of the three updated credit reports are sent directly to the Nationwide Credit corporate office.

Now, isn’t it time you checked your current credit score? It’s easy, just Contact us Below:

![]()