-

-

Get A free

Consultation Now!

Credit Cards

Paying only the Minimum Credit Card Balance

For many of us, opening a credit card is our first chance to start building a credit history. We believe that obtaining a credit card and using it responsibly will give us a head start on a long life of positive financial habits. Millions of credit card users are fulfilling their goal of swiping their card and paying it off each month. However, there are others who are struggling to get the money together to pay of the minimum balance. We all have a tight month every once in awhile, and paying the total balance seem so optional, compared to other bills. But what really happens when you pay the minimum balance?

How The Minimum Balance Works: Interest

As you are probably aware, you can swipe your credit card as you please, as long as you do not exceed the credit card limit. As with all debt instruments, the credit issuer gives you the option to pay the bill in its entirety or to pay a small amount to deal with at a later time. Interest will be added to the remainder, which in return will increase the price of your purchases. What is interest exactly? It is what the credit card issuer chargers their cardholders to extend the loan past the finance-free grace period. The lower your interest rate or annual percentage rate (APR), the less debt you will roll over month to month.

How Does The Minimum Balance Affect Me

Aside from the obvious, of having to pay more for your purchases due to the interest rate, there are other negative consequences to paying only the minimum balance.

- Your Credit Score Will Fall: Making a minimum payment on your credit card is a quick solution for when you are short on cash. But the debt that you rack up over the course of a few months of minimum payments, will really mess up your credit score. 30% of your credit score is determined by how much debt you carry. Accruing charges on your credit card and failing to pay them off is like putting a dent in your credit score every month. Over time, this will add up to a lot of damage.

- Your Monthly Bills Will Pile Up: As a result of the damage you will be doing to you credit score with minimum payments, other monthly bills will expensive to. These include obligations such as insurance, rent, and loans. Lenders and insurance companies tend to charge people with poor credit more.

- Credit Card Costs Will Skyrocket: One of the most obvious impacts of minimum payments, is the unpaid balance building up. The average interest rate on a credit card is 15%, it will become very expensive to fail to pay off your balance in full. Additionally a lot of credit card companies charge a fee for exceeding your credit limit. When you are only paying off the minimum balance, this is quite easy to do.

What Should You Do?

Keep track of what you are spending. Make sure that you do not swipe for more than you can comfortably pay off at the end of each month. Credit cards are a great tool for building good credit. However, don’t give in to the temptation to rely on them to cover the balance of a purchase you can not afford. Just because you can spend the amount of your credit limit, does not mean that you should. Remember that your credit card activity is being watched. The credit card company will send the date of your opening to consumer credit bureaus, and every month report your activity. If you charge regularly, keep the balance at $0 and make all payments by the due date.

If you have high credit card balances, deragatory remarks, or even late payments and you just can’t seem to get yourself together enough to increase your overall credit score, there is help.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

6 Financial Mistakes Young People Make

Whether you just graduated from college or are moving out on your own, it can be hard to keep track of your personal finances as a young adult. Read through these 6 common financial mistakes and learn how you can avoid them.

1. Not Taking Advantage of Discounts: There is a world of special prices for students and young people out there, from banks to movie theatres – take advantage of them! Do your research beforehand, find out what discounts are available to you. Check out Groupon or Retail Me Not.

1. Not Taking Advantage of Discounts: There is a world of special prices for students and young people out there, from banks to movie theatres – take advantage of them! Do your research beforehand, find out what discounts are available to you. Check out Groupon or Retail Me Not.

2. Misunderstanding Credit Cards: Whether it be cash advances, large balances, late fees, or only playing the minimum balance, credit cards can lead to much more trouble than realized. The fine print and details of credit cards are often times misunderstood by young people. Read into what you are signing up for and ask plenty for questions when you do not understand something.

3. Signing Up For A Rental Or Mortgage That Is Too Expensive: Signing a lease for rent or applying for a mortgage that leaves you with little money to do anything else, will not only leave you at home but put you at risk for debt. You have no cash at hand, so what do you do? Sign up for credit cards to make up the difference in order to enjoy your lifestyle and pay for unexpected costs. Avoid making this mistake, sign up for a lease or mortgage that is within your budget in order to avoid creating debt for yourself.

4. No Rainy Day Fund: Setting aside money for emergencies gives you cushion for unexpected events and helps you avoid adding to your credit card balance. Maybe your car got towed, or you get injured, having a “rainy day” fund keeps you prepared for the most unexpected events. Including a “rainy day” fund as a part of your budget, will eventually help the money add up.

5. Failure To Realize How “Little Things” Add Up: Your daily coffee stops, eating lunch out, or weekly shopping trip of $100, can all add up to thousands of dollars a year. Cutting back can help you save a lot of money for savings, retirement or paying down your debt.

6. No Financial Planning Or Budget: Some young people are tainted by the idea that saving for the future is only for people thinking about retirement. Everyone can benefit from financial saving whether you are planning for retirement, purchasing a home, or traveling around the world. It is also important to budget your daily expenses. Sit down and look at what is left after your wages and fixed expenses. Not knowing how much you have can easily lead to spending more than you can afford. A budget will help you determine what you need to do to pay for your next vacation.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com

All about your Credit Score

Your Credit History plays a huge role in everything you do in life. From getting a job to applying for loans, your credit score is factored in everywhere. A credit score is a screenshot taken by the 3 major credit bureaus, Experian, TransUnion, and Equifax. This gives lenders the ability to determine whether or not you will be given credit, the total amount of credit you are granted as well as the terms on your loan, (loan amount, interest rate and repayment schedule).

Below you will find information about credit scores as well as some simple steps to keep them high, all which are crucial for you in determining your financial future.

What is a credit score and how is it calculated?

Your credit score is usually a number that ranges between 300 & 850 and it’s used by creditors to determine if you are responsible and worthy of obtaining credit based on many factors. Many of the businesses that you have a credit line or a loan will send reports to these 3 bureaus of credit info such as whether or not you pay bills on time, your total credit amount, and even your credit history going back many years. A credit score is calculated simply from your individual credit history. Someone with a higher credit score, will have the ability to borrow more money. However, when your credit score is low, you may be able to obtain loans, but your interest rates will be much higher. Generally, a score of 700+ is considered GOOD while a score of 600 or below is considered very POOR.

Everyone has the ability and should take the opportunity to get a free credit report from each of the 3 bureaus once per year. All three bureaus offer this to us, but many of us don’t take advantage nor pay attention. It’s important to check your credit score to determine if it’s accurate because your score will be used to determine your financial future.

So How do I increase my credit score?

This is not a quick fix, when trying to increase your credit score, however, you can take steps to repair your score over time.

Here is our advice:

*Payment history is important so always pay your bills on time

*You never want to max out any of your credit cards. In fact, keeping your balance at 30% of your total limit is ideal.

*Don’t apply for new credit unless it’s absolutely necessary.

*Even when you pay off a card, keep it open to increase the length of your credit history

*Pay your high balance cards first, and never just transfer debts among a variety of lenders.

*If you have collections or past due accounts, settle them

*If you find inaccurate items in your credit report, make sure to dispute them.

*Usually, The last 2 years of your credit history are the most valuable

Your Credit Score will affect your life in many ways.. good or bad!

Credit scores are often used in determining prices for home or car loans as well as homeowners insurance. Employers will also check your credit score as part of background checks when making the final decision as to whether to hire you or not. Although it may not seem fair, credit scores have become more prevalent and are now used in nontraditional ways to judge you as a person.

Nevertheless, It’s more important than ever to become educated about Credit Scores.

This leads us to the final question.. When was the last time you checked your credit score?

If it’s been a while, Nationwide credit Clearing can help. We are the leaders in Credit Repair and are here to help you in making your future financial decisions or correcting mistakes you have made in the past.

So what are you waiting for? Call Nationwide credit Clearing today and get started with your free credit report and consultation.

Nationwide Credit Clearing

2336 N Damen

First Floor

Chicago, IL 60647

773-862-7700

877-334-3296

FAX: 773-862-7703

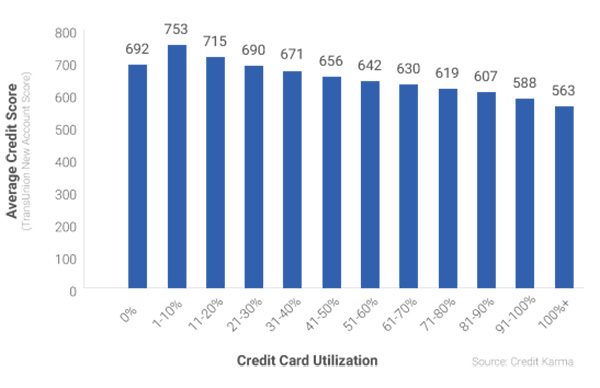

Your Credit Score & Credit Utilization Rates Have A Very Distinct Relationship

One of the most important things credit companies do to factor in your total credit score is they look at your balance to limit ratio. Your rate of utilization is simply the percentage of the total limit based upon your current balance.

To illustrate how important this factor is, Credit Karma sampled approximately 15 million Credit Karma members who visited the site in 2014 and compared their credit scores and corresponding credit card utilization rates. (Graph Provided by Creditcarma.com)

The Facts:

The correlation here is very easy to see. If you max out your card, and don’t pay it down, you are going to have problems. The lower the utilization rate, the higher your score, that is, with the exception zero utilization. As you can also see, not using your card at all is not the best option. The better choice would be to use the card for purchase during the month, then always keep that utilization at about 30%. This gives you credibility and proves to creditors that you can be responsible with money.

What this Means…

Lenders don’t like high utilization rates because it tends to indicate there’s a higher chance of you not being able to repay debt. Keeping your credit card utilization low at about 30% is the most ideal range. Creditors need to see proof, long term, that you can manage money and credit–something you can’t do without using the credit you’re granted.

If you’re uncomfortable with the idea of using your card for large purchases, you can still show an active credit profile by paying for small items with your card. It’s important that you practice good habits when managing your credit cards. Charge what you can pay back and make sure your payments are on time. In order to keep your utilization rate greater than 0%, you’ll need to let your charges show up on your billing statement, and then you can pay it off in full. This does not mean you need to carry a balance from one month to the next–doing so may just cost you money in the form of interest.

Credit utilization is just one of many factors when generating an overall score

Credit card utilization % is definitely an important aspect of your credit worthiness, and more than likely will have a significant impact on credit health, but it’s not the only factor these lenders care about. Basically, and what it comes down to, is it is not impossible for people who have high credit utilization rates to still have good credit scores, just as long as the other factors are all good– but it’s definitely not something that typically happens.

Question: When was the last time you even Checked your Credit Score?

If it’s been a while, it’s probably time to catch up. Nationwide Credit Clearing is the home of the free credit report and consultation. Not only will we provide you with an accurate view of where you stand as far as credit worthiness, but we can then help you by taking the existing derogatory items, late payments, etc.. and helping to remove them from your credit altogether.

We have helped thousands live a better life, free from credit hangups. Call today for your free report!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

![]()

Lower credit score?

How is it that you can actually get a lower credit score when you feel like your spending habits have gotten better? Learn why your credit scores might have dropped since you last checked them by using this informative infographic below:

In summary, here are 5 solid reasons your credit score may have recently dropped:

1. 30 plus days late on payments

2. Credit Card balances exceed 30% total

3. Closing an old account

4. Too many Credit Card Inquiries

5. Identity Theft may have racked up debt without you knowing.

If this seems overwhelming to you, it’s important to call a credit repair company such as Nationwide Credit Clearing

Our Family of Experts is Ready To Get You Back To Healthy Credit

LET US HELP YOU SOLVE YOUR CREDIT TROUBLE (773) 862-7700

Nationwide Credit Clearing, the home of the Free Credit report and Consultation.

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

CLICK BELOW FOR YOUR…

![]()

Department Stores Credit Cards. Good or Bad Idea?

This video explains why it’s important not to be fooled by department store discounts given to people just for opening up a new card. Todd Stern, founder of Nationwide Credit Clearing, explains “I do not advise people opening several credit cards just to get discounts”

Tips: if you do ask them if you can charge it on your main credit card which they WILL SAY YES.

Then wait a few days and call to cancel.

How to Score:

Get your 10% and be done. You don’t want to have several open credit cards it leads to nothing but confusion and possible late payments.

The Bottom Line:

Too many open cards will decrease your credit score and increase your debt.

Already have too many?

Contact Nationwide Credit Clearing for your free credit report and consultation today.

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

http://mynationwidecredit.com/index.php/contact-us/

Own up to your Credit : Good or Bad

We all have made major mistakes either currently or in the past, especially when it’s regarding Money, Credit and Financial well being. Understand how you can set your self on a more effective financial route by owning up to most of your undesirable $$$ mistakes.

No one’s perfect – particularly when you are looking at managing your hard earned dollars. As you may always keep track of your funds, budget intelligently & spend well now, you may have made some significant money errors while you were young. Since having money does not come with an owner’s manual, you may have had lackadaisical spending ways or went wild with credit before you smartened up & began taking money as serious as you need to. Still, those past sins may come directly back to haunt you .. by way of creditors or really low credit scores. Your best bet would be to face money concerns head-on & compensate for those missteps before you can move on to more positive spending patterns in the future.

While confronting financial mistakes from your past, it is easy to turn a blind eye and hope they simply go away. However when you must pay back money or go into default on loans, not just are those creditors still looking to get paid, it will probably affect your long-term ability to secure funding & have what we like to call, Financial Freedom, in the near future. Rather, gather up all of your statements and read through them with a microscope to give you a general picture of which mistakes you’ve created & which can be easily rectified with a little bit of knowledge as well as hard work.

Understanding your credit is crucial.

So is a great score.

Get your credit report & Consultation NOW. Why wait? Call Today!

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

Debt Solutions: Ways to Begin Eliminating Credit Card Debt

A lot of people end up with staggering credit card debt. Even though it seems overwhelming, trimming your financial allowance through small changes in your lifestyle might help.

Debt Solutions: Day-To-Day Savings

Take a seat and consider the amount of money you would spend throughout the week on coffee, lunches and takeout dinners. Somebody who spends $ 5 each day in the coffeehouse is looking at Hundred Dollar expenditure throughout the course of the month. Invest that first month’s savings on a at home coffee maker and travel mug so you’re able to take the coffee from your home. The same goes for your morning breakfast. You will begin to see extra cash in your pocketbook right away.

For lunch time, take the brown bag with you. The $10 or more you spend every day on one salad or perhaps a sandwich leads to over $200 monthly. Instead, buy salad fixings or lunch meat at the supermarket. For anybody who typically runs late each and every morning, pack your lunch the evening before to prevent adding precious minutes towards your morning routine.

This may be the toughest adjustment for families on the go, but it’s time to cut back on takeout dinners. These quickie meals are budget busters. A few cartons of Chinese food or a couple of pizzas can easily run you $30 or more a pop. Instead, keep frozen prepared meals on hand for those nights when cooking isn’t an option. Double your recipes and freeze batches of soup, chili and casseroles on weekends when you have time to cook. Even frozen prepared foods from the grocery store will save you considerable amounts of money. Avoiding expensive takeout even twice a week can save nearly $250 a month.

Debt Solutions: Monthly Payments

The initial place to search for simple savings is in your mobile phone, cable and Internet fees. Chances are you’re spending money on features you are not using. For people with every cable channel but aren’t big on watching TV, contact your cable company to find out what packages are available that still offer what you need. Your cell phone bill could possibly be another budget drain which can be trimmed through careful research of packages available.

You could search for a bundle package that provides you significantly lower rates on your Internet, mobile phones and cable by utilizing the same company for all those. Comparison-shop between providers and do not hesitate to let them understand what you have been proposed by their competitors. This tactic is known to sweeten many deals.

Debt Solutions: Big-Ticket Items

Make the most use out of your expensive items before replacing them. Keep appliances, cars and electronics until they are no longer useful instead of purchasing every new item that comes on the market. You could be in need of that new tablet, but stick to the existing laptop for a bit — it is not costing you anything at all. Invest a few bucks in repairs to maintain your big-ticket belongings in good condition, and wait to buy new items before you look for a deal you simply can’t pass by.

Now that you know more about how to eliminate credit card debt, get your FREE credit report & consultation from the #1 Chicago Credit Repair Company, Nationwide Credit Clearing.

![]()

Nationwide Credit Clearing

2336 N. Damen

First Floor

Chicago, IL 60647

Phone: 773-862-7700

Toll Free: 877-334-3296

Fax: 773-862-7703

E-Mail: support@mynationwidecredit.com

find us on…

![]()

![]()

![]()

![]()

![]()