-

-

Get A free

Consultation Now!

Author Archives: Norm Schriever

Millions of Americans get a credit score boost because of new scoring rules. Will your score go up?

While millions of Americans just filed their taxes in hopes of a big refund, consumers may be getting some good financial news in another arena: their credit scores. That’s because the three major credit reporting bureaus – Experian, Equifax, and Transunion, just reported that they’ll start excluding tax liens from their credit scoring algorithms.

While millions of Americans just filed their taxes in hopes of a big refund, consumers may be getting some good financial news in another arena: their credit scores. That’s because the three major credit reporting bureaus – Experian, Equifax, and Transunion, just reported that they’ll start excluding tax liens from their credit scoring algorithms.

In a concerted effort to improve the accuracy and fairness of their scoring models in respect to public records, a significant number of Americans will see their credit scores jump, virtually overnight (the changes took place April 16.)

The push for reformatting the way judgments and tax liens are factored into credit scoring comes after a study from the Consumer Financial Protection Bureau revealed that incorrect, outdated, or otherwise erroneous information too-often showed up in credit files, sinking that person’s score. So, starting last July, the credit bureaus started their clean sweep of civil judgment data from credit reports, including some tax lien reporting. This April 16, they finished that job.

To be clear, the vast majority of Americans won’t see any difference if they check their credit score again. According to the IRS and other reports, between 93% and 94% of Americans do not have any sort of tax liens reporting on their credit. However, that still leaves about 12 to 14 million Americans that may have tax liens or other judgments affecting their credit score.

The number of people who see a credit score benefit could be even higher. Based on research by LexisNexis Risk Solutions, about 11% of our population will have a judgment or tax lien removed from their credit file.

No matter how you add it up, since the credit bureaus are reshuffling their credit scoring model and excluding tax liens from consideration, these “lucky” millions of consumers will enjoy that sizable score increase.

So, just how high might their scores increase with the new scoring changes?

The answer is “It depends,” of course, because credit scoring is based on a host of factors and individual circumstances (like payment history, status of other existing loans, how seasoned accounts are, and credit mix). While many consumers may see their FICO score up by about 10 points after the April 16 change, a whole lot more could see their score ascend even higher.

For instance, according to a study of 30 million credit files by credit scorer FICO:

• The majority of consumers will see an increase of about 1 to 19 points.

• But between 1 and 2 million consumers may see their scores skyrocket by 20 to 39 points.

• In the case of about 300,000 consumers, their credit scores could go up by as much as 60 points when multiple liens are removed – or more.

But, it’s important to remember that the vast majority of people won’t see any credit score increase at all, as they don’t have tax liens or judgments. Others point to the fact that the 92-93% of consumers who don’t have a tax lien are somehow unduly being penalized because they won’t see their score go up.

Likewise, various financial watchdog groups have gone on record that the changes won’t make a big impact for consumers, at all. According to Eric Ellman, senior vice president of the Consumer Data Industry Association, “Analyses conducted by the credit reporting agencies and credit score developers FICO and VantageScore show only modest credit scoring impacts.”

But wait, is it possible that the credit scoring changes not only make a minimal impact but even harm consumers? “Lenders and servicers have to hedge for that risk,” says Nick Larson, business development manager for aforementioned LexisNexis Risk Solutions. “Overall, consumers actually get hurt,” he goes on, pointing to the fact that banks, lenders, and creditors will have to adjust their guidelines and regulations accordingly (therefore hurting those who didn’t see a credit score increase from erasing tax liens) just to provide the status quo risk-gauging model.

No matter what the temporary impact may be, remember that the best way to maintain a great credit score over the long term – and save thousands on your credit cards, mortgages, loans, and more – is to make your payments on time, keep your balances low, and keep a good mix of seasoned, responsible accounts.

For more help or if you’d like a great credit score increase of your own, contact Nationwide Credit Clearing for a free report and consultation.

How mortgage lenders (or consumers!) can quickly raise a borrower’s credit score.

In recent years, the housing market has benefited from historically-low interest rates, widely accessible to most homebuyers and homeowners even if they didn’t have the highest credit scores.

In recent years, the housing market has benefited from historically-low interest rates, widely accessible to most homebuyers and homeowners even if they didn’t have the highest credit scores.

However, times are ‘a changing, and with interest rate hikes and storm clouds on the economic horizon, it’s not unrealistic to think that we may see a market – and financial – tightening within a couple of years. While loan officers and mortgage brokers have their fingers on the pulse of these changes as they occur, there is one thing that will return to relevancy: credit score.

In fact, when a borrower or home buyer comes to you and applies for a loan, the difference between a 720, 680, or 620 FICO will make a huge difference in what loan programs they get approved for, and the interest rate. Furthermore, your clients will be able to afford more home when buying, save a lot when refinancing, and generally have better options.

But you don’t want to wait six months to a year to organically improve their credit score (nor will they wait around!). Luckily, we have some tactics and strategies that can help improve a consumer’s credit score in short order. In this blog, we’ll bring you the first five strategies, and look for the next five in our upcoming blog.

And you can always contact Nationwide Credit Clearing for more information on how to improve your credit score (or your client’s score) quickly!

1. Pay down balances quickly.

We know that the ratio of your debt to total available credit – called credit utilization ratio – makes up about 30 percent of your credit score. Therefore, people with maxed out credit cards or high debt loads compared to their available credit will see their scores steadily sinking.

So, the first thing you want to do when improving your credit score is to pay down as much debt as possible.

It’s important to get your credit utilization ratio below 30 percent (so you only owe $3,000 or less on a credit card with a $10,000 available balance). Credit experts even suggest keeping a utilization ratio of 10% or less to achieve a great credit score. However, don’t go all the way to 0% because it won’t show an established payment history they can use in their calculations (since you won’t have any payment).

2. Call today and request a credit line increase.

Don’t have enough money sitting around to pay down your credit balances enough to raise your scores? Another sneaky-good way to improve your credit utilization ratio – without paying down one cent of debt – is to increase your total available credit. For instance, let’s say you had a $10,000 credit line but owed $4,000 (so your utilization ratio was 40 percent).

Instead of paying down your debt, if you could get the credit card company to increase your available limit to $15,000 from 10k, your utilization ratio just went down to about 27 percent – and your score would go up! To do this, simply call the credit card company or lender and make your case over the phone and they’ll either approve or deny your request or approve a lesser increase.

3. Remove authorized-user accounts that are hurting their score ASAP.

Many times, a borrower agrees to become an authorized user on someone else’s credit account to help that person qualify for the loan, whether it’s a credit card, an auto loan, or even a business obligation. However, if that person misses a payment or otherwise mismanages that account, the borrower’s negative hit will affect your credit score, too. Thankfully, it’s easy for us to help your borrower remove themselves from the credit account in question. It usually only takes a call to the credit card company or bank with a formal request that they’re removed from the account, as well as the item deleted from their credit report, removing the negative reporting item and improving their score.

4. Consolidate accounts – virtually overnight.

A good number of consumers find themselves with multiple credit cards or accounts from the same bank. Even if the name on the card is different. By consolidating these multiple accounts with the same parent company into one, it may help their credit score take a big jump forward. That’s the case especially if they can consolidate a newer account with an older one, which will then report as a well-seasoned account. However, we do need to carefully mind their credit utilization rate to make sure this move will positively impact their score, but it can really assist some borrowers, virtually overnight.

5. Dispute any errors or bad information on your credit report.

Most people don’t realize that credit reports often contain mistakes, misreporting, duplicate items, or outdated information. All of these things may be lowering your score, but they can also be removed. Start by contacting Nationwide Credit Clearing for a copy of your credit report, and we’ll help you review it carefully for any errors or inaccuracies.

By reviewing it line-by-line, we’ll be able to highlight inaccuracies or items that are lowering your score. Remember that there are three major credit bureaus and they each may report different information, so it might be a good idea to check all three. Look for errors on larger accounts first, length of history, payments reporting on time, and that your balances are accurate.

The last step is formally disputing each inaccuracy or error with each of the credit bureaus, Equifax, Experian, and TransUnion, separately. They are legally obligated to get back to you in a certain amount of time with proof that the information you’re disputing is correct – or they have to change it or remove it.

***

If you have more questions about improving a borrower’s credit score quickly, contact Nationwide Credit Clearing for a free credit report and consultation.

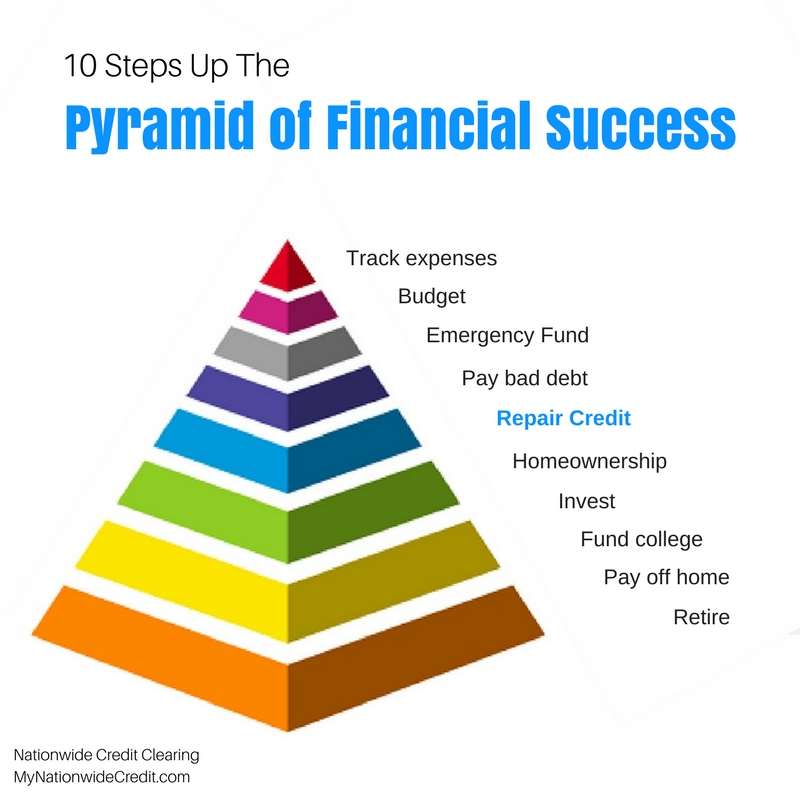

The Pyramid of Financial Success

The Pyramid of Financial Success

The Pyramid of Financial Success

No matter what our financial situations look like, everyone pretty much wants the same thing: low bills, plenty of savings, living in our own home, and enough investments to retire whenever we wish. Achieving that lofty goal is also very obtainable if you follow these 10 steps to climb the Pyramid of Financial Success:

1. Track expenses

Before you do anything else, it’s critical to know exactly how much you’re spending every month, and on what. Sure, you may THINK you know what your bills are and how much you spend, but I bet that you’ll be pretty shocked when you write down every single penny you spend (or use one of the great financial apps that help you record expenses). Try this for a month and then add up the total expenses and you’ll be amazed how much you’re blowing on impulse purchases, things you don’t really need or even want, and items that you didn’t realize are costing you!

2. Set a budget

Now that you know exactly what you’re spending your hard-earned dollars on, it’s time to tighten the belt. Ruthlessly slash everything from your budget that’s not a necessity – and hold yourself accountable to it. This will take some discipline but turn it into a fun game, and keep reminding yourself that by sacrificing NOW, you’ll be able to put yourself in a much better financial situation that lets you spend more on the things you really love and want later on.

3. Build an emergency fund

Did you know that 40 percent of Americans couldn’t come up with $400 in cash if faced with an emergency today, and two-thirds don’t have even $1,000 saved? As we’ve turned to debt more and more, the savings deficit in the U.S. has grown. However, it’s so important that you accumulate a rainy-day fund, which is a fair bit of cash that you can use when the car breaks down, you miss work because of a medical problem, or some other challenge. Start by putting $400 away, then $1,000, and keep saving until soon, you’ll have at least a few month’s total expenses saved as a cushion.

4. Pay debt

This is a big one! Once you’ve set a budget and put aside a few bucks as a safety net, it’s time to tackle the hardest part of all: paying off debt. In fact, the average American household now has $16,883 in credit card debt, $50,626 in student loans, $29,539 in auto loans, and, if they’re lucky, a mortgage on top of all that. But the one that we want to start with is paying off credit cards, as well as other revolving debt and retail installment loans. This is essential if you want to free yourself from a life of struggling and stressing about money and bills, and open up a much more secure and comfortable relationship with money.

There are several ways you can pay off your debt, but one of the best is using the technique of Debt Snowballing which is advocated by financial gurus Dave Ramsey, Suzie Orman and others. We’ll bring you more info on Debt Snowballing soon.

5. Repair credit

In fact, it’s a good idea to tackle #4 and #5 on this list in conjunction so that you’ll end up debt free AND with a fantastic credit score, starting with a free credit report and consultation from Nationwide Credit Clearing. We’ll go over your credit report and debt load with you, identifying which of them should be paid off first since they have the highest interest rates (or smallest balances).

Likewise, we can advise you which of your credit accounts should just be paid down (not off) and kept open. Our service will also attempt to remove negative, incorrect, and outdated items from your credit report, boosting your score to new heights.

How important is a great credit score? These days, just about everything you pay is tied to credit score, from all of your credit cards, your mortgage, and other loans, as well as utilities, cell phone accounts, the ability to rent a home, and even your job!

6. Buy a house

Speaking of (not) renting, once you have some savings and your debt paid off, the next big step in your financial pyramid is buying your own home. In fact, homeownership is still the American Dream, allowing you to build equity, pay down your loan, enjoy lucrative tax breaks, and experience the pride of ownership. These days, down payment programs make it easier than ever to come up with the money needed to buy a house, and you’ll essentially be paying yourself every month instead of your landlord!

7. Invest

Your bad debt is gone, and you’re now in your own home, so it’s time to start investing. Actually, you should be investing from day one in a 401K, mutual fund, or other safe, stable vehicle, as the power of compounding really comes into play the earlier you start. Contact a financial planner or advisor for the best way to invest and save for retirement considering your situation and goals.

8. Fund college

Remember how we mentioned that the average household has $50,000+ in student loan debt? Why not give your children a head start (not extra hurdles) in life by funding as much of their college education as possible instead of piling on more debt?

9. Pay off your home

We paid off your bad debt when we zeroed-out those credit cards, and you’ll get to a point high up the pyramid of financial success where the next logical step will be to pay off your home, too. There are several great strategies to help you do this, such as sending in a 13th payment every year, paying every two weeks instead of monthly, or adding extra funds to pay off principal faster. Either way, once you pay off your home in 20 or even 10 years instead of 30 (like most mortgages), your biggest bill will be knocked off the list.

10. Retire

With little or no debt, plenty of savings, a well-spring of investment income, and your home paid off, you’ll be in the enviable position at the top of the pyramid, where you can choose to retire whenever you like. Of course, that doesn’t mean that you must stop working, as many people opt to pursue their passion or work a lighter schedule just because it’s enjoyable. Either way, you’ll be the master of your financial life – not the other way around! Congratulations on making it to the top of the pyramid!

What the wealthy OVERstand about money that the rest of us may not.

The average person now has more knowledge available to them than any time throughout history, including plentiful wisdom about money, finances, and wealth. However, the income gap keeps growing in the U.S., with the rich getting richer and the typical middle-class family struggling just to make ends meet.

The average person now has more knowledge available to them than any time throughout history, including plentiful wisdom about money, finances, and wealth. However, the income gap keeps growing in the U.S., with the rich getting richer and the typical middle-class family struggling just to make ends meet.So what do the wealthy OVERstand about money that the rest of us may not?

1. Debt is dangerous

The number one principle of money that wealthy people understand is to not misuse debt. In fact, every time you use your credit card to make everyday purchases, you not only spend more than you would with cash (on those impulse purchases). You’re also essentially spending 110, 120, or even 130 cents on the dollar if you factor in interest charges and other fees. Wealthy people pay cash for their purchases and resist the temptation to use debt as a way to afford things they otherwise could not or should not.

Likewise, wealthy people understand that there is good debt (like mortgages, business loans), etc. that helps them achieve assets and investments, and bad debt (credit cards, car loans, etc.) and know how to utilize the former.

2. Your credit score is everything

Let’s say that before you even reached in your pocket and spent a single dollar on groceries, credit card bills, your mortgage or rent, insurance, or any other expenses, there was a number that basically ranked how much or little you should pay for those things. You would probably concern yourself with knowing and improving your ranking so you’d spend less, right?

Well, that’s exactly what credit score does. Rich people understand that credit score dictates so much of what we pay and even opens up remarkable financial opportunities if we have great scores, and therefore, make sure their FICO is fantastic.

3. Compounding and the time value of money

Would you rather have a penny a day that doubles every day for a month, or $1,000,000? Believe it or not, you’d miss out if you chose the quick seven-figure payout, as the first option would yield you $5,368,709.12 in those same 30 days!

Welcome to your first lesson in the time value of money, as your money will grow exponentially over time thanks to the magic of compounding. For that reason, the wealthy aim first to eliminate debt, buy their own home, and obtain assets like stocks, bonds, and other investments that will grow for them over time (more on the ‘time’ part later).

4. Don’t forget about taxes

It’s not what you make but what you keep! What good is a job that pays you $50,000 a year if you give 30% of it away for taxes (for example) when you could have a $40,000 job but pay in a much lower tax bracket? Wealthy people are always aiming to maximize their returns (make more) and minimize their liabilities (spend less) and saving on taxes is a huge part of that.

And when it comes to that yearly tax return you may be getting back, do the right thing with it and pay off debt and put some in savings!

5. Buy a home!

Homeownership always has been (and always will be!) part of the American Dream. It’s not only nicer living in your own place, but the financial advantages are impossible to ignore.

When you ow your own home and pay a mortgage every month, you’re paying off what you owe on the home (over 30 years), so it’s sort of like a forced savings plan.

Likewise, homes have appreciated in value over any 10-year period throughout modern U.S. history, so purchasing a home early and paying it off allows you to retire without having to pay mortgage or rent (and then you can leave it to your children). Likewise, owning a home offers one of the biggest tax breaks you’ll ever get from Uncle Sam, too.

Meanwhile, the alternative is to keep paying rent to your landlord every month, which yields you no appreciation, you’re not paying anything down or building any equity, and you’re missing out on tax breaks. The wealthy aim to be landlords; not pay a landlord!

6. Save first

Sure, we know that when your paycheck arrives once or twice a month, it’s probably already spent and accounted for before you can even cash it. But wealthy people become that way by making sure they save first. In fact, most financially stable people utilize auto-withdrawals from their paychecks to put some money into savings, pay bills, and maximize their investments – before they even see any money from their paycheck. Doing so takes some discipline and sacrifice, but the results will pay off big-time!

7. Education never ends

We all have 24 hours in every day, but instead of gossiping, wasting time arguing on Facebook, and watching funny cat videos, wealthy people invest their time in learning and growing. That can be learning new job skills, going back to school for another degree, or just reading, listening, and watching inspirational and educational messages. Of course, many of those are about improving their finances, so pat yourself on the back for reading this blog!

***

If you’d like more information about credit, debt, and putting yourself in a better financial position, contact us for a free consultation and credit report.

How long will negative information stay on our credit reports?

How long will negative information stay on our credit reports?

How long will negative information stay on our credit reports?

Did you miss a credit card payment, have a bill go to collections, or even had to file bankruptcy recently? If so, your credit score has probably taken a pretty big hit. You’re also probably wondering when it will stop showing up on your credit report so you can move on.

Luckily, negative information that’s reported on your credit doesn’t last forever. In fact, we know the timeline when they will “fall off” and not be reported anymore thanks to the Fair Credit Reporting Improvement Act of 2014, which defines the timelines for how long negative information can remain on your credit file.

Here’s a rundown of how long common items will remain on your credit report, where they very well could be hurting your score:

Credit accounts

Credit cards, store cards, retail accounts, auto loans, and other credit accounts that are paid on time can keep reporting on your credit for up to 10 years from the date of last activity.

Late payments for credit accounts

However, if you missed payments or failed to pay on time, that negative data will also be reported, but for a period of 7 years (starting from the exact date the account was first past due.)

Late payments for other debts

While late payments on common credit accounts will show up for 7 years, those same rules don’t apply for revolving or installment loans. In fact, if you have a revolving or installment debt that is now current but does have a late payment some time in the past, that negative item (late payment) will appear on your credit report for 10 years past the date of last activity.

While it may get a little confusing, the late payment history will be removed for these installment and revolving debts after 7 years, but the reporting for accounts that are current will show up for 10 years.

Collections

Collection accounts usually will show up on your credit report for a full 7 years after the date the account first became past due. Remember that the date it was past due will be earlier than the date it was sent to collections, which could be 90 days or more after that.

Bankruptcies

If you’ve been through a chapter 7 bankruptcy (most common for consumers), a chapter 11 bankruptcy, or a non-discharged or dismissed chapter 13 bankruptcy, that will typically keep reporting for 10 years from the date the bankruptcy was first filed (not the date they were discharged).

However, chapter 13 bankruptcies that have been discharged can only stay on your credit report for 7 years from the date they were first filed.

Public Records

Judgments usually stay on your credit report for 7 years after the date they were filed, whether you have satisfied (paid) them or not.

If you have a tax lien and then pay it off in full, the lien will still report on your credit for 7 years from the day it was satisfied.

However, tax liens that go unpaid (unsatisfied) will stay on your credit report indefinitely – which means that you’re stuck with them until they’re paid off.

Inquiries

When a third-party requests a copy of your credit report (usually a lender, retailer, or employer), that activity shows up on your credit report, and can possibly impact your score. But the good news is that there’s usually not a big hit, and the credit bureaus only keep this on your report for 1 or 2 years.

But there are different types of credit inquiries that might have different reporting timelines. For instance, promotional inquiries (when you received a pre-vetted offer for credit) don’t affect your score and generally remain on your credit for only 12 months. When one of your current creditors performs a review of your account, it also does not affect your score and remains for 12 months. Finally, when you request a copy of your own credit report, it does not affect your score and will remain on your credit file for up to 24 months.

However, there are some slight variations on these timelines depending on state law:

For instance, in California, paid or released tax liens will stay on your credit file for 7 years from the date released, or ten years from the date filed. And unpaid tax liens remain on your credit file for only ten years from the date they were filed – not indefinitely.

New York State residents see their satisfied (paid) judgments only remain on their credit file for 5 years and paid collections only reporting for five years from the date of last activity.

***

I know – that’s a lot to remember. So we’ve put together this easy list so you can quickly see how long a certain negative item will stay on your credit report:

The item remains two years (or less);

Credit Inquiries

The item remains no more than 7 years:

Late payments

Collections

Judgments

Settlements

Foreclosures

Repossessions

Released tax liens

Charged off accounts.

Note: the timeline begins from the date of default OR 180 days after the date of the first delinquency that eventually went to collection.

The item remains no more than 10 years:

A Chapter 7 bankruptcy can remain on a credit report for up to 10 years from the date it was first filed.

A Chapter 13 bankruptcy can also remain on a credit report for up to 10 years.

The item will remain indefinitely (until paid):

Federally guaranteed student loans that are unpaid and in default can remain on a credit file indefinitely until such time as they are paid.

Unpaid tax liens may report on a credit file indefinitely.

***

Remember – there’s another way to get rid of negative items that are reporting on your credit BEFORE they naturally fall off after all of these years! Contact us for more information!

How men and women differ when it comes to credit and debt.

How men and women differ when it comes to credit and debt.

How men and women differ when it comes to credit and debt.

There are some profound differences between men and women when it comes to men and women, from what we earn, to what we spend our money on, and even how we go about investing. When it comes to credit and debt, there are some interesting comparisons between males and females, too – although it might not always be what you think.

For instance, when it comes to credit score, would you guess that men or women are leading the way with better scores?

In fact, according to surveys by Experian, women have a higher average credit score (675) than men (674).

Men have more debt, with an average of $26,227 compared to $25,095 for women.

The average man owes $5,282 in credit card debt, compared to only $4,867 for women in credit card balances.

Women have 4.1 credit cards on average, while the average man only carries 3.7 cards.

But at least part of that debt total for men can be attributed to home loans. Of all people who are mortgage holders, men have an average of $187,245 in home loans compared to $178,140 for females.

In fact, the average U.S. man has $50,425 in mortgage debt versus only $35,116 for the average American woman.

Another check in the “Men” column is that 60% of men have more savings than credit card debt, while only 49% of women have more in their savings account than their credit card balances.

While both sexes sometimes exhibit less than stellar use of credit cards, women lead the way in a metric called “problematic behaviors” when it comes to cards.

In fact, only 33% of men display two or more problematic behaviors with credit card usage, compared to 38% of women.

But men carry a larger total of debt than women (+4.3%), and females also use only 30% of their available credit, while men use 31% or higher on average.

Men comparison shop for better rates and terms on their credit cards more than women (37% to 31%).

Women also carry a bigger balance from month to month on their cards (60% do so) compared to men (55%).

And 42% of women only make the minimum payment every month, compared to only 38% of men (a big no-no for your credit score).

Backing up that statistic, 45% of men pay their balance in full every month, compared to only 39% of women.

Women also pay late fees on their credit cards far more than men, at a rate of 29% (of women who have to pay late fees) versus only 23% of men.

Despite having lower credit scores (slightly), men also have better interest rates on their credit cards than women. In fact, the average rate for men is 14.3%, compared to 14.9% for women’s credit cards.

How about student loan debt? On a per-student basis, women have far more student loan debt than men. In fact, the average woman has $11,786 in student loans, compared to only $8,187 for men.

But men finance far more for their cars, with an average auto loan tally of $8,249, while women only owe $6,693 on their car loans on average.

While the one-point credit point advantage favors women by a small margin, the data reveals that women do have a better understanding of credit scores and credit reporting. The Experian study concluded that:

48% of men incorrectly believe that marital status factors into credit scores, compared to only 38% of women who mistakenly think the same thing.

46% of men mistakenly think marital status is a factor in scoring, versus only 34% of women who get that wrong.

74% of women understand that the credit bureaus collect the information that’s used for scoring, while only 68% of men realize that.

Women are more apt to know when scores are free (65%) than men do (60%), know when lenders are mandated to discloses scores (53% to 46% for men), and better understand the importance of regularly checking and monitoring their credit reports (77% to 72% for men).

***

So which gender wins the title of “Best with Credit and Debt?” It seems like women win out over men on average in certain important factors, but men are profoundly better in a few others. Overall, well call it a tie and just say that BOTH men and women need to work hard, educate themselves, and do better with credit and debt if they want to improve their finances and get ahead!

And you can start with a free credit report and consultation from Nationwide Credit Clearing! Contact us to get started.

The difference between hard and soft credit inquiries.

Most people check their credit periodically, such as when they’re about to apply for a big loan, once a year, or every four months (like you should). But you may not realize that a whole lot of others are checking your credit – and probably on a more frequent basis. In fact, every time you apply for a credit card, submit an application for a student loan, take out a store discount card, or even apply for insurance or rent a new apartment, your credit is probably being pulled.

Most people check their credit periodically, such as when they’re about to apply for a big loan, once a year, or every four months (like you should). But you may not realize that a whole lot of others are checking your credit – and probably on a more frequent basis. In fact, every time you apply for a credit card, submit an application for a student loan, take out a store discount card, or even apply for insurance or rent a new apartment, your credit is probably being pulled.

Those credit pulls also can ding your credit score, if not handled correctly. Sometimes, that’s inevitable, and other times it’s avoidable. But it’s important to understand the facts about hard and soft credit inquiries, or credit “pulls.”

In fact, only 26% of women and 31% of men know the difference between “hard” and “soft” credit inquires, or credit “pulls.”

So today, we’ll give you some fundamental information about credit inquiries, both hard and soft. Contact Nationwide Credit Clearing if you have further questions about credit pulls, and would like a free copy of your credit report and consultation with a credit expert!

Hard credit pulls:

Hard credit pulls only take place when you apply for new credit accounts.

Or, a hard pull will occur when one of your existing creditors decides to pull your credit. In fact, most creditors can access your credit any time, for any reason they deem, without needing your permission first.

Creditors commonly do this when they’re reviewing your account to consider an increase to your credit line.

Soft credit pulls:

Sofer credit pulls, however, can occur either with inquiries where the consumer voluntarily agreed to have their credit accessed, or other involuntary inquiries.

For instance, soft pulls usually take place when you’re applying for a new job, a cell phone account, trying to rent an apartment, etc.

Effect on credit score:

There is no one set rule for how credit pulls will affect your score. But, typically, hard credit pulls will only have a slightly negative impact on your credit score, possibly dropping your score a few points in the short term.

Typically, your FICO score can go down about 5 points per inquiry if you have your score pulled too much by the wrong vendors. The drop could be greater if you have few accounts or a short credit history without seasoned, positive factors to compensate.

In fact, the negative effect of hard pulls usually last only one year, but most of the damage disappears within the first 90 days.

Are all credit score pulls considered equal?

Since credit scoring is primarily a means of gauging the risk of default, consumers with high credit scores will suffer a little more damage from hard credit pulls. That’s because the credit algorithms consider the fact that they’re getting their credit pulled atypical, and more of a red flag.

So the higher your score to begin, the more damage a hard credit may do.

Additionally, unsecured credit inquiries, like you’ll find with personal credit cards, retail cards, and in-store accounts, will cause the most damage to your score.

When current creditors pull your credit:

We are certain that soft credit pulls have a negligible negative effect on credit scoring – or none at all. That’s the reason why most of your current creditors will only order soft credit pulls on your account, not hard pulls.

Current creditors usually also do a soft pull every month or so, although some check up on their consumers much more frequently.

Some credit pulls always act as hard inquiries, some are always soft injuries, and some can show up as either/or.

Hard pulls are most often found with:

• Applications for new credit cards

• Requests t activate a pre-approved credit offer (such as you receive in the mail)

• Applying for a new cell phone account and contract

Soft pulls are most often found with:

• Background checks by potential employers

• Your bank verifying your identity

• Initial credit checks by credit card companies that want to issue you preapprovals

Who can pull your credit, whether through hard or soft inquiries?

Lenders

Mortgage companies

Student lenders

Banks

Credit card companies

Financing departments of retail stores

Auto dealerships financing departments

Utility companies

Cell phone companies

Employers

Landlords

Insurance companies

Collection agencies

Child support agencies

Court agencies

Anyone with “Permissible Purpose,” as deemed by the Federal Credit Reporting Act.

Timing is everything with credit pulls:

Timing is so important when it comes to credit pulls. The more “bad” inquiries that appear on your report within a short time, the bigger hit to your score. For instance, if you apply for five new credit cards within a two-week period, it definitely is seen as risky to the credit bureaus, and your score will drop accordingly.

However, the credit bureaus do account for consumers who want to “shop around” for large and important loans, like mortgages, business loans, etc. Of course, shopping for the best rate on a single loan (not applying for multiple loans at once) means getting your credit score pulled several times within a short period, but the good news is that this practice won’t hurt your credit score.

In fact, the credit bureaus typically just count this group or batch of inquiries as one if they’re within a 30-day period (or a 45-day period with some credit scoring versions).

So, if you’re shopping around for the best rate on an important loan, try to contain all credit pulls to within a 30-day period to keep your score in good order!

***

Contact Nationwide Credit Clearing if you have further questions about credit pulls, and would like a free copy of your credit report and consultation with a credit expert!

How much will a late payment drop your credit score?

Sometimes, life happens. Maybe you went on vacation and forgot to send off your credit card payment before you left, or you did send it off (you swear!), but it was lost in the mail. Or, you just flat-out didn’t have enough money to pay a bill, so the late notices are piling up.

Sometimes, life happens. Maybe you went on vacation and forgot to send off your credit card payment before you left, or you did send it off (you swear!), but it was lost in the mail. Or, you just flat-out didn’t have enough money to pay a bill, so the late notices are piling up.

When that happens, you may be wondering how far your credit score will drop, as the payment becomes 30, 60, and then 90 days later – or more.

The answer is, like so many questions in life, “It depends.” However, we do have some factual information and a few guidelines to go by.

For instance, we do know that paying on time is a major factor in how our credit scores are calculated. In fact, according to FICO, payment history makes up 35% of your credit score.

That being said, there is some gray area when it comes to the credit score damage a late payment can cause.

Here are five factors that help determine just that:

- Was it a 30, 60, or 90-day late payment?

Missing a payment’s due date by 30 days is the first huge milestone that will affect your credit, but continuing to miss that payment by 60 and then 90 days will impact your score even further. Remember that credit reporting is all about gauging risk (for potential lenders and creditors). So while a 30-day late may be explainable as a mistake, oversight, or one-time error, 60 or 90-day lates show that you are really in a financial freefall. Therefore, your score will drop accordingly, so you should definitely avoid a 90-day late payment if you want to save your score.

- How long ago was the late payment?

Credit scoring algorithms also factor in recency – how long ago the late payment took place. So if a 30,60, or 90-day late just hit your credit report this month, your score will drop a lot sharper than if the same late payment occurred five years ago. But that also means that as time goes on (and you continue to make your payments on time) the negative scoring

- Was it just one account with a late payment – or more?

If you’ve only missed a payment with one credit line, loan, or account, it will damage your score a lot less than if you’ve missed payments over multiple accounts.

- What type of credit account did you miss a payment for?

Of course, the credit reporting algorithms give more weight to more important loans, like mortgages, etc. over smaller ones, like a $250 store retail card. Therefore, a 30-day late payment on a mortgage loan will hurt your score a lot more than with smaller and lesser accounts.

- How long have you had that account?

Accounts that are well seasoned – that have been open and in good standing or a long time – will take less of a hit than newer accounts. So, avoid missing payments on that brand new credit card!

- What was your score before the late payment?

Believe it or not, the BETTER your credit was before the late payment, the MORE the late will hurt your score! Are you be punished for having a great score? NO; but the credit bureaus are gauging risk, and a late payment that’s out of character for a high-scorer is more alarming than the same late for someone who commonly makes credit missteps.

A 30-day late on your credit report will probably result in a credit score drop of around 80 points IF your score was originally around 680 or so. But if your score started out at 780 or higher, one late payment could send your score plummeting by 90-110 points!

Ouch!

However, if you’ve missed a payment, there are some ways to do damage control. Immediately contact your creditor and work out a payment, and you can even ask them to delete the negative blemish on your credit if and when you pay.

But different lenders report on different days of the month, so you may get lucky and prevent them from even reporting a 30, 60, or 90-day late. Again, you definitely want to avoid paying 90 days late on any accounts, as that will cause significant damage to your credit – and stay on your report for seven years!

The good news is that Nationwide Credit Clearing is here to help you clean up your credit and improve your score! Contact us if you have any questions about late payments or for a free credit report and consultation!

10 More things you didn’t know about credit scores, credit reporting, and debt in America

Your credit score impacts so much in your life these days, from rent and homeownership to credit card approvals, interest rates on student and auto loans to even employment. But too often, we’re still in the dark when it comes to credit scores, credit reporting, and general financial knowledge about debt management.

Your credit score impacts so much in your life these days, from rent and homeownership to credit card approvals, interest rates on student and auto loans to even employment. But too often, we’re still in the dark when it comes to credit scores, credit reporting, and general financial knowledge about debt management.

As the nation’s leader in credit repair solutions, Nationwide Credit Clearing is committed to help educate you about these important topics. This is part two of our ongoing series, 50 things you didn’t know about credit score, credit reporting, and debt. Look for part one here, and contact us if you have any questions or credit issues at all!

1. Which company earns the title as the most popular credit card in the rest of the world? That honor belongs to both Mastercard, which has 551 million cards issued throughout the world as well as 180 million cards here in the United States. However, Visa wins top-dog honors on home soil, with 278 million cards floating around the U.S., as well as 522 in the rest of the world.

2. It’s no surprise that people often turn to their credit cards to pay bills and living expenses once they are unemployed, In fact, 86 percent of low and middle-income households who have a working member that is now unemployed turn to credit cards to fill the gaps monthly.

3. Likewise, almost 50 percent of low and middle-income households now are carrying credit card debt that comes from out of pocket payments they have to make on medical bills and expenses.

4. It’s interesting to look at a map and compute the average credit score for each state (OK, I don’t get out much!). In fact, the states with the lowest average credit scores are in the south and southwest, including New Mexico, Texas, Oklahoma, Arkansas, Louisiana, Mississippi, Tennessee, Georgia, Alabama, South Carolina, Nevada, and Florida. In those states, an alarming 40 percent of the population have subprime credit scores!

5. However, the states with the highest average credit scores are found in the north and midwest. Minnesota and North Dakota are the states with the highest average credit scores, with 707 and 700 average FICOs, respectively.

6. Aside from the state you live in, there are some other puzzling correlations between the heights of your credit score and your seemingly unrelated behaviors. For example, one study found a direct correlation between credit scores and which email provider the participants used! They found that Comcast email user (692 average) and Gmail, (682) have above average scores, but MSN (669), Aol (668) and Yahoo! (652) email users have below average scores.

7. But more common-sense correlations also apply. For instance, there are significant differences in credit scores based on age. Baby Boomers and the Silent Generation (68-85 years old) have average scores of 700 and up, while Gen Xers average a 655 score, Millennials average a 634 score, and Gen Z is lagging with a 631 average Vantage Score.

8. One correlation that we could have easily predicted is that between scores and homeownership, In fact, a Federal Reserve study found that the average credit score among homebuyers and homeowners is 728 – significantly higher than the national average. Additionally, they found that only 6.8% of homebuyers or homeowners had scores below 620 in the study.

9. We hear about our credit scores impacting home ownership, credit cards, interest rates on other loans, renting, and even employment. But did you know that your credit score can make a big difference on…your dating life? It’s true! According to a 2016 Bankrate survey, almost 4 in 10 U.S. adults say that they’d rather date someone with a good or excellent credit score, but they’d be wary of dating a sup-prime suitor. In fact, 43% of women and 32% of men said that a person’s credit would have an impact on if they dated them.

10. Americans are still pretty mixed up, confused, and turned around when it comes to basic knowledge of credit scores and credit reporting. In fact, studies have shown that of an average sample Americans, 47% didn’t know that credit scores are used by non-creditors like electric utilities and home insurers, 68% didn’t know that cell phone companies use credit scores, and 32% had no idea that landlords could check their credit!

***

Do you have questions about your credit or looking to improve your score? Contact Nationwide Credit Clearing for a FREE credit report and consultation at (773) 862-7700 or mynationwidecredit.com!

The 15 most common credit score wrecking balls!

1. Paying late (or not at all)

1. Paying late (or not at all)

Of course, one of the biggest wrecking balls that smash through your credit score and finances is paying your bills late. For accounts on your credit report, like mortgages, credit cards, auto and student loans, and many others, paying even just a day or two late can trigger a 30-day late, which will significantly ding your score.

Even worse, being 90 days late causes further damage to your credit report that. Remember that payment history (paying on time every month) is 30% of your score, so pay on time to dodge this wrecking ball!

2. Max out credit cards or accounts

Your credit ratio, or the amount of total debt you hold compared to your available credit, is also a major factor for your score, making up 30% of your FICO as well

So, when you max out your credit cards, even if they are paid on time, your score will get smashed.

3. Have an account charged off and go to collections

Once you are 90 days late with your credit card payment or bill, the next step is typically that your creditor soon charges off the debt, sending it to a third party for collections, causing even more damage to your credit score that can be hard to erase.

4. Cosign for someone who doesn’t pay

Maybe you have a friend or even family member that asks you to be a cosigner on their credit card, auto loan, or another account. I know that you’d like to help, but aware that if they don’t pay, YOU are fully responsible for their debt. In fact, those late payments will show up on your credit report just like you took out the debt, yourself.

5. Filing bankruptcy

If you want to talk about a big, heavy wrecking ball, filing a Chapter 7 or 13 Bankruptcy is one of the most damaging events to someone’s credit score. However, for some people, legal insolvency is still the best option if they are drowning in debt with no way out. The good news is that Nationwide Credit Clearing can work with you during and after the BK process to repair the damage!

6. Foreclosing on your home

Another major wrecking ball is foreclosure, which occurs when you miss enough house payments so the bank legally repossesses the home. Foreclosures cause serious damage to your credit score and will take seven years to fall off your credit report.

7. A judgment against you

This is a dangerous and scary wrecking ball for consumers. When you don’t pay your debt obligations, your lender or third-party collection agencies may take you to court, trying to secure a judgment for the amount you owe (plus late fees, penalties, and court costs). Also, there are state and federal judgments for unpaid child support, alimony, IRS tax liens, etc. that will never disappear from your credit file until they’re satisfied! Contact us immediately if you have judgments!

8. Applying for new credit recklessly

If you start filling out a lot of credit card and loan applications within a short period, it shows the credit bureaus that you’re financially desperate, or something is wrong. Since their main job is indicating risk for lenders, your credit score will take a hit, accordingly.

9. Close old credit cards in good standing

It may seem like good financial sense to cancel old or unused credit cards, but by shutting down a seasoned card or credit line in good standing, you’ve just effectively erased a positive track record of paying on time. Sorry, but your score will go down once that positive payment history is taken out of the equation.

10. Not pay student loans

Remember when we were talking about judgments? Unpaid federal student loans will level your credit very quickly, and they also won’t naturally disappear from your credit report until they’re paid. Unfortunately, unpaid student loans are the fastest growing form of credit score “wrecking ball” in the United States.

11. Utilize payday loans, cash advances, or financing through Rent-a-Centers

All credit is not created equal, and when you take out loans that are deemed risky, it will hurt your score. Payday lenders, check cashing services, certain retail credit cards, and financing purchases like furniture can shake the foundation of your score.

12. Try to outthink the credit card companies with balance transfers

Are you “jumping around” between credit card offers, taking out 0% interest or cash-back offers and moving balances around just to stay one step ahead? The chances are that questionable financial practice will catch up with you sometime, in the form of penalties, late fees, small print you miss, or higher interest rates. But even if it works, your credit score will be battered and bruised.

13. Not using your credit at all

About 30 million Americans are considered “Credit Invisible,” as they don’t have a sufficient – or any – credit history. If you don’t have any credit cards or other accounts, there’s no established payment history for the credit bureaus to judge you by, and your score will be rock-bottom. Luckily, you can contact Nationwide Credit Clearing, and we will guide you through how to establish credit and build a good score.

14. An imbalanced mix of credit

Do you have only credit cards on your credit report? Or, is have you taken out four installment loans but nothing else? An imbalance between credit cards, installment debt, auto or student loans, mortgages, etc. can also act like a demolition crew to your credit score.

15. Not checking your credit frequently

These days, credit and identity theft is the fastest growing form of crime around the world, and companies that collect your sensitive financial data – and even credit bureaus (like Equifax) are susceptible to hackers. Even if you pay all of your bills on time and do everything else correctly, the best way to protect your credit and finances is to regularly monitor your credit report.

Start by contacting Nationwide Credit Clearing for a free credit report and consultation at (773) 862-7700 or MyNationwideCredit.com.